WhatsApp, used by more than three billion people worldwide, said on June 30, 2026 that it would let users go by a reserved username instead of a phone number, closing what it called a longstanding privacy gap. On its face this reads as a plain upgrade: message a stranger, a delivery agent or a customer-support account without handing over the number that many other services also use to check who you are.

It is worth slowing down on that pitch. India's IT ministry did not treat the announcement as routine. MeitY sent Meta a formal notice on July 1, 2026, giving it three days to respond and to halt the usernames rollout in India until the government is satisfied. A single day between a global product update and a formal government notice is not how India usually treats an opt-in feature.

The notice's complaint was specific: usernames could let scammers reach victims without ever showing a phone number. MeitY warned that the feature could materially increase online fraud, phishing, digital arrest scams and impersonation attacks by allowing bad actors to contact victims without disclosing their phone numbers.

The number behind the warning

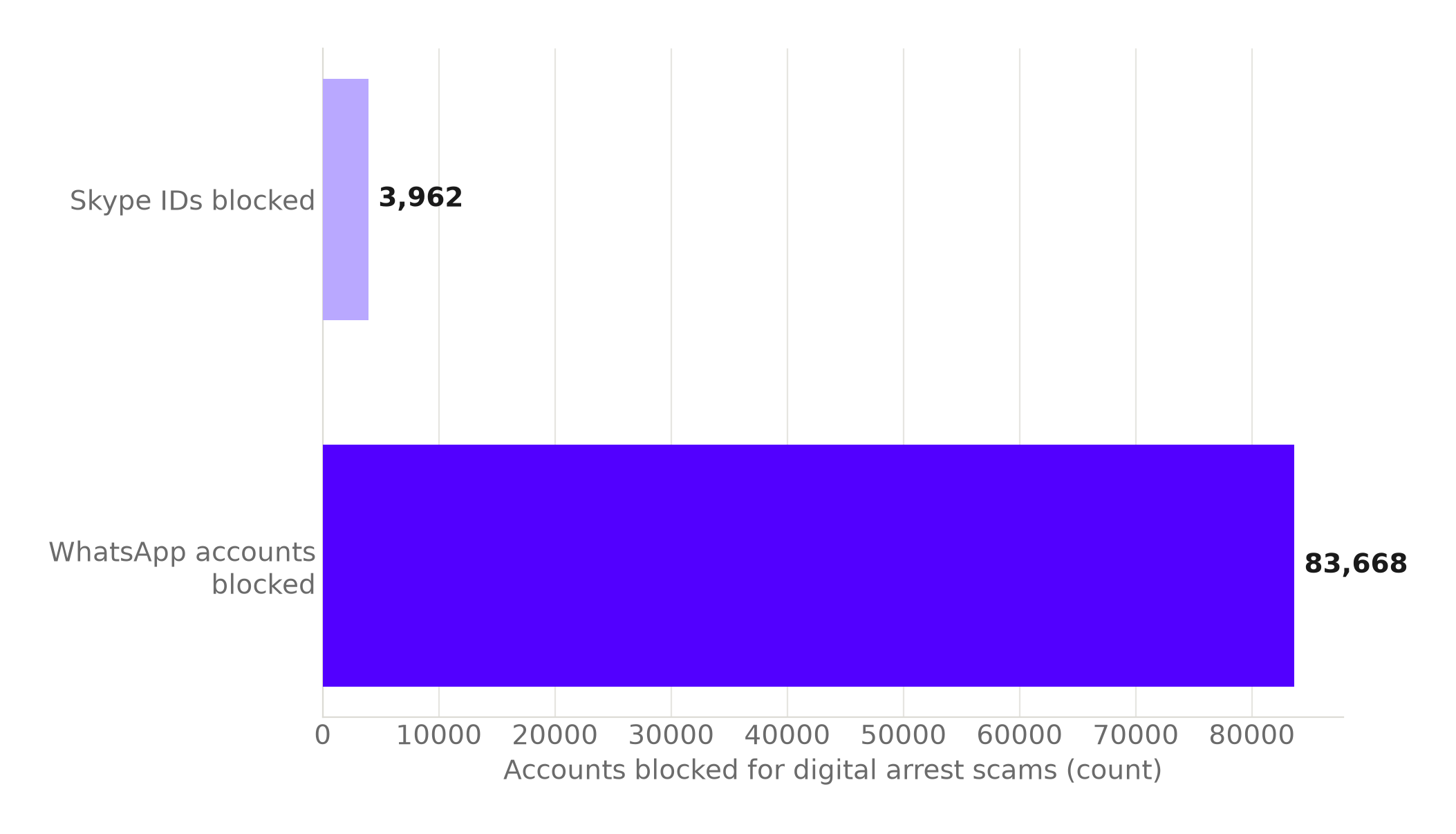

That warning is not abstract. India's Cybercrime Coordination Centre, known as I4C, has already proactively identified and blocked more than 3,962 Skype IDs and 83,668 WhatsApp accounts used for so-called digital arrest scams, the con in which a caller poses as a police officer or an investigator and threatens a victim with imminent arrest unless they pay immediately.

