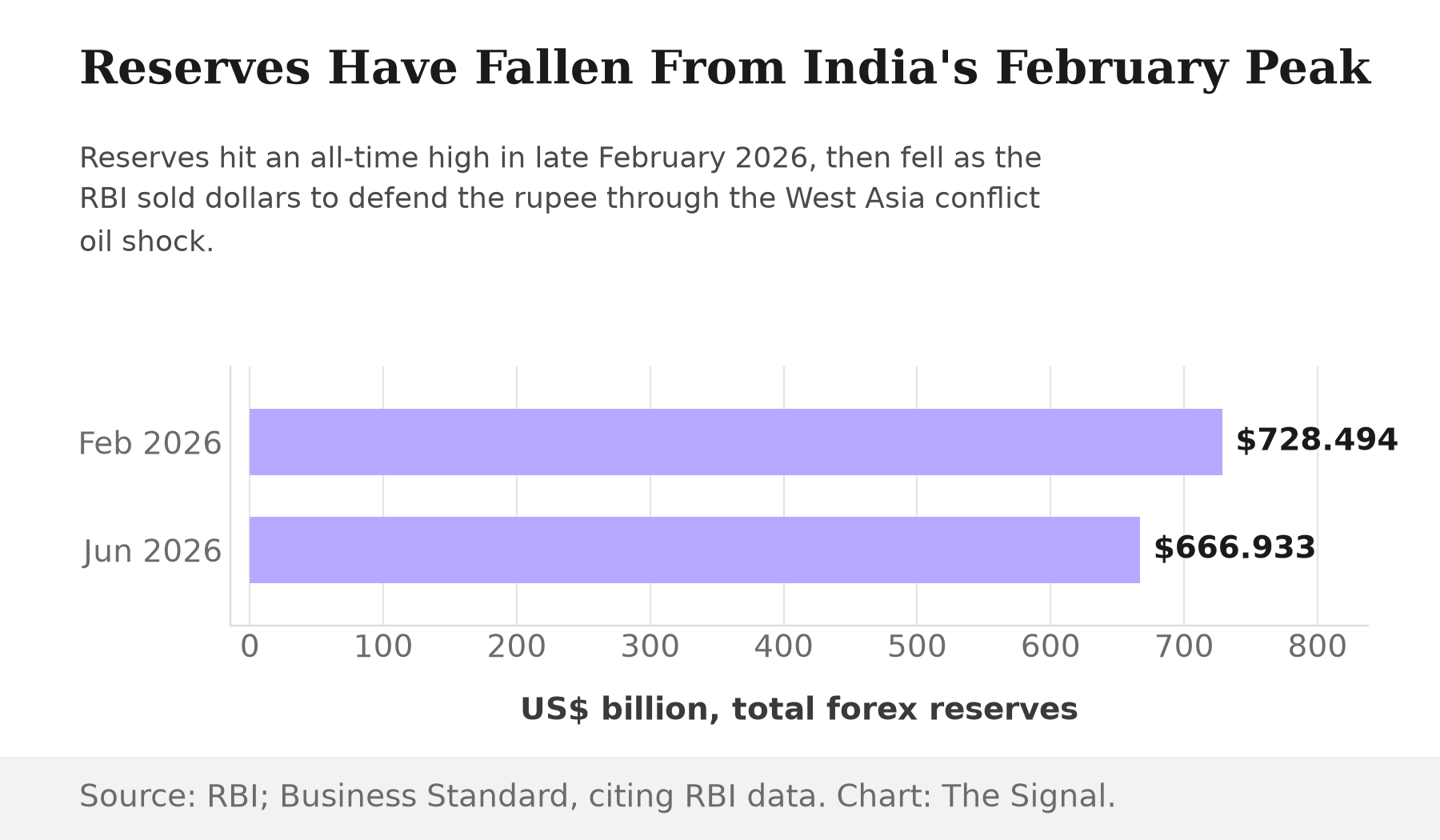

India's forex reserves hit an all-time high of $728.494 billion in the week ended February 27, 2026, Business Standard reported, citing RBI data. Weeks later, crude prices went from a regional wobble to a full-blown shock: international crude surged from about $70 a barrel to around $122 a barrel in under four weeks, a jump of nearly 75 percent. That forced India to cut fuel excise duty by ₹10 a litre on both petrol and diesel on March 27, 2026, according to a Press Information Bureau release from the Ministry of Petroleum and Natural Gas. The rupee came under sustained pressure, and the RBI did what central banks do: it sold dollars to slow the slide. By June 26, 2026, reserves stood at $666.933 billion, the RBI's own Weekly Statistical Supplement shows. The reserves cushion has fallen $61.6 billion from its February peak, and the headline story is straightforward: the RBI spent down its war chest to hold the line.

