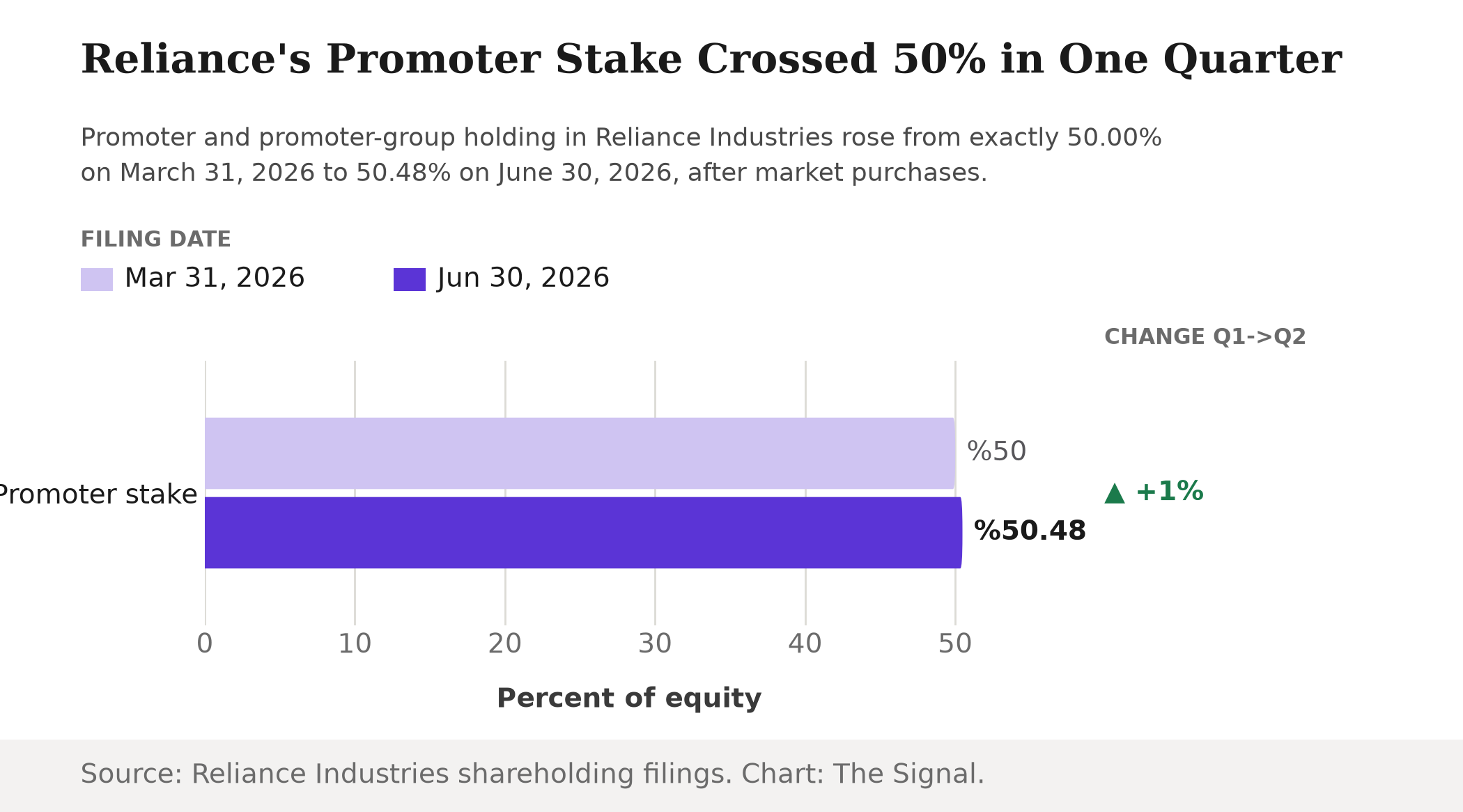

Reliance Industries' promoter and promoter group holding rose to 50.48% of equity as on June 30, 2026, according to the company's own regulatory shareholding filing. Market analysts estimate the group's market purchases that quarter cost roughly Rs 8,500-9,000 crore. The reading in the market has been straightforward: India's largest listed company's founders just wrote a very large cheque to buy more of their own stock, and that is what confidence looks like.

It is worth slowing down on that. The same filing that reads as a confidence signal also feeds the formula Nifty and MSCI use to decide how much of Reliance passive funds must hold, and that formula does not care about confidence at all.

Reliance's promoter stake crossed 50 percent for the first time this quarter.

Three months earlier, as on March 31, 2026, the same holding stood at exactly 50.00%. The rise to 50.48% is a jump of 0.48 percentage points in a single quarter, and it means promoters now legally control more than half of every share Reliance has issued.

The rule that let them do it

Promoters buying more of their own listed company is not automatically allowed in India. SEBI's takeover rules bar a promoter who already holds 25% or more of a company from acquiring more than an additional 5% of voting rights in a single financial year without making a mandatory open offer to all other shareholders. Reliance's promoters used a sliver of that allowance: 0.48 percentage points against a 5-percentage-point yearly ceiling.

