On July 13, 2026, Finance Minister Nirmala Sitharaman asked the chiefs of public sector banks and public financial institutions to intensify their outreach to the NRI diaspora and sustain the momentum of foreign currency mobilisation under the Reserve Bank of India's swap schemes, spanning the FCNR(B), external commercial borrowing and overseas foreign currency borrowing routes. Read on its own, it looks like routine tending of an existing tool. Banks that already sell non-resident Indians fixed deposits are simply being told to sell harder. The scheme itself, in force under a circular dated June 8, 2026, is unchanged: RBI's own FAQ describes it as a plain buy or sell foreign exchange swap from the RBI side, covering only the principal amount of the deposits and not the interest component. Nothing about that instruction, by itself, reads as urgent.

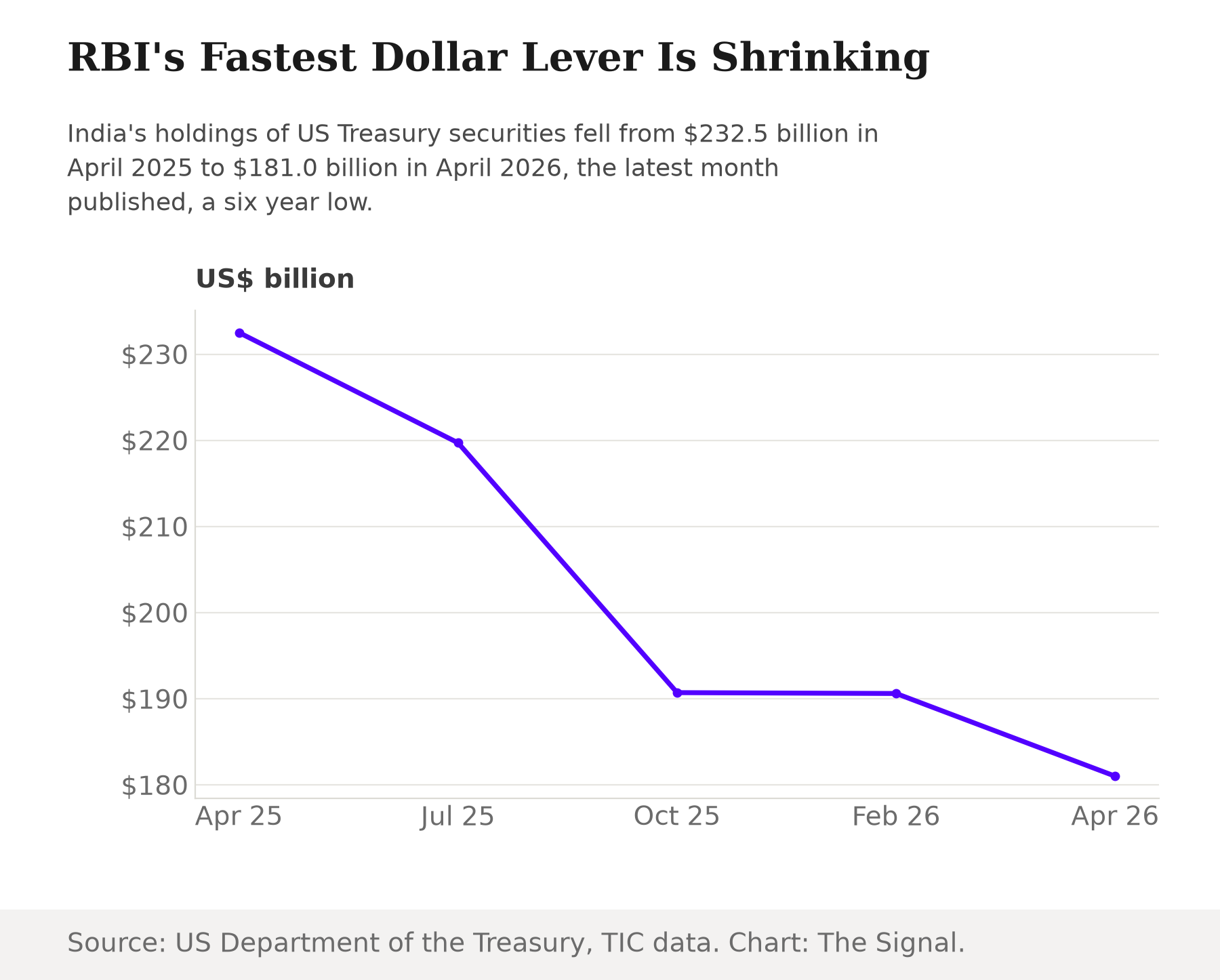

It is worth slowing down on that. The ask did not arrive in a vacuum. The US Treasury's Major Foreign Holders of Treasury Securities table shows India's holdings fell to $181.0 billion in April 2026, the latest month published, down from $232.5 billion a year earlier in April 2025, a decline of about 22 percent and a six year low.

RBI's fastest, most liquid dollar lever just hit a six year low.

US Treasuries are the one reserve asset RBI can sell in an afternoon to raise dollars and defend the rupee. It has not shrunk in one clean move. As the TIC data show, it fell in most months over the past year, a slow bleed rather than a single decision.

Source: US Department of the Treasury, Treasury International Capital (TIC) data. Chart: The Signal.

This is not purely an India story. The same US Treasury data show China's holdings fell about 12 percent over the same year, from $743.6 billion to $651.1 billion, and Brazil's fell about 20 percent, from $212.0 billion to $168.6 billion, while Saudi Arabia's holdings rose about 5 percent, from $133.8 billion to $140.1 billion. Some of the drawdown, in other words, tracks a broader emerging-market drift out of Treasuries. But India's 22 percent decline is still the steepest of that group, well beyond what the shared trend alone would explain. That is why the timing of the diaspora push next to India's own number still carries weight, even after accounting for the wider pattern.

The lever that's thinning

The timing of the diaspora push matters because of what happened the next day. The rupee breached 96 to the dollar for the first time in weeks on July 14, 2026, opening at 96.17, down about 55 paise from its previous close of 95.62, after Brent crude climbed above $85 a barrel on fresh military escalation between the United States and Iran and shipping concerns over the Strait of Hormuz. That chokepoint is not a minor shipping lane. In 2024, oil flow through the Strait of Hormuz averaged 20 million barrels a day, about 20 percent of global petroleum liquids consumption, and flows through the strait in 2024 and the first quarter of 2025 made up more than a quarter of total global seaborne oil trade. India imports most of the oil it uses, so a Hormuz shipping scare that moves Brent moves the rupee almost immediately, and a central bank that wants to lean against that move needs dollars it can deploy fast.

That is precisely the lever that has been thinning for a year. The FM's ask to banks on July 13 landed one day before the rupee cracked 96, five weeks after the June 8 swap circular, and three months after Treasury holdings printed their six year low. Individually, a circular, a ministerial ask and a currency move are three separate events, but stacked on a calendar, they read like a slower lever being pre-positioned just as the fast one runs thinner.

Reaching for a slower, less certain substitute

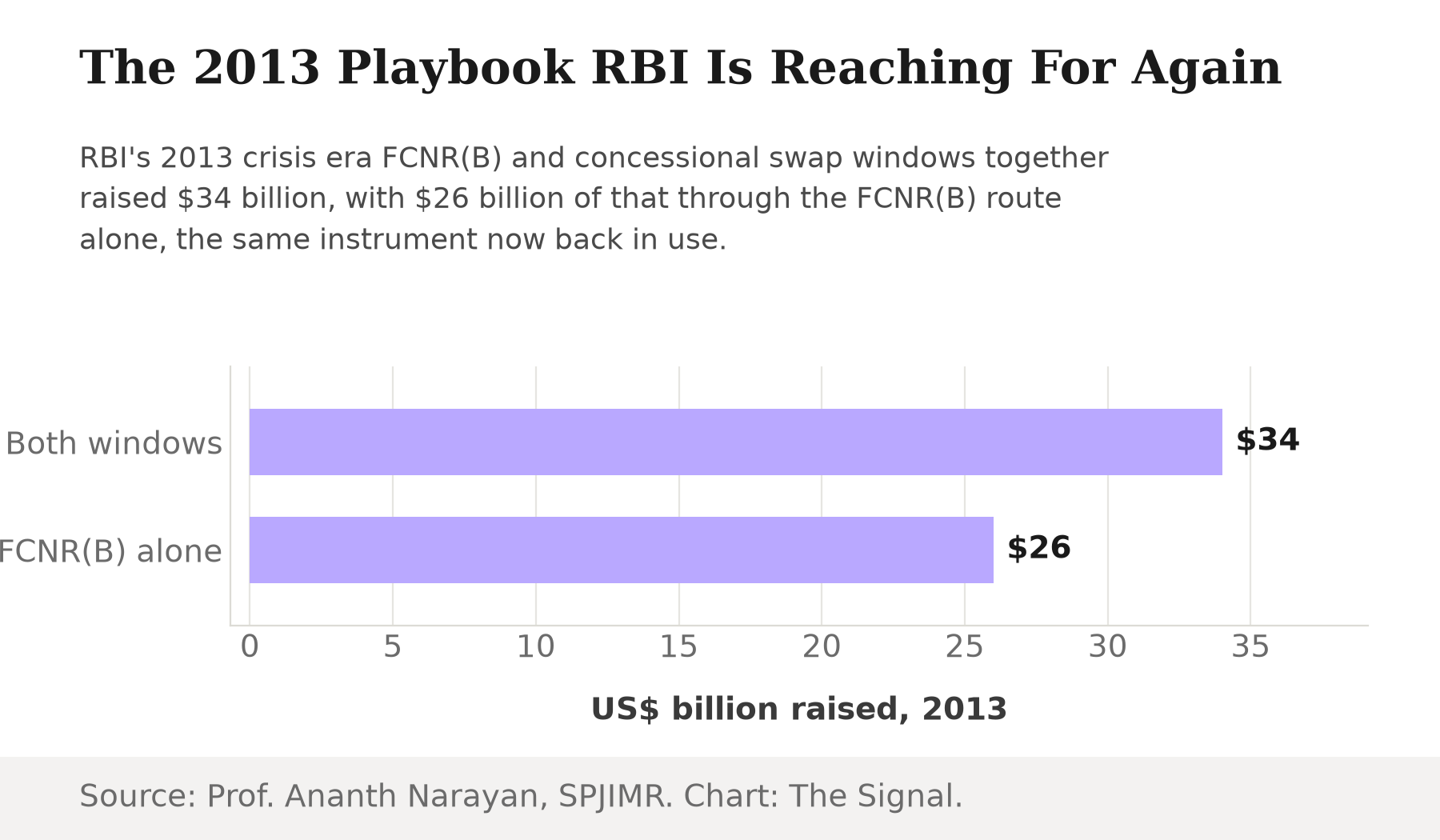

This is not a new idea for RBI. It is closer to the last time this specific tool was used at scale. RBI's 2013 FCNR(B) and concessional swap windows, its crisis era playbook, together raised $34 billion, with $26 billion of that coming through the FCNR(B) route alone, the single largest emergency dollar mobilisation drive in RBI's modern history, run during that year's taper tantrum currency stress.

Source: Prof. Ananth Narayan, SPJIMR. Chart: The Signal.

The instrument now in circular form is the same one. What has changed is the sequencing. In 2013, the FCNR(B) window followed a currency crisis that had already made headlines for weeks. This time, in 2026, the circular came first, in June, before the rupee had cracked 96, while the fast lever was already visibly thinner than a year earlier. Diaspora deposits are also a structurally slower tool than a Treasury sale: RBI can sell a bond in an afternoon, but it cannot sell an FCNR(B) deposit that has not been opened yet. Banks must solicit it, a depositor abroad must choose the swap scheme over an ordinary account, and balances take weeks or months to accumulate at any real scale.

RBI's three dollar levers are moving at three different speeds.

| Lever | Latest figure | As of | Source |

|---|---|---|---|

| US Treasury holdings | $181.0 billion (a six year low) | April 2026 | US Department of the Treasury (TIC) |

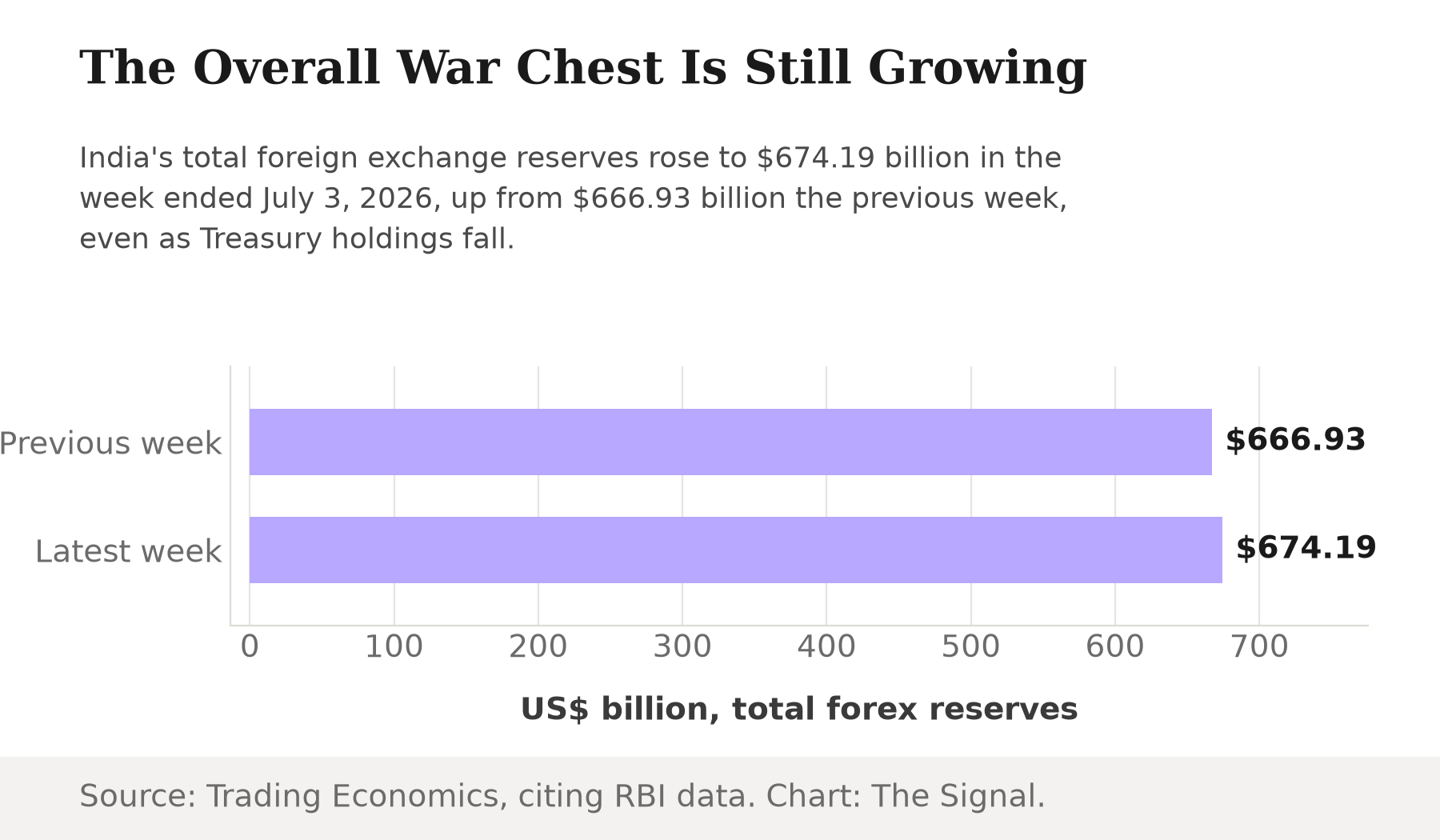

| Total forex reserves | $674.19 billion | Week ended July 3, 2026 | RBI, via Trading Economics |

| Gold reserves | 880.52 tonnes | Q1 2026 | World Gold Council, via Trading Economics |

Sources: US Treasury TIC data; Trading Economics, foreign exchange reserves; Trading Economics, gold reserves.

The honest objection

RBI has already offered its own version of this objection, directly. Governor Sanjay Malhotra said in February 2026 that the swings in reported Treasury holdings are fluctuations on a day to day or week to week basis tied to overall reserve management, and that there is no reduction in RBI's holdings of US Treasuries. That is the central bank's own account, on the record, and it deserves to be taken seriously rather than waved off.

The strongest case against reading any of this as stress is that India's overall reserve position is not shrinking. It is growing. India's foreign exchange reserves rose to $674.19 billion in the week ended July 3, 2026, up from $666.93 billion the previous week, and RBI's gold reserves reached 880.52 tonnes in the first quarter of 2026, up from 880.18 tonnes in the fourth quarter of 2025. A central bank genuinely short of dollars would not usually be adding to gold at the same time it lets a liquid Treasury book run down.

Source: Trading Economics, foreign exchange reserves. Chart: The Signal.

On that reading, the Treasury drawdown is portfolio rebalancing, not distress, and the diaspora push is RBI diversifying its funding sources rather than covering a shortfall. That case is real, and the headline reserve number backs it.

But total reserves and the speed at which a slice of them can actually be deployed are different things. Gold is not an asset a central bank sells at short notice to defend a currency without sending a signal of its own; a Treasury bond is. India's remittance base is large enough to make the diaspora lever plausible: the country received $137.7 billion in personal remittances in 2024, but that is the ordinary annual flow of money migrants send home for families and expenses, not deposits sitting ready at RBI's disposal. Converting a slice of that flow into FCNR(B) balances takes bank solicitation, depositor choice and time to build up. A central bank confident its fastest lever was fine would not need to start recruiting a slower one in the same month its fastest lever hit a six year low.

The Signal

The revealed preference is the tell. RBI never framed the Treasury drawdown as strategy, and this piece is not arguing that it did. What the Finance Ministry did announce, on July 13, one day before the rupee cracked 96, was a push to intensify NRI deposit outreach. That push runs through a facility whose own terms leave RBI absorbing the interest hedge on every dollar it brings in. That is a cost a central bank accepts when the alternative, an emptier fast lever, looks worse. Watch two numbers next. If the Treasury book stabilises or recovers toward last year's levels even as the diaspora campaign continues, this was ordinary diversification. Keep falling instead, with the outreach intensifying and the rupee pinned above 96, and RBI is running its 2013 playbook again, with less of its fastest tool in reserve than the headline number lets on.

Reporting basis: India's US Treasury holdings are from the US Department of the Treasury's Treasury International Capital (TIC) system. The FCNR(B) swap facility's terms are from the Reserve Bank of India's own published FAQ. The Finance Minister's July 13, 2026 instruction to bank chiefs is per a Ministry of Finance press release, as reported by Asian News International. The July 14, 2026 rupee and oil move is per NewsDrum's market report. Weekly foreign exchange reserves and quarterly gold reserves are Reserve Bank of India and World Gold Council data respectively, as compiled by Trading Economics. The 2013 FCNR(B) swap window total is per Prof. Ananth Narayan's account on SPJIMR's blog, the only source for that figure. India's 2024 remittance total is World Bank data. The Strait of Hormuz oil-flow figures are from the US Energy Information Administration. The 22 percent year-on-year decline in Treasury holdings is The Signal's calculation from the TIC figures.