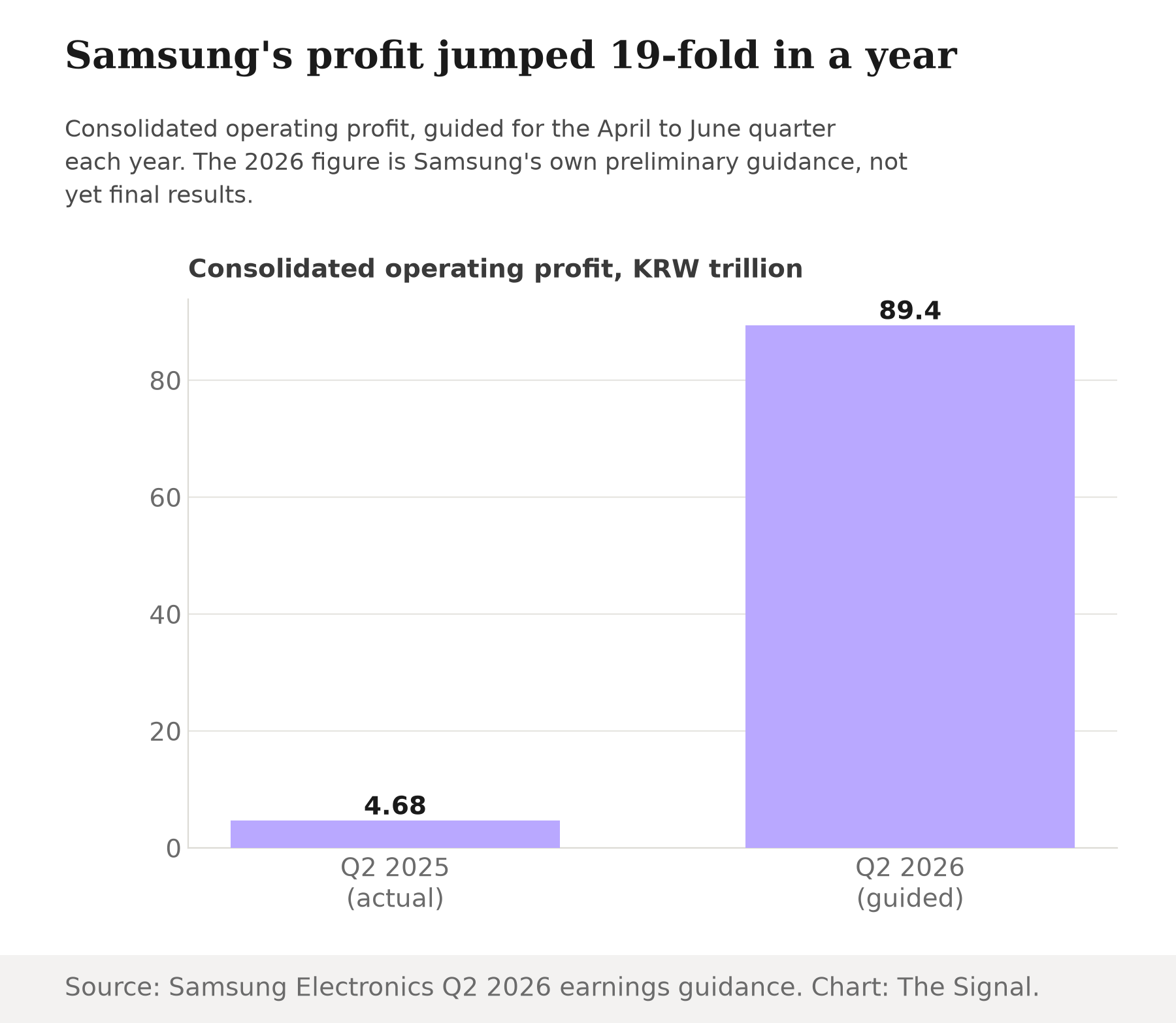

Samsung Electronics told investors on July 7 that its April to June quarter produced consolidated operating profit of approximately 89.4 trillion won, on sales of about 171 trillion won. That is roughly 19 times the 4.68 trillion won the company earned in the same quarter of 2025. Citi Research, as reported by Reuters, traced the surge to average selling prices for DRAM and NAND flash memory that rose 44% and 53% quarter-on-quarter respectively in that same April to June 2026 period. Read only the guidance number and the story writes itself: the AI boom's insatiable appetite for memory has handed the world's largest chipmaker its best quarter on record.