WhatsApp accounts already outnumber Skype IDs blocked for this single scam by about 21 times.

Both figures come from that same government reply, covering the same scam type. Whatever platform scammers turn to next, WhatsApp is already carrying the larger share of blocked accounts today.

Source: Ministry of Home Affairs, reply to the Lok Sabha. The 21-times comparison is The Signal's calculation from these figures. Chart: The Signal.

Why a phone number is not just a contact method

The reason a username threatens more than convenience is that India's fraud-detection systems are built to key on the number itself, not the account sitting behind it. The Department of Telecommunications runs a Financial Fraud Risk Indicator that scores a mobile number as Medium, High or Very High risk of financial fraud. It shares that score with banks and UPI providers in real time. The Reserve Bank of India's own KYC rules require that the mobile number used for Aadhaar-based e-KYC match the number already on file with the bank, specifically to prevent fraud.

Both systems assume a flagged number stays traceable across whatever app it turns up in next. A username breaks that assumption inside WhatsApp itself: the ten traceable digits become optional. The number a bank or a telecom operator has already scored is no longer the same thing a stranger sees on the other end of a chat.

The scale of what's being defended

India already runs a large, active machine for freezing this exact kind of fraud.

| Metric (as of October 31, 2025) | Figure |

|---|---|

| Complaints logged with the fraud reporting system | 23.02 lakh |

| Financial amount saved | ₹7,130 crore |

| SIM cards blocked | 11.14 lakh |

| IMEIs blocked | 2.96 lakh |

Source: Ministry of Home Affairs, press release. Table: The Signal.

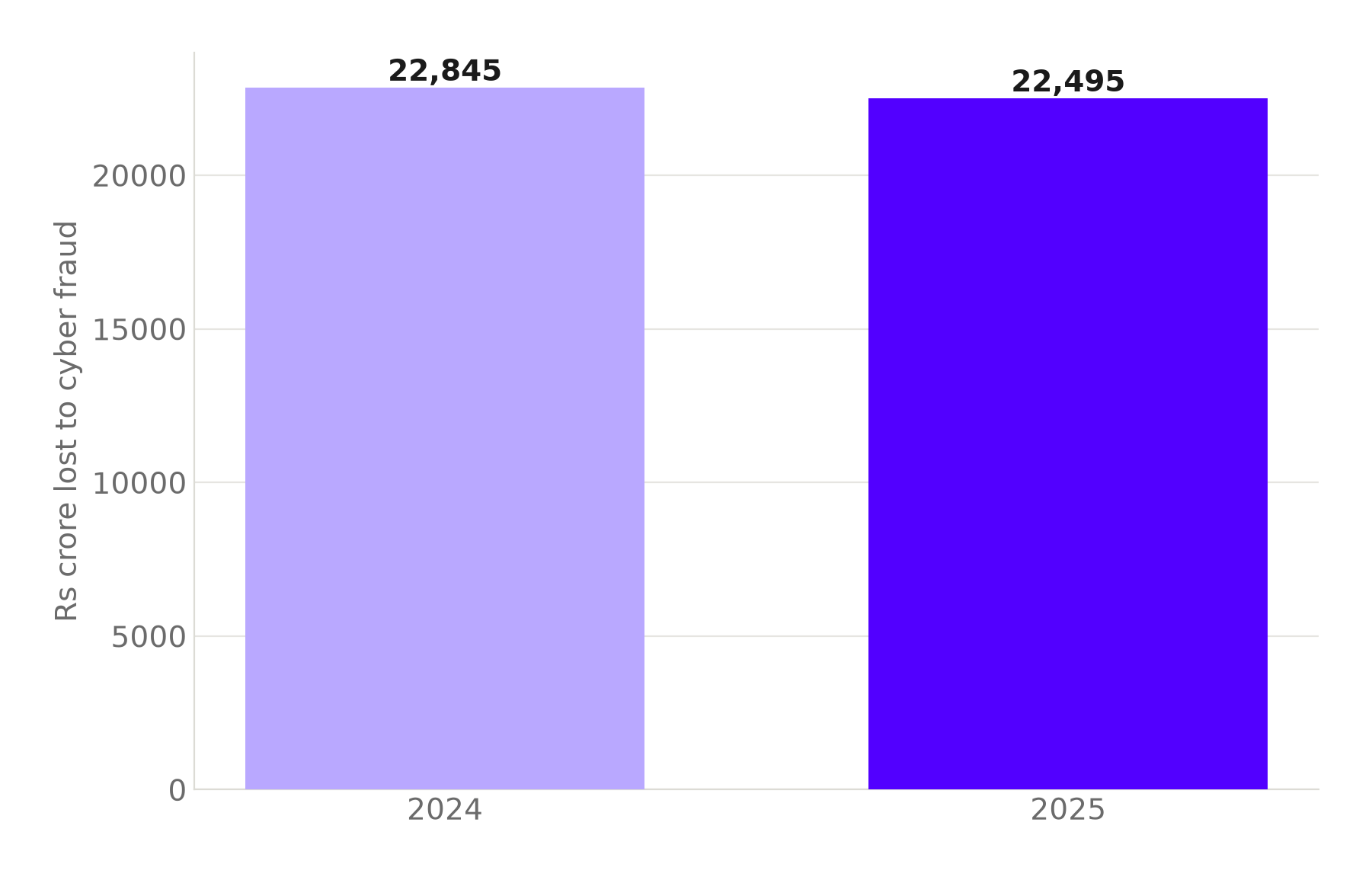

Even against that machinery, the fraud has not shrunk. Indians lost ₹22,495 crore to cyber fraud in 2025, compared with ₹22,845 crore in 2024, essentially flat rather than falling.

Source: ThePrint, citing Ministry of Home Affairs data. Chart: The Signal.

The honest objection

The strongest case against MeitY's intervention is that a username does not, on its own, manufacture a scam. Someone impersonating a bank employee or a police officer over WhatsApp already does so from an ordinary phone number today; the con works because of what the caller says and how urgently they say it, not because a victim can see ten digits on a profile. On this reading, the government is regulating the feature that is easiest to point to, not the trick that actually persuades someone to transfer money.

That case is about how the scam is pulled off. It says nothing about how the scam gets caught, and banks and telecom regulators have wired the number itself deep into that side. The Department of Telecommunications and the Reserve Bank of India have both built their fraud-scoring and KYC-matching machinery on top of a traceable phone number. Peel that number away from a chat account, and the link between a conversation and that machinery breaks. The objection is right that a username alone cannot invent a con. It is silent on why the government would want to remove the one thread that already connects a WhatsApp conversation back to a number banks and telecom operators can already check.

The Signal

This is not, at bottom, a privacy dispute. It is a collision between a design decision made for a global user base and a domestic fraud-detection system built entirely around one identifier: the phone number. WhatsApp's proposal treats that number as a liability to be made optional. India's banks, its telecom regulator and its cybercrime unit treat the same number as the anchor that makes a scammer traceable at all. Watch what Meta actually changes after the three-day window closes. If usernames roll out in India with the phone number still visible by default, and hiding it costs real convenience, the fraud-defense architecture holds. If the anchor becomes optional for whoever wants it that way, the next digital arrest scam gets a little harder to trace back to anyone at all.

Reporting basis: WhatsApp's usernames announcement is per Al Jazeera's report of June 30, 2026. MeitY's notice to Meta and its three-day deadline are per The Register. The notice's specific fraud, phishing, digital-arrest-scam and impersonation language is per Forbes, quoting the notice directly. The Skype and WhatsApp account-blocking figures are from the Ministry of Home Affairs' written reply to the Lok Sabha. The Financial Fraud Risk Indicator is per the Department of Telecommunications' own press release. The Citizen Financial Cyber Fraud Reporting and Management System's savings, complaint and SIM/IMEI-blocking figures, current as of October 31, 2025, are from a separate Ministry of Home Affairs press release. The 2025 and 2024 cyber fraud loss figures are per ThePrint, citing Ministry of Home Affairs data, and are not independently re-verified beyond that account. The KYC mobile-number-matching rule is from the Reserve Bank of India's own FAQ document. The 21-times comparison between blocked WhatsApp accounts and Skype IDs is The Signal's calculation from the Lok Sabha reply figures above; every other figure is as stated by the sources named.