RBI's reserves cushion has fallen $61.6 billion, from a $728.494 billion February peak to $666.933 billion in June.

That is the visible defense. It is not the whole defense.

The bill that has not come due

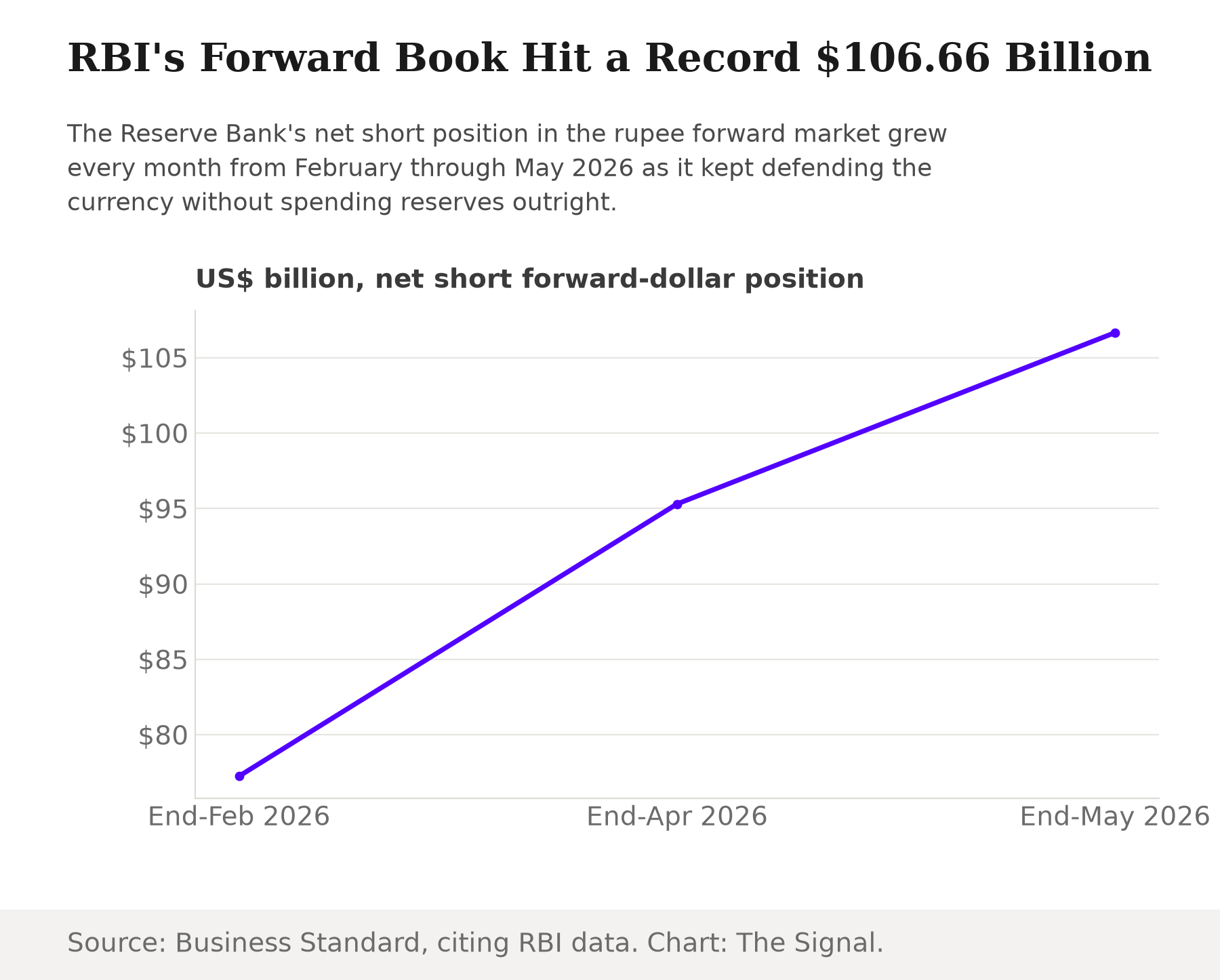

Alongside spot sales, the RBI has been selling dollars forward, agreeing today to deliver dollars at a future date rather than handing them over now. That book has grown fast. The RBI's net short forward dollar position had already reached $77.25 billion by end-February 2026, the highest since March 2025, Business Standard reported, citing RBI data. It rose to $95.30 billion by end-April and then to a record $106.66 billion by end-May 2026, with $56.07 billion of that maturing beyond one year, Business Standard reported.