They also stayed well clear of the other wall in the room. Every listed Indian company must keep public shareholding at a minimum of 25% of equity, which puts a hard ceiling of 75% on how much promoters and other non-public holders can own between them. At 50.48%, Reliance's promoters have used up roughly a third of the room the rule leaves them, and this quarter's purchase was legal, disclosed and nowhere near either limit.

| SEBI threshold | What it allows |

|---|---|

| Creeping acquisition cap | Up to 5 percentage points more voting rights per financial year, once a promoter already holds 25% or more, without triggering a mandatory open offer |

| Minimum public shareholding | At least 25% of equity must stay public, capping combined promoter and non-public holding at 75% |

| Reliance's move, June quarter 2026 | Promoter holding rose 0.48 percentage points, to 50.48% |

Source: SEBI, SAST Regulations 2011; SEBI, SCRR 1957 Rule 19A; Reliance Industries shareholding filings.

What an index actually counts as "float"

Nifty 50 and the MSCI India indices do not weight a stock by its full market value. They weight it by the value of shares actually available to ordinary investors, a concept both call free float. NSE Indices' own methodology states that the Investible Weight Factor behind every Nifty constituent's weight is computed from each company's quarterly shareholding pattern, and explicitly excludes shareholding of promoter and promoter group from that computation. MSCI's Global Investable Market Indexes Methodology defines free float the same way: the share of a stock's equity available to international investors after stripping out strategic, promoter-type holdings.

That is the mechanism. Free float is not an opinion anyone forms about a stock. It is a number pulled straight from the same shareholding-pattern filing that just showed Reliance's promoter line rising, with promoter and promoter-group shares excluded by rule, not by judgment. Reliance's promoter and promoter group holding rose from 50.00% on March 31, 2026 to 50.48% on June 30, 2026, so the free float NSE Indices and MSCI compute from that filing shrank by the same 0.48 percentage points, our calculation applying the exclusion rule to those two filings.

A stock's free float shrinks by exactly what its promoters just bought.

That identity holds regardless of why the promoters bought, or what the market thinks the purchase means.

