By the numbers coming out this year, India looks like it is racing ahead on AI. The Union Cabinet has approved the IndiaAI Mission with a Rs 10,371.92 crore budget, a plan built around acquiring more than 10,000 GPUs through public-private partnership. HCLTech has just signed a $1.14 billion AI-led digital transformation deal with a European Fortune Global 50 firm, its largest contract since the $2.1 billion Verizon deal in August 2023. And India's global capability centres, or GCCs, have scaled to 2,117 centres generating $98.4 billion in revenue and employing 2.36 million professionals, according to the Zinnov-Nasscom India GCC Landscape Report 2026. Read the headlines and the country is building an AI power base.

It is worth slowing down on what that money is actually buying. The IndiaAI Mission's own quote is explicit about what it funds: over 10,000 GPUs will be acquired through public-private partnerships, compute capacity, not a foundation model. HCLTech's $1.14 billion contract is not for a product HCLTech built and sells; it commits HCLTech to help the client establish an AI-driven operating model to manage its digital workplace and networks, someone else's AI, run on HCLTech's labour. And the GCC number reflects the world's largest companies running their AI programmes out of India, not India selling AI to the world.

India's AI economy is priced in billions of dollars. Its frontier-model spending is priced in crores of rupees.

That contrast is the story: not whether India has an AI industry, but what kind.

The GCC mandate is real, and it is someone else's mandate

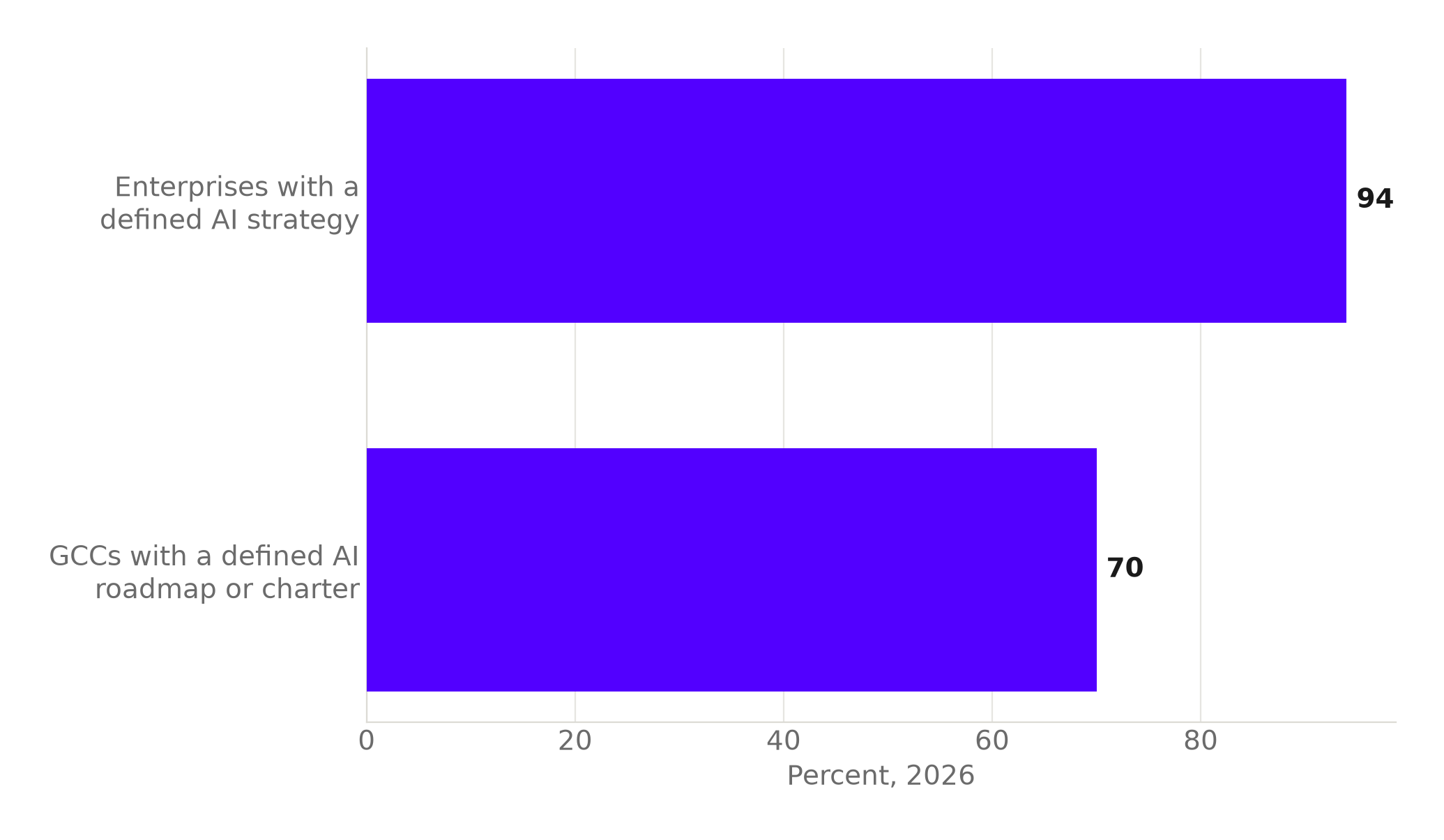

The GCC data is not a footnote. India's GCCs span 2,117 centres across 3,728 units, generating $98.4 billion in revenue and employing 2.36 million professionals, a scale few countries can match for enterprise technology delivery. And that scale is increasingly an AI scale specifically. 94% of enterprises now have a defined AI strategy, and 70% of India's GCCs already have a defined AI roadmap or charter in place, according to the Zinnov-Nasscom-Tiger Analytics GCC AI Maturity Study.

The line between the two numbers is the point: the AI strategy belongs to the global parent, and the GCC is where it gets built and run.

Source: Zinnov-Nasscom-Tiger Analytics GCC AI Maturity Study. Chart: The Signal.

A GCC executing someone else's AI roadmap is a different business from a lab building one: a high-value, fast-growing, genuinely skilled delivery business, where the mandate, the model architecture and the intellectual property sit with the parent company issuing the charter, not with the centre in Bengaluru or Hyderabad carrying it out.

Where the big dollar numbers actually go

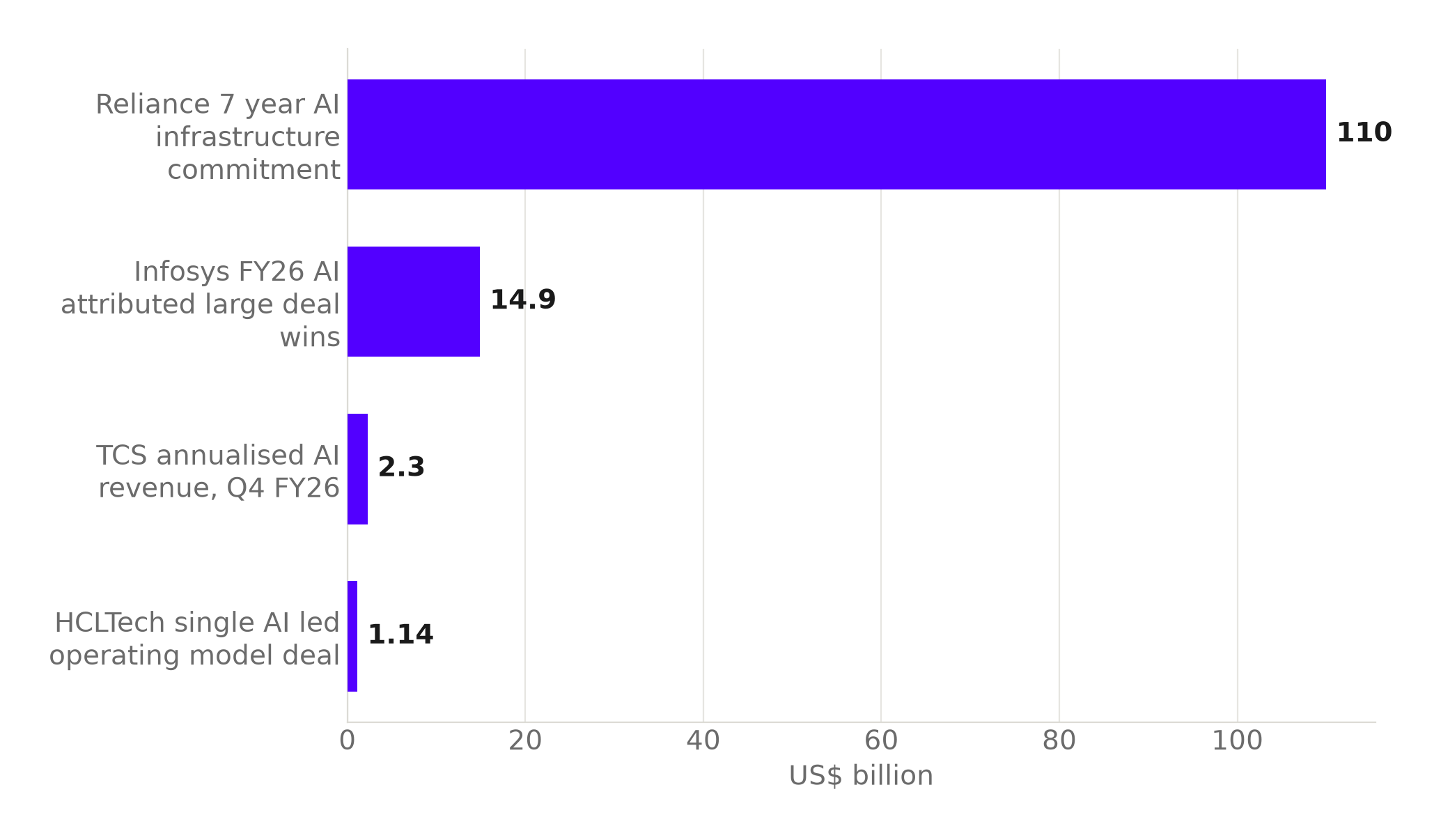

Follow the dollar figures through 2026 and every one of them sits on the delivery side of that line. Reliance is committing roughly $110 billion over seven years to AI data centres, edge computing and Jio-integrated AI services, infrastructure and distribution, not a foundation-model research programme. Infosys posted $14.9 billion in large deal wins for FY26, which the company attributes to its enterprise AI proposition: servicing client adoption, not fielding a model of its own. TCS's annualised AI revenue crossed $2.3 billion in the fourth quarter of FY26, money earned deploying AI inside client operations. And HCLTech's single largest AI deal of the year is worth $1.14 billion, an operating-model contract, not a licence to a proprietary system.

Every large AI dollar figure out of India Inc in 2026 is servicing revenue or infrastructure spend, not model-building capital.

Four different companies, four different deal structures, one identical shape: dollars in, delivery out.

Source: TechCrunch; The Globe and Mail; Forbes India; The Star. Chart: The Signal.

Reliance's number alone dwarfs the other three combined, and it still is not frontier-model capital. It is data centres, edge compute and a telecom-integrated AI service layer, the physical and distribution backbone a model needs, not the model.

What frontier spending actually looks like

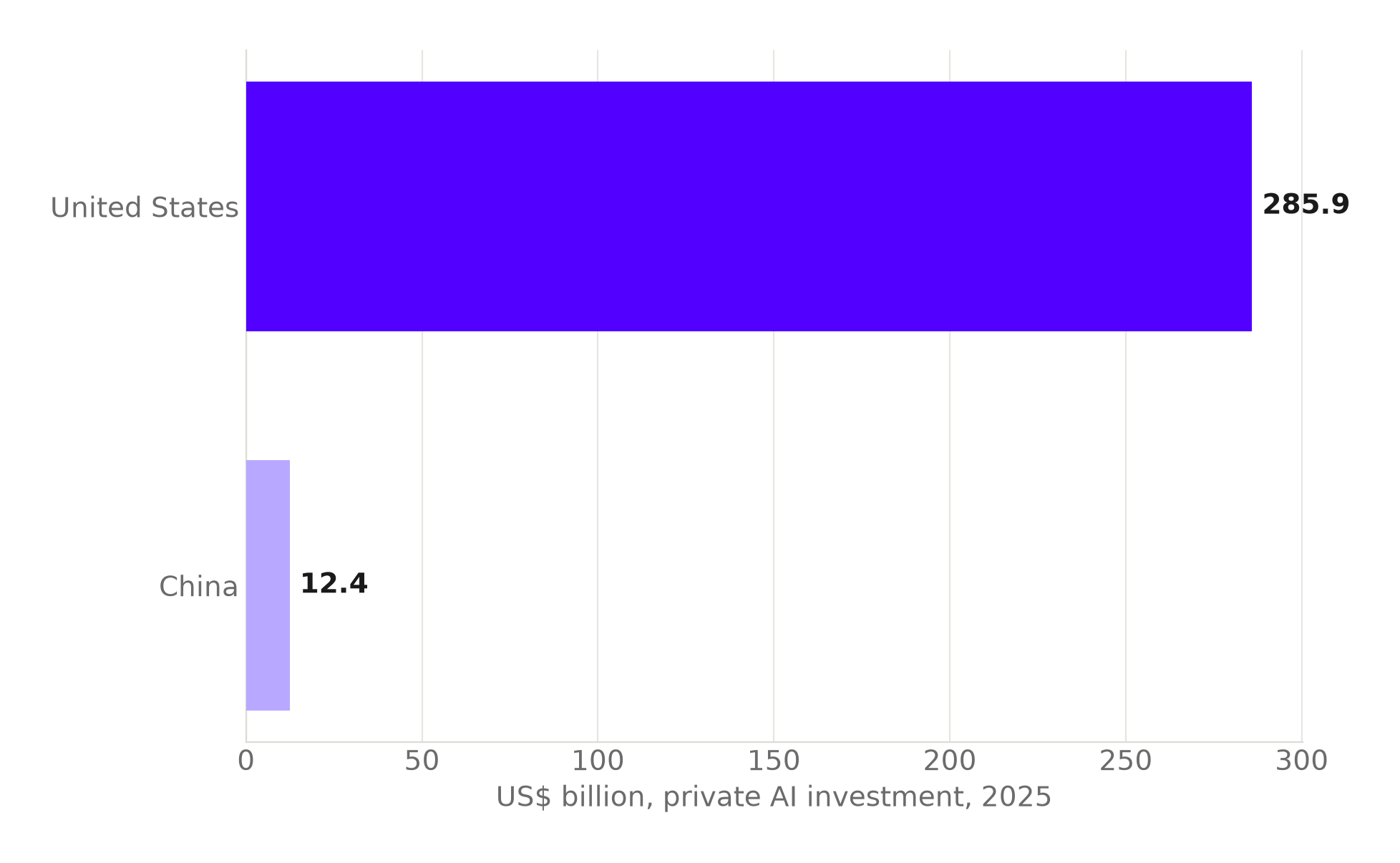

For comparison, look at where money is actually going into building frontier systems. US private AI investment reached $285.9 billion in 2025, more than 23 times the $12.4 billion invested in China, according to Stanford HAI's 2026 AI Index Report. Those are national totals for private capital chasing frontier model development and the compute to train it. India's equivalent government commitment, the IndiaAI Mission, is a national infrastructure programme denominated in rupees: Rs 10,371.92 crore to acquire GPU capacity through public-private partnership, built explicitly to buy compute access rather than fund a model of India's own. Converted at roughly ₹95.34 to the dollar, that budget is about $1.1 billion. That is smaller than any single one of the AI dealflow figures India Inc booked this year, let alone the $285.9 billion the US alone put into frontier AI.

Source: Stanford HAI, 2026 AI Index Report. Chart: The Signal.

The gap between the United States and China is itself a 23-fold spread among the two countries actually funding frontier labs. India is not a third bar on that chart. It is not competing in that race yet; it is supplying the workforce and the compute-buying budget for a market where other countries and other companies own the model.

The honest objection

The strongest case against calling this a gap is that GPUs come before models, not after. The IndiaAI Mission's own stated purpose is acquiring more than 10,000 GPUs through public-private partnership, and no country builds a frontier model without first securing the compute to train one. On this reading, India's conglomerates and IT majors are making the rational sequencing choice: bank the delivery revenue and infrastructure returns available today, while the compute base the IndiaAI Mission is buying gets built underneath. TCS, Infosys and HCLTech are cash-generative precisely because they serve global AI adoption at scale, and that cash is what would fund a frontier bet later, if one comes.

That case is real, and compute scarcity is genuinely the binding constraint everywhere. But sequencing an eventual model behind today's delivery revenue is a choice about capital allocation, not a law of technology, and the size of the gap says something about which choice is actually being made. A national compute-acquisition budget denominated in a few thousand crore sits next to a set of India Inc AI deals and commitments each individually running into the billions of dollars, and none of that private capital is being redirected toward a foundation-model programme of its own. Compute-first sequencing explains a slow start. It does not by itself explain a decade of companies with the cash choosing servicing over building, deal after deal, without the pattern ever tipping.

The one concrete counter-example only sharpens the point. Sarvam AI trained a 105-billion-parameter foundation model from scratch on compute provided under the IndiaAI Mission, the most concrete domestic frontier attempt on record. It came from a venture-backed startup running on subsidised government GPUs, not from Reliance, TCS, Infosys or HCLTech redirecting a fraction of their AI dealflow into a model of their own.

The Signal

The GCC and IT-services numbers are not evidence that India is falling behind on AI. They are evidence of what India has chosen to be good at: running other companies' AI programmes better than almost anyone else can, at a $98.4 billion GCC-revenue scale that most countries would envy. But running the mandate is not owning it. The intellectual property, the model weights and the pricing power that come from fielding a frontier system sit wherever the model is built, and by every dollar figure in this year's deals, that is not India. Watch what the IndiaAI Mission's GPU procurement actually enables over the next few years: if it seeds a domestic frontier attempt, the gap starts closing. If it just lowers the cost of doing more delivery work, India's AI economy stays exactly what it is today, indispensable to everyone else's model, and the owner of none.

Reporting basis: the IndiaAI Mission's Cabinet approval and budget figure are per DD News, the government's own broadcaster, covering the Cabinet decision directly. The GCC landscape figures (centre count, units, revenue, talent) are from the Zinnov-Nasscom India GCC Landscape Report 2026, and the enterprise and GCC AI-maturity percentages are from the related Zinnov-Nasscom-Tiger Analytics GCC AI Maturity Study, both industry compilations rather than official statistics. The HCLTech deal is per The Star, carrying a Reuters wire account. The Reliance AI investment plan is per TechCrunch, citing Reliance's own announcement. TCS's AI revenue figure is per Forbes India's account of TCS's Q4 FY26 results, and Infosys's large-deal figure is per an Infosys results announcement carried by The Globe and Mail. The United States and China private AI investment figures are from Stanford HAI's 2026 AI Index Report. The Sarvam-105B detail is per TechCrunch's reporting on the model's launch, and the rupee-dollar conversion of the IndiaAI Mission budget uses the USD/INR exchange rate reported by Trading Economics on July 3, 2026, which is The Signal's own calculation from that reported rate. No other figure in this piece is The Signal's own calculation; each of the rest is stated as its source reported it.