Samsung's guided profit is roughly 19 times what it earned a year earlier.

It is worth slowing down on that reading. Samsung's own shares still closed nearly 7% lower on the day it announced the guidance, as investors weighed AI-capex and demand-durability concerns against the headline number. A stock does not sell off on genuinely free money. Strip out the framing of a single record quarter and a different question appears: who is actually paying for this memory shortage, and is Samsung's own business absorbing part of the bill?

The bill lands on Samsung's own phone division

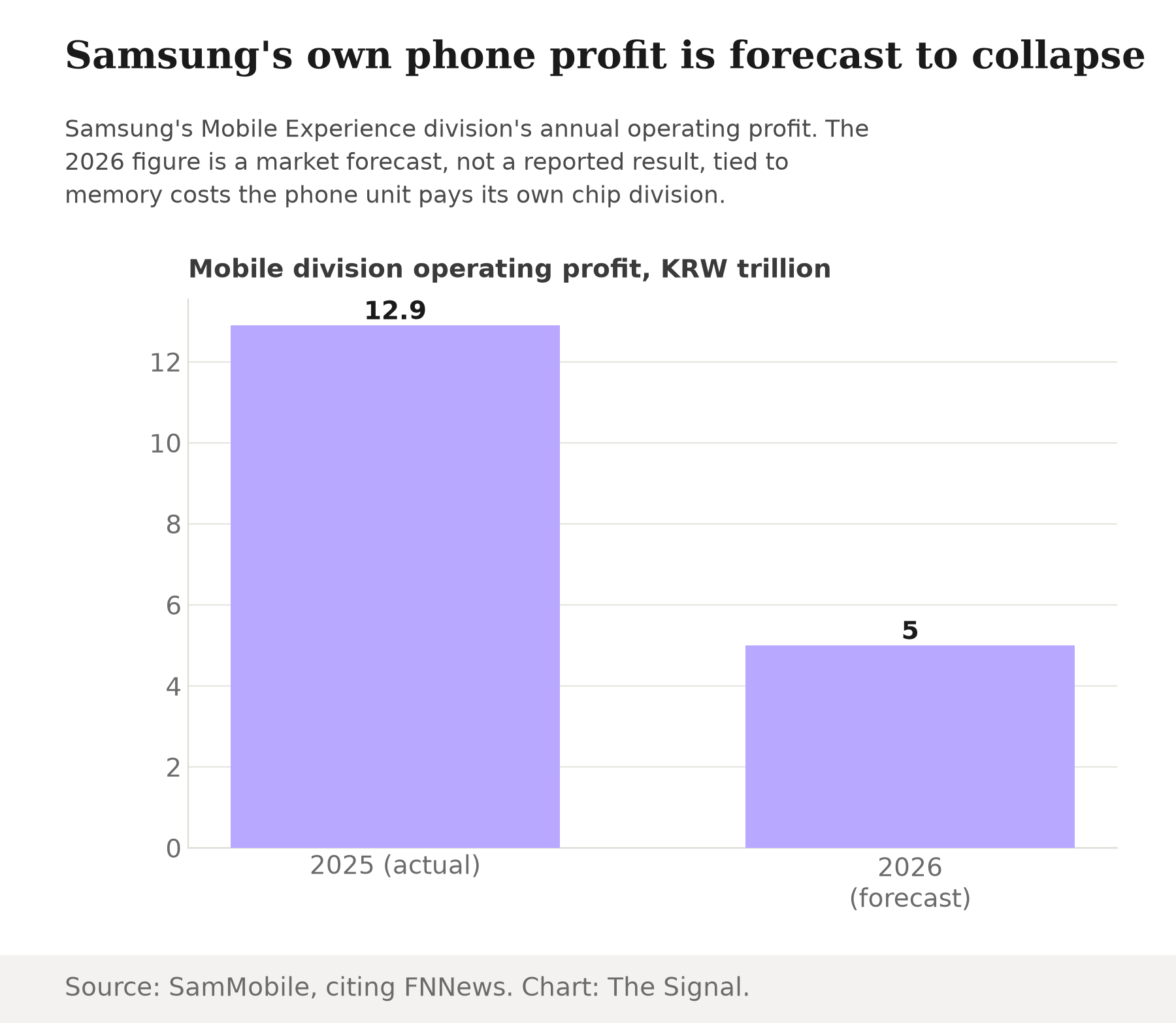

The clearest answer sits inside Samsung's own numbers, not a rival's. Samsung's Mobile Experience division reported an operating profit of 12.9 trillion won in 2025, and that figure could fall to around 5 trillion won in 2026, as SamMobile reports, citing a report from the Korean outlet FNNews, because memory-chip costs the mobile unit must buy from Samsung's own semiconductor division rose roughly 8.5-fold over the year. Two numbers from the same company, in the same year: a fall from 12.9 trillion won to about 5 trillion won is a drop of roughly 61%.

Samsung's own phone division could lose more than three-fifths of its 2025 profit.

The chip division's grip on Samsung's bottom line is not a one-quarter fluke. The Elec, a Korean semiconductor-industry trade publication, reports that in the first quarter of 2026 the Device Solutions division alone generated 53.7 trillion won of operating profit on 81.7 trillion won of revenue, against 57.2 trillion won of total consolidated operating profit for the entire company that quarter: chips were roughly 94% of everything Samsung earned, before the mobile division's own costs even entered the picture.

That is the mechanism the guidance number hides. Samsung is not simply a winner of the memory shortage; it is both the seller and, through its own phone business, one of the buyers. The internal price it charges itself has shifted enough that the phone division's fortunes are moving in the opposite direction from the parent company's headline profit. The chip windfall and the phone squeeze are two faces of the same shortage, inside one balance sheet.

The foldable price hike is the visible symptom

Consumers are about to see this mechanism directly. Leaked Korean retail-channel pricing reported by The Korea Herald, citing the outlet Bloter, points to Samsung's Galaxy Z Flip8 launching at about 1.68 million won ($1,100) for the 256GB model, a 13.3% increase over the Flip7, ahead of the phone's scheduled July 22 unveiling. A foldable is a premium device with room to absorb a cost increase. The mechanism is more damaging further down the price ladder.

Beyond Samsung, the shortage is repricing every phone

Counterpoint Research now forecasts global smartphone average selling prices will rise 6.9% in 2026, up from an earlier forecast of 3.6%, in a note reported by CNBC. The same note found that bill-of-materials costs for phones priced below $200 had already risen 20% to 30% since the start of the year because of the memory shortage. A flagship maker can shift a shortage into a foldable's price tag. Thinner margins to begin with leave a budget phone with far less room to hide the same increase.