A net short forward position is a commitment, not a completed sale. The RBI has agreed to deliver dollars it does not currently hold in reserves; it must source them later, either from fresh spot purchases, from reserves at maturity, or by rolling the contracts forward again. The $106.66 billion outstanding at end-May is larger than the entire $61.6 billion drawdown in headline reserves since February. The forward book, in other words, is now a bigger number than the visible cost of the defense it was built to support.

RBI's record forward book is larger than the entire reserves drawdown since February.

Of the $106.66 billion total, $56.07 billion matures beyond a year; the rest, about $50.6 billion, comes due within twelve months of end-May 2026. That is dollars the RBI has committed to deliver by roughly May 2027, on top of whatever fresh pressure the rupee faces between now and then. And not every rupee of the $666.933 billion headline reserve figure is available to meet that bill: $541.067 billion is foreign currency assets, the hard-currency holdings the RBI can actually deploy, while $102.536 billion sits in gold, per the same Weekly Statistical Supplement. Gold backs the balance sheet; it does not settle a forward dollar contract without first being converted. The dollar-liquid cushion behind the forward book is smaller than the headline number suggests.

The rupee did not wait for the unwind

The risk is not abstract. The rupee weakened to a record closing low of 95.71 per dollar on May 13, 2026, extending its 2026 slide, Business Standard reported, and that record low landed in the same window the forward book was climbing from $77.25 billion to $106.66 billion. A weaker rupee makes every dollar the RBI still owes more expensive to source in rupee terms. The forward book was built to buy time and calm the spot market without an immediate reserves hit. It does not remove the currency risk, it defers it, and it defers it into a market that spent the same three months getting worse, not better.