Reliance's size is what makes this matter

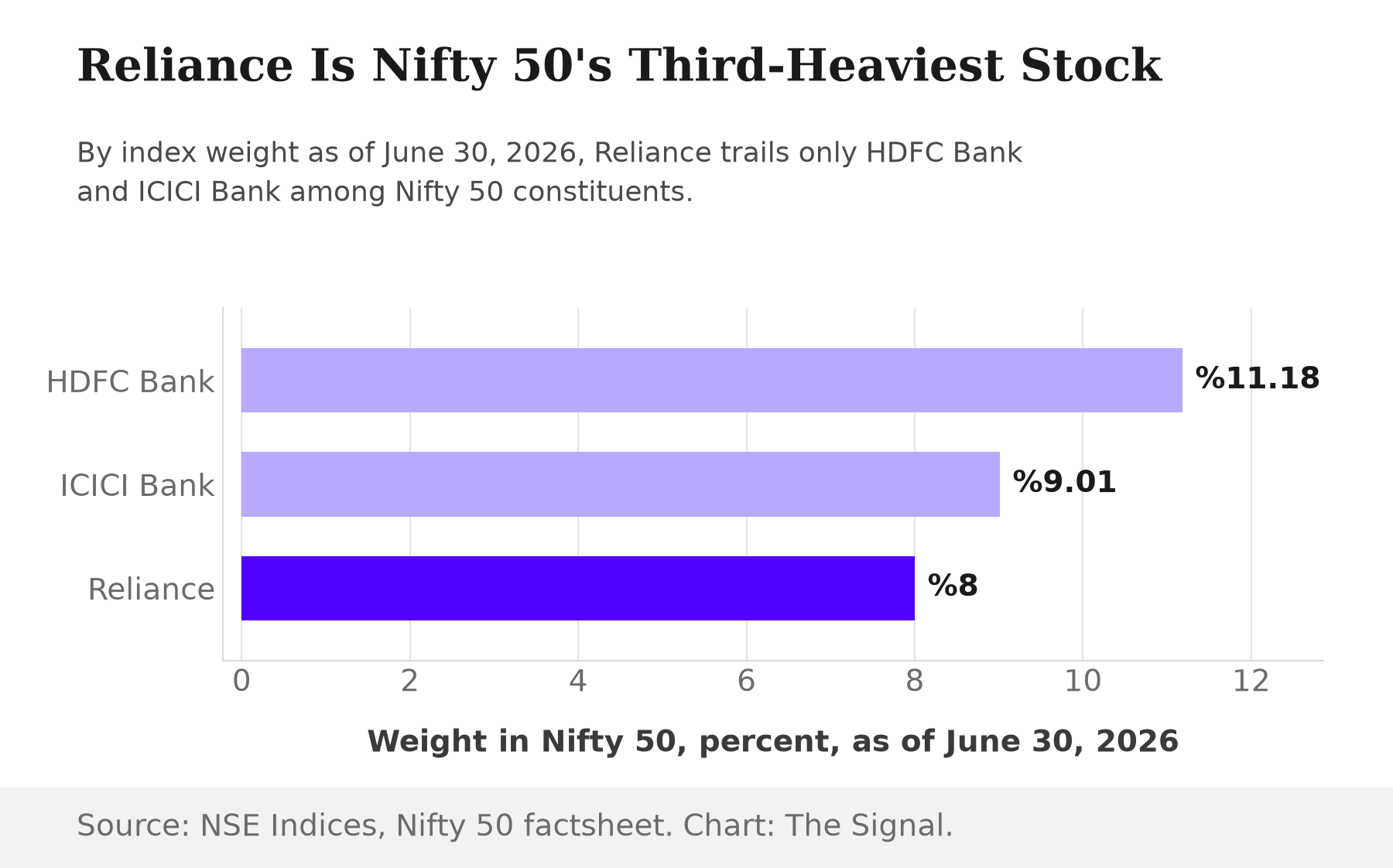

A 0.48-percentage-point float change on a small, thinly tracked stock would be a rounding error. Reliance is not that stock. As of June 30, 2026, Reliance is Nifty 50's third-largest constituent by weight, at 8.00%, behind only HDFC Bank at 11.18% and ICICI Bank at 9.01%. Every rupee-crore fund benchmarked to Nifty 50, and every fund benchmarked to MSCI India, holds Reliance in roughly that proportion by mandate, not by choice.

The timing sharpens it further. NSE Indices rebalances its broad-market indices, including Nifty 50, twice a year, at cut-off dates of January 31 and July 31, using six months of average free-float data ending on that cut-off. Today is July 17, 2026. The next cut-off, July 31, 2026, is two weeks away, and the June 30, 2026 filing showing Reliance's lower free float sits squarely inside the six-month window that review will average over. This is not a hypothetical future rebalancing. It is the one already in motion.

MSCI runs on its own separate clock, and that clock also has a date on it. MSCI's own published Index Review Dates schedule lists its next scheduled Index Review as having an announcement date of August 12, 2026 and an effective date of September 1, 2026, the first MSCI review to fall after the June 30, 2026 filing that shrank Reliance's free float. MSCI India trackers face the same mechanical question on that date that Nifty trackers face on July 31.

The honest objection

The strongest case against reading this as a forced-selling story is that the move is small and the data is thin. A 0.48-percentage-point shift is a tenth of what SEBI's own creeping-acquisition rule permits in a single year, and the semi-annual review averages six months of free-float data, not a single quarter's snapshot. The two filings this piece rests on, from March 31 and June 30, 2026, are two points on that six-month curve, not the whole curve. It is possible the average free float NSE Indices actually applies on July 31 moves by less than 0.48 percentage points, or that other shareholding categories shift enough in the same window to blunt the effect.

That case tempers the size of the move, not its direction. NSE Indices and MSCI do not decide whether to count promoter shares as float; their own published methodologies exclude that category outright, mechanically, from every quarterly recalculation. Whatever the precise number that survives the six-month average, it starts from a lower public share than it did three months earlier, on a stock that is Nifty 50's third-largest constituent, where even a fractional weight change moves real rupees for funds that are contractually required to track the index, not to have a view on Reliance's fundamentals.

The Signal

Reliance's promoters bought their own stock with two audiences in mind and only fully satisfied one of them. To the market reading a Rs 8,500-9,000 crore purchase as conviction, the message landed. The index machinery that decides how much of Reliance passive money must hold reads the same filing differently: a smaller float to work with, recalculated on a fixed semi-annual schedule that does not pause to ask why the number changed. Watch what NSE Indices actually publishes after the July 31, 2026 cut-off. If Reliance's weight holds steady, the six-month averaging smoothed the move away. If it dips, passive funds tracking Nifty 50 and MSCI India will trim a stock whose business did not change at all, purely because its own promoters bought too much of it.

Reporting basis: Reliance Industries' promoter and promoter-group shareholding for June 30, 2026 and March 31, 2026 is from the company's own regulatory shareholding-pattern filings, made under SEBI LODR Regulation 31. The estimated cost of the promoter group's market purchases is per Free Press Journal, citing market analysts, and rests on that single secondary estimate. The creeping-acquisition allowance and the minimum public shareholding floor are from SEBI's SAST Regulations, 2011 and the Securities Contracts (Regulation) Rules, 1957, respectively. The definition and computation of free float are from NSE Indices' own Nifty 50 methodology document and, for the international comparison, MSCI's Global Investable Market Indexes Methodology. Reliance's Nifty 50 weight and the index's semi-annual rebalancing schedule are from NSE Indices' Nifty 50 factsheet. The 0.48-percentage-point shrinkage in free float and the characterization of the July 31, 2026 rebalance as the first to include the June 2026 filing are The Signal's calculations and inferences from those primary documents.