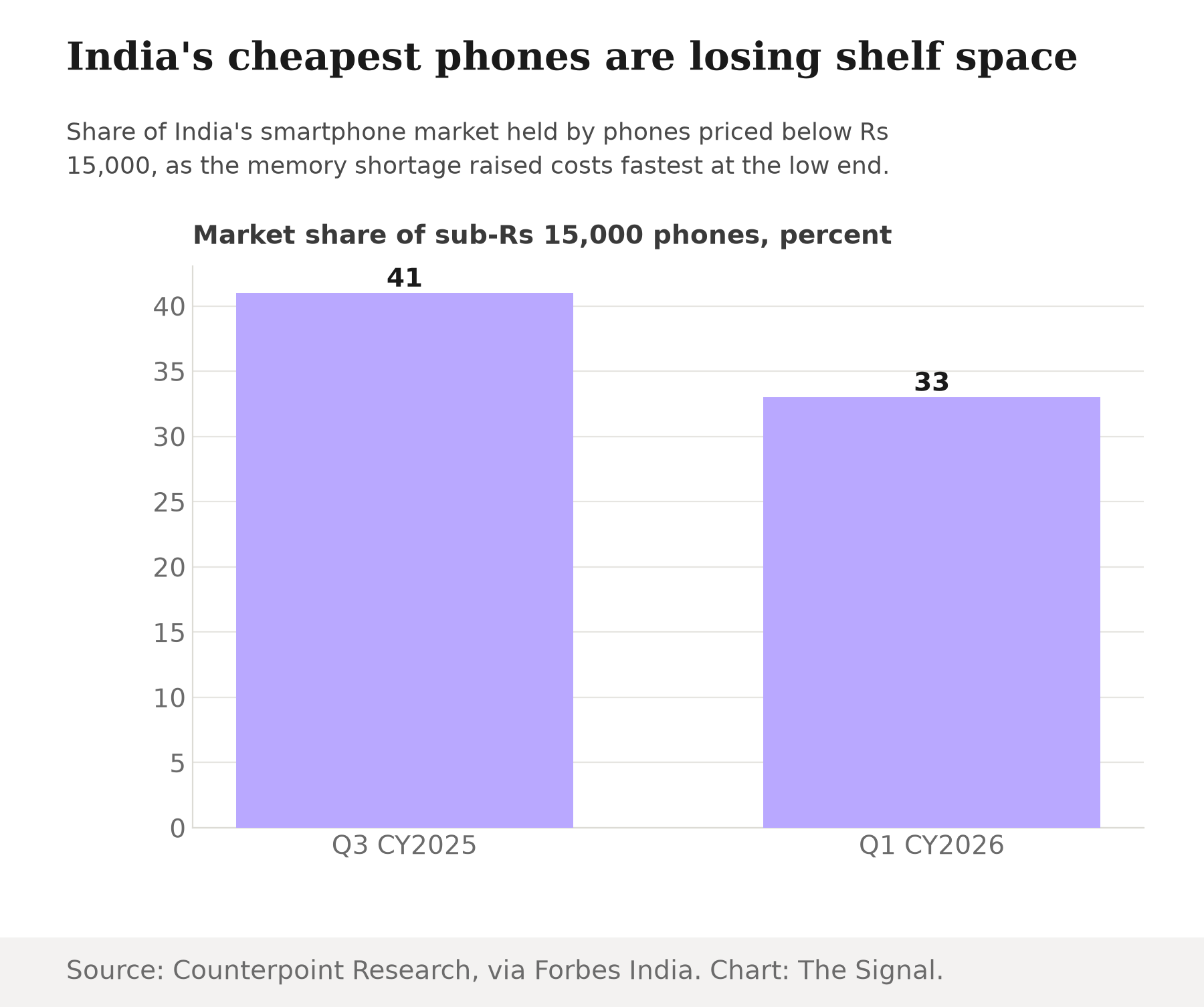

India's cheapest phones are losing shelf space

That squeeze already shows up in India's market data. Counterpoint Research's Tarun Pathak told Forbes India that India's entry-level smartphone segment, phones priced below Rs 15,000, saw its market share fall to 33% in the January-March 2026 quarter, down from 41% in the July-September 2025 quarter, a drop attributed directly to the memory-price squeeze on budget handsets.

India's cheapest phones lost eight percentage points of market share in two quarters.