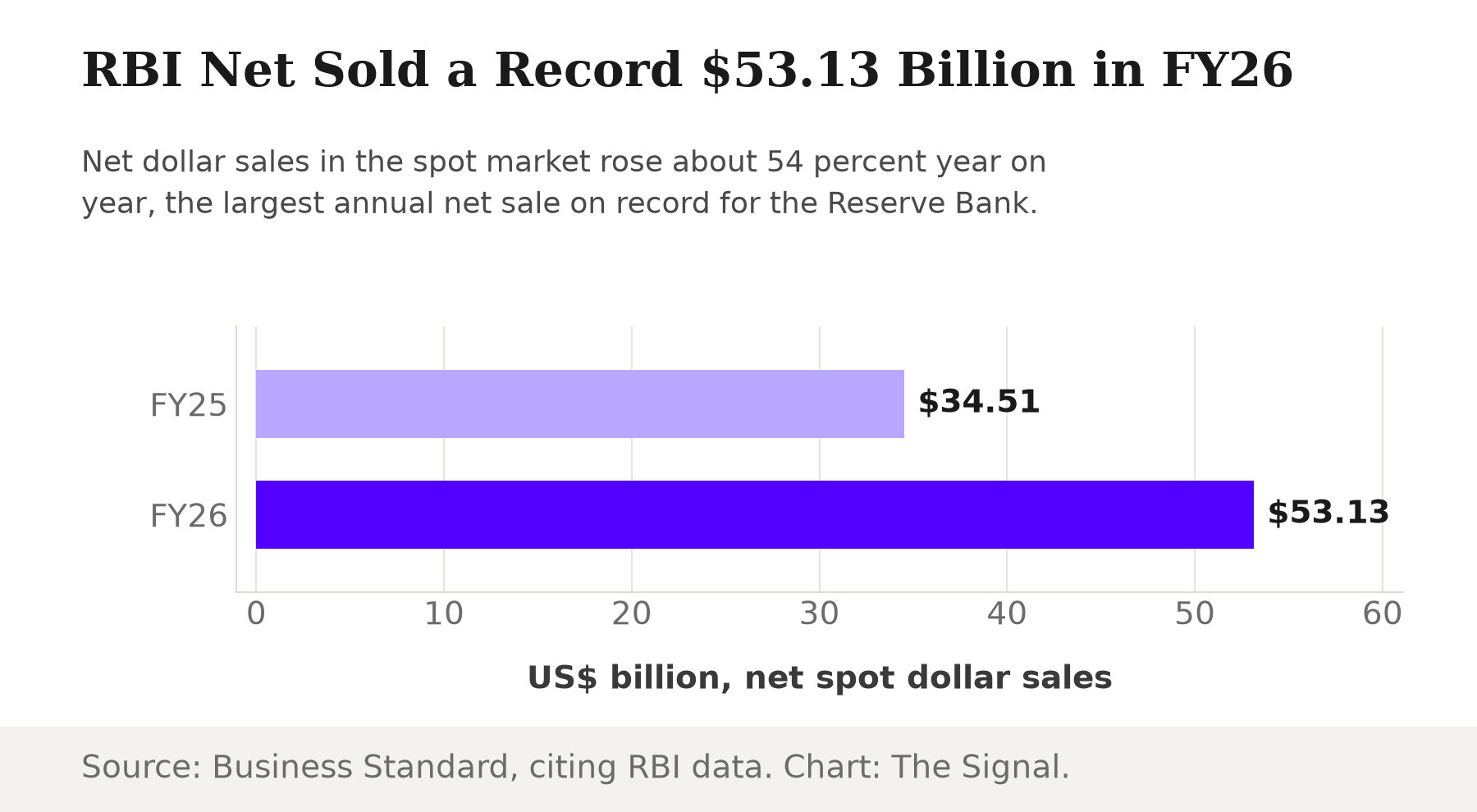

Over the same fiscal year, the pattern shows up in the spot data too. The RBI net-sold a record $53.13 billion in the spot foreign exchange market in FY26 (April 2025 to March 2026), up from $34.51 billion in FY25, a jump of about 54 percent, Business Standard reported, citing RBI data. Spot sales and the forward book are not the same instrument, but they point the same direction: a central bank leaning harder on every tool it has to hold the rupee's line.

One adjustment did happen fast

Not every part of India's energy exposure moved slowly. India's crude oil imports from OPEC nations fell to 44.2 percent of the total in April 2026, down from 48.7 percent a year earlier, a drop of 4.5 percentage points, as refiners diversified toward non-OPEC supply, according to the Petroleum Planning and Analysis Cell's monthly report. Refiners could reroute purchases within a single reporting month. The RBI cannot reroute a forward contract; it can only wait for it to mature, roll it, or pay it.

The shock has not finished landing

The forward book was built to buy time for one oil shock, the one that began in February, to fade before the bill comes due. It has not gotten that time. Iran's Islamic Revolutionary Guard Corps fired missiles that struck three commercial ships in or near the Strait of Hormuz within 24 hours on July 6-7, 2026, including the Qatari LNG tanker Al Rekayyat and a Saudi-flagged crude carrier, Al Jazeera reported. The attacks broke a June 14, 2026 truce that had guaranteed safe shipping passage through the strait for at least 60 days. Brent crude rose to $76.48 a barrel, its highest level since June 23, 2026, after the US launched fresh strikes on Iran on July 8 in response, Al Jazeera reported. The forward book's bet was that the rupee would recover before the contracts matured. That bet now has to survive a second oil shock arriving before the first one has even been paid for.

The honest objection

The strongest case for the RBI's approach is that forwards are a standard, deliberate smoothing tool, not a sign of losing control. Selling dollars forward instead of dumping them in the spot market avoids an immediate, visible reserves hit that could itself spook the market, and it buys time for the shock, an oil-driven currency shock tied to the West Asia conflict, to fade before the bill comes due. Other emerging-market central banks manage currency pressure with forward books for exactly this reason, and $56.07 billion of the current book is not due for more than a year, which gives the rupee room to recover before those contracts must be settled.

That case is real, and it is also the reason the timing matters. The objection assumes the pressure fades before the contracts mature. Nothing in the data confirms that yet: the rupee's record closing low came on May 13, 2026, the same month the forward book hit its record $106.66 billion, reserves kept falling into June, and fresh Hormuz attacks in July show the underlying shock reasserting itself rather than fading. A smoothