SBI Funds Management opens its IPO on July 14, closing July 16, with a price band of ₹545 to ₹574 a share and a total issue size of ₹11,692.91 crore. It is entirely an offer for sale of up to 20.37 crore shares by its promoters, State Bank of India and Amundi India Holding, so the company itself collects nothing from the listing. The business being sold is India's largest, by a wide margin: SBI Funds Management holds a 15.4 percent share of industry assets, with quarterly average AUM of ₹12,487.9 billion as of December 2025, growing 12.1 percent year on year. The prospectus is explicit about where that scale comes from: parent SBI's 23,125 branches and more than 96.5 million customers as of December 2025, India's largest bank distribution footprint by far. Read only that far, and the pitch is simple: buy a piece of the biggest fund manager in the country, sold through a network no rival can replicate.

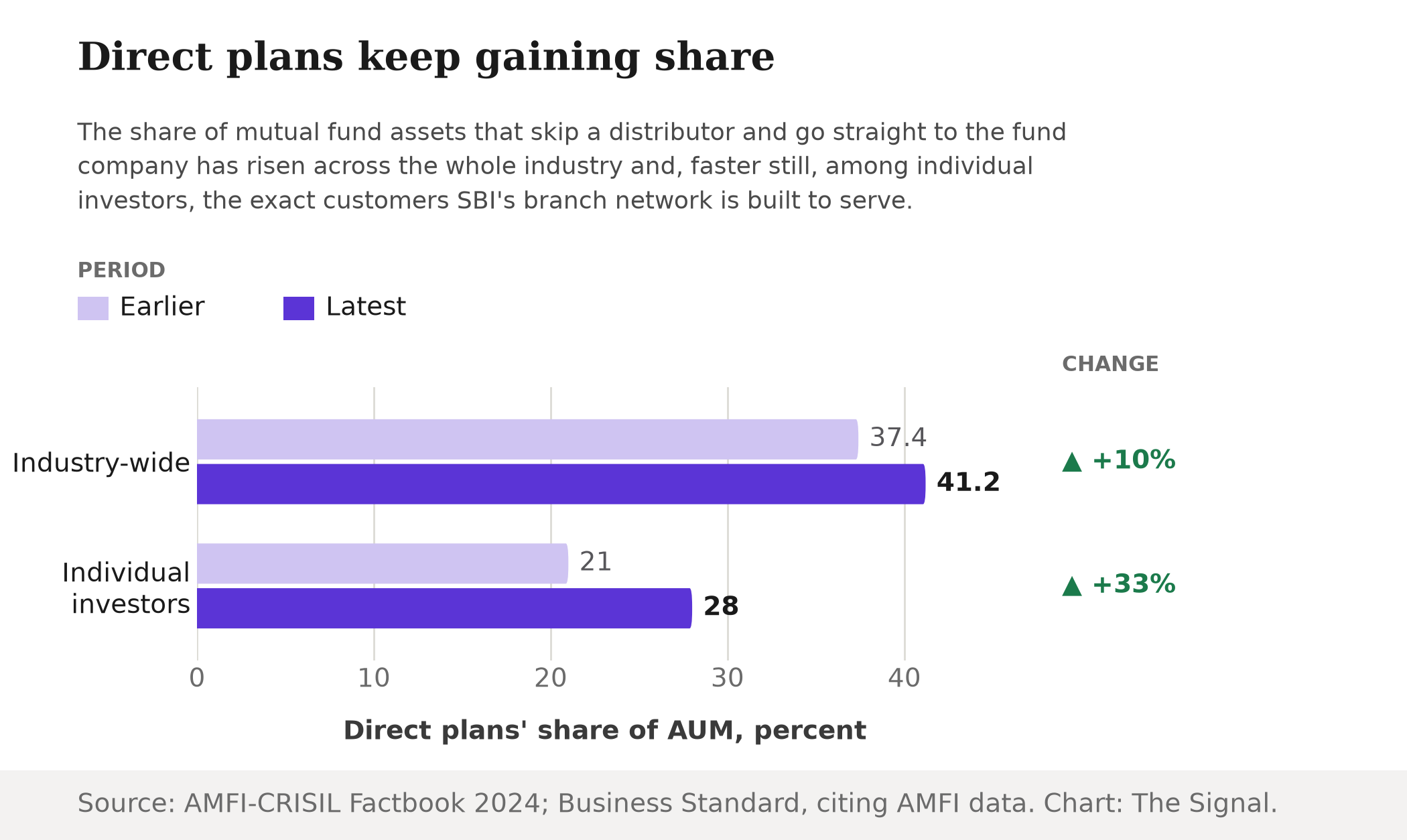

It is worth slowing down on that pitch. The precise thing being monetized, the ability to sell mutual funds through a bank branch and earn a distributor's cut for doing it, is losing ground every year AMFI publishes new numbers. By November 2025, 28 percent of individual investors' mutual fund assets sat in direct plans, up from 21 percent at the start of 2024, a shift measured across exactly the retail customers SBI's branches are built to serve. A direct plan is bought straight from the fund company's own site or app, no distributor involved and no commission paid out of the investor's return. Every rupee that moves from a regular plan to a direct one is a rupee where SBI's branch network stops earning anything extra for having sold it.

The moat SBI is selling

The DRHP is not shy about the source of SBI Funds Management's edge. Its case for scale rests on SBI, established in 1806, being India's largest bank by advances, deposits, and branch network, a reach smaller rivals cannot buy their way into quickly. Paired with a 15.4 percent share of industry AUM and 12.1 percent year-on-year growth, that is a genuinely dominant, genuinely growing business. And because the IPO is a pure offer for sale by SBI and Amundi, the price the market puts on that moat this month has no bearing on the company's own balance sheet. It changes only what the two sellers walk away with.

The customers going around the branch

That is exactly why the direct-plan trend matters more than a single quarter's number. It is not new, and it is not slow. Across the whole industry, direct plans' share of aggregate AUM rose from 37.4 percent in March 2019 to 41.2 percent in March 2024, a five-year climb through a period when SBI Funds Management itself was gaining assets. Narrow the lens to individual investors, SBI's core constituency, and the shift is sharper still: direct-plan AUM for individual investors grew 43.5 percent in 2025, more than triple the 11 percent growth in regular plans. Both trends point the same direction, on two different denominators, and both are AMFI's own published figures.

New entrants are still tiny, but fast

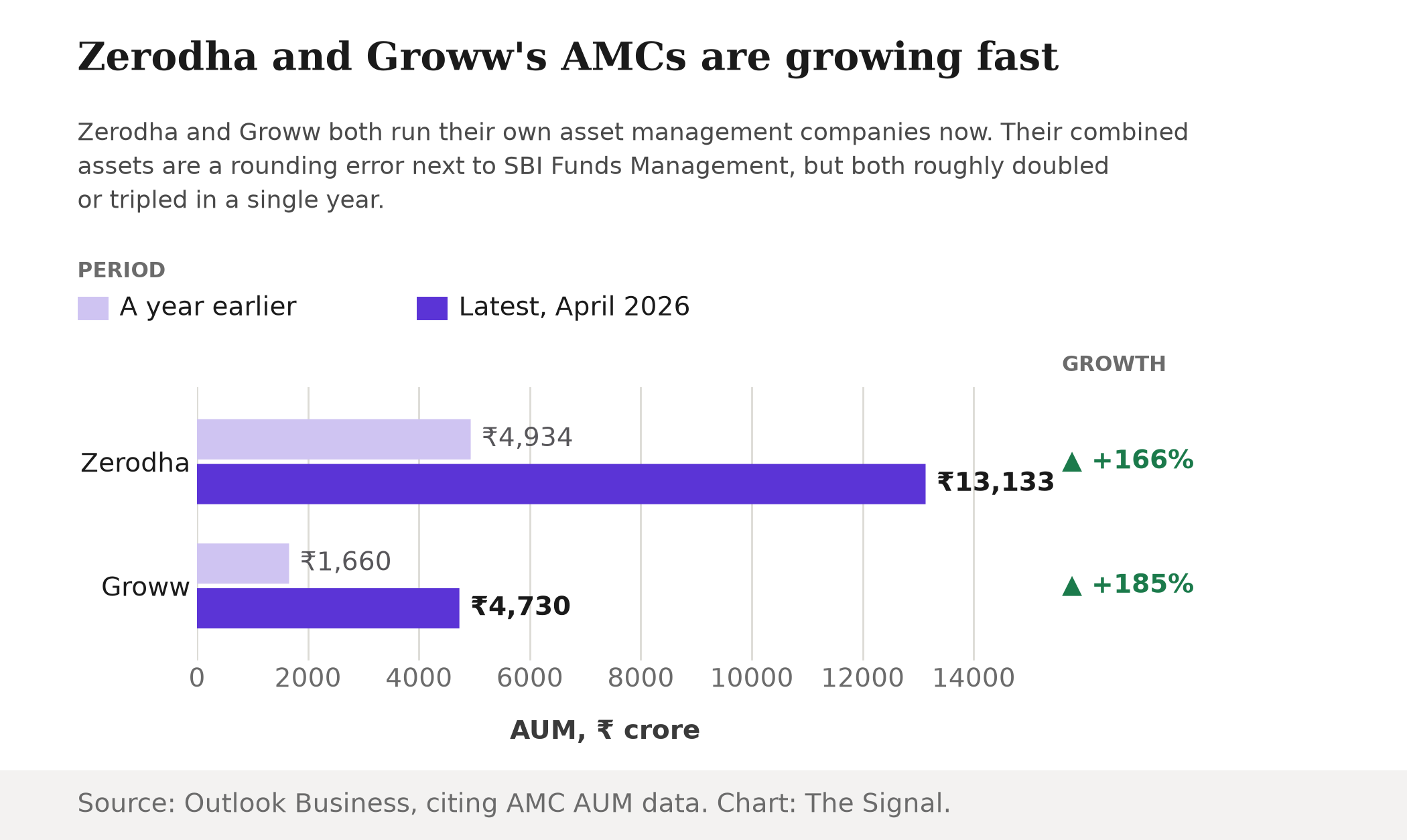

None of this requires a new competitor to bite. But India already has two, and both are growing far faster than the industry SBI Funds Management leads. Zerodha Fund House's AUM rose 2.6 times, to ₹13,133 crore, and Groww AMC's AUM nearly tripled, to ₹4,730 crore, in the year to April 2026. Even added together, Zerodha and Groww's fund arms are worth roughly 1.4 percent of SBI Funds Management's ₹12,487.9 billion book, our calculation from those two figures. They are not a threat to SBI's scale today. They are a threat to the assumption that a bank-branch distribution edge is the only route to India's fund-buying public, at a moment when both firms already distribute investment products through the discount-broking apps millions of Indians use to invest directly.

SBI's own revealed preference

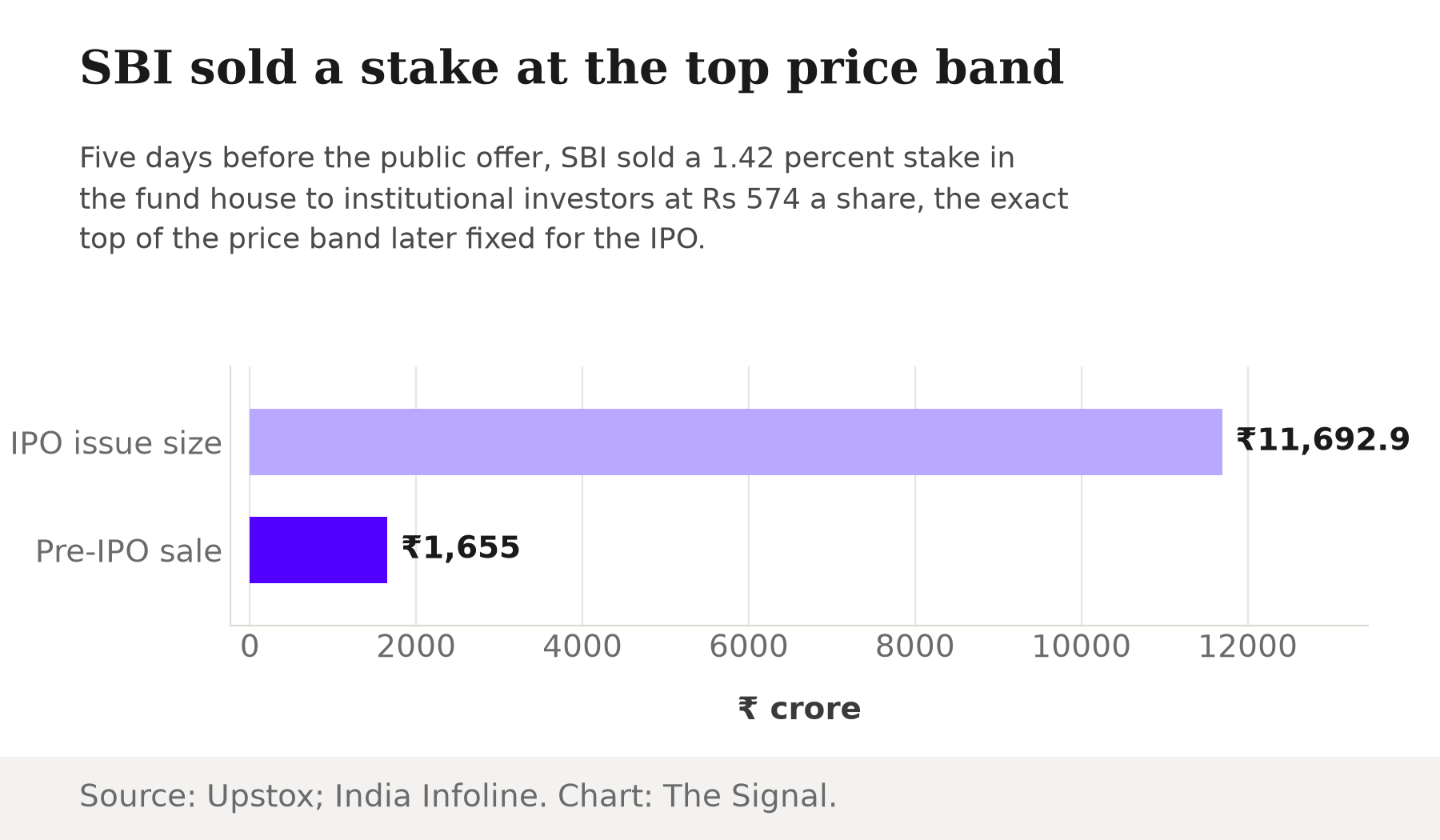

The clearest signal of what SBI itself thinks this business is worth arrived before the public even got a chance to bid. Five days before the IPO opens, SBI sold a 1.4156 percent stake in the fund house, 2.88 crore shares, to 30 institutional investors for about ₹1,655 crore, at ₹574 a share. That price is not a discount. It is the exact top of the ₹545 to ₹574 band later fixed for the public offer. A seller who controls the timing and the counterparty list, and who chooses to lock in the ceiling price with institutions rather than wait to see what the open market bids, is telling you something about where it thinks the risk in that price sits.

The honest objection

The strongest case for the moat is that SBI Funds Management does not need to win every rupee to keep winning. Its 15.4 percent share is still growing at 12.1 percent a year, and the pool it draws from is expanding too: India's mutual fund industry held ₹81,58,342 crore in assets as of May 2026, roughly six times its size a decade earlier. A shrinking share of a fast-growing pie can still mean a growing business, and SBI's branch network, built over more than two centuries, remains a distribution asset no direct-only platform can replicate for the millions of Indians who still prefer walking into a branch. On this reading, the pre-IPO placement at the top of the band is not a warning, it is confirmation: 30 sophisticated institutional buyers looked at the same numbers and paid the ceiling price anyway.

SBI Funds Management's own book adds a real complication to the bear case. 57.68 percent of its assets already sit in its Direct channel, investors holding direct plans, against 42.32 percent in regular plans sold through third-party distributors including SBI's own branches, and that mix has barely moved in three years, from a near-identical 57.67-42.33 split in March 2024. Most of that direct share is institutional money that never needed a distributor to begin with, so it is not proof the branch channel is safe for retail investors specifically. But it does mean the company's own book, unlike the individual-investor numbers above, has not visibly eroded.

That case holds for SBI Funds Management's absolute size. It does not hold for the specific thing this IPO prices, which is the value of the bank-branch channel itself as a growth engine. The pace of the direct-plan migration keeps rising, not falling: individual investors' direct-plan AUM grew 43.5 percent in 2025 against 11 percent for regular plans, the same gap the moat has to overcome, not close. Nor is the market pricing in a rich premium for that bet: SBI Funds Management's listed peers trade at FY2026 price-to-earnings ratios from 31.57 times for UTI AMC to 51.10 times for Nippon Life India AMC. On its own FY2026 diluted EPS of ₹15.04, SBI Funds Management's ₹545-574 price band works out to roughly 36 to 38 times earnings, our calculation from those two figures. That sits below HDFC AMC's 41.71 times, Nippon's 51.10 times and ICICI Prudential AMC's 49.38 times, though above Aditya Birla Sun Life AMC's 34.46 times and UTI's own 31.57 times. A buyer of this IPO is betting on something narrower than India's mutual fund industry's growth, which already looks safe, and the price band is not obviously stretched next to listed peers either. The real bet is that a distribution channel losing share every year AMFI measures it can still command a mid-pack multiple for that specific advantage, in a market where the seller itself chose to cash out a slice at the top of the range five days before opening the doors to everyone else.

The Signal

This IPO is a test of two different bets wearing the same ticker. One is that India's mutual fund pool keeps growing, which the AMFI numbers support without much argument. The other is that a bank-branch distribution network is worth a rich premium even as the reason to use one, avoiding the hassle of a direct account, keeps disappearing into an app. Watch AMFI's next monthly release: if direct plans' share of individual AUM keeps climbing at anything like last year's pace, the second bet gets harder to defend with each update. SBI, the party that knows its own franchise best, has already placed its bet. It sold at the top of the band five days early rather than wait to see what the rest of the market would pay.

Reporting basis: the IPO's offer-for-sale structure, SBI Funds Management's market share and AUM, and SBI's distribution network figures are per SBI Funds Management's draft red herring prospectus filed with SEBI, which in turn cites CRISIL Intelligence. The IPO's dates, price band and issue size are per India Infoline. The pre-IPO placement terms are per Upstox's reporting of the placement agreements. The industry-wide direct-plan share of AUM is from the AMFI-CRISIL Factbook 2024. Individual investors' direct-plan AUM growth is per Business Standard, citing AMFI data. Zerodha Fund House and Groww AMC's AUM figures are per Outlook Business. The Indian mutual fund industry's total AUM and its decade-long growth are per AMFI. The combined scale of Zerodha and Groww's fund arms relative to SBI Funds Management's AUM is The Signal's calculation from those figures. SBI Funds Management's own direct-versus-third-party distribution mix and its listed peers' price-to-earnings ratios are per SBI Funds Management's red herring prospectus filed with SEBI; the implied P/E of its own IPO price band is The Signal's calculation from that prospectus's disclosed earnings-per-share figure and the price band reported by India Infoline.