That shift lands on a manufacturing base India has spent years building for exactly this category of phone. The Ministry of Electronics and Information Technology reports, via a Press Information Bureau release, that the PLI Scheme for Large-Scale Electronics Manufacturing had achieved Rs 11,01,813 crore in cumulative production (136% of target) and Rs 17,519 crore in investment (250% of target) by February 2026, even as domestic value addition in electronics manufacturing remains just 18-20%. The Ministry of Electronics and IT separately reports, via a Press Information Bureau release, that smartphones were India's top exported commodity in calendar 2025, worth $30.13 billion.

| PLI-scheme electronics manufacturing, as of February 2026 | Figure |

|---|---|

| Cumulative production | Rs 11,01,813 crore (136% of target) |

| Cumulative investment | Rs 17,519 crore (250% of target) |

| Domestic value addition | 18-20% of manufacturing value |

| India's top exported commodity, CY2025 | Smartphones, $30.13 billion |

Source: Ministry of Electronics and Information Technology, via Press Information Bureau and a second PIB release.

Taken alone, the production and investment lines make the scheme look like a comfortable success against its own targets. But domestic value addition in electronics manufacturing remains just 18-20% of manufacturing value, meaning most of what goes into an assembled Indian phone is still imported, and memory is one of the components imported most. The 44% and 53% quarter-on-quarter jump in DRAM and NAND prices does not stop at Samsung's factory gate. It raises the landed cost of the same components that go into smartphones, India's top exported commodity in calendar 2025 at $30.13 billion.

The honest objection

The strongest case against reading this as a lasting problem is that Samsung's guidance is one quarter and the mobile division's 2026 figure is still a forecast, not a confirmed result, and memory has always been a cyclical business: prices that spike on a supply crunch can fall just as fast once new capacity comes online, and Samsung's own investors already priced in some of that doubt by selling the stock the same day. On that view, the mobile division's projected fall to around 5 trillion won is a worst-case estimate from one Korean financial outlet, not a certainty, and the India entry-tier share loss could reverse once the shortage eases.

That case has real force, and memory prices have swung hard both ways before. But it does not explain why Samsung's own investors, who see the company's internal cost structure more clearly than any outsider, sold the stock the same day the guidance came out. And it does not change what has already happened to India's sub-Rs 15,000 segment between mid-2025 and early 2026, which is measured history, not a forecast. A cycle that might turn is still the cycle setting prices today.

The Signal

The headline number in Samsung's guidance and the headline number in its own phone division's forecast describe the same shortage from opposite sides of one company's balance sheet. The chip business is charging the mobile business what the market will bear. Watch two things next: whether Samsung's Mobile Experience division actually lands close to that projected 5 trillion won when 2026 closes, and whether India's entry-tier smartphone share keeps falling through the rest of the year. If both happen, the AI memory boom will have proven it can enrich a chipmaker and squeeze its own phone unit, and the country building the phones, inside the very same balance sheet.

Reporting basis: Samsung's Q2 2026 consolidated guidance and its underlying sales and profit figures are per Samsung Electronics' own earnings guidance disclosure. The DRAM and NAND price data is Citi Research's estimate, as reported by Reuters and carried by WHBL. Samsung's share-price reaction is per CNBC's own reporting. The Device Solutions division's Q1 2026 profit share is per Samsung's own earnings release, as reported by The Elec. The Galaxy Z Flip8 pricing leak is per The Korea Herald, citing the outlet Bloter. The Mobile Experience division's 2025 profit and 2026 forecast are per SamMobile, citing a report from the Korean outlet FNNews, and rest on that single financial-press source. The global smartphone price forecast and budget-phone cost data are Counterpoint Research's figures, as reported by CNBC. India's entry-tier market-share data is Counterpoint Research's figures, as quoted by its analyst Tarun Pathak to Forbes India. The PLI-scheme production, investment, value-addition and export figures are from the Ministry of Electronics and Information Technology, via two separate Press Information Bureau releases. The percentage decline in Samsung's mobile division profit and the percentage-point drop in India's entry-tier market share are The Signal's calculations from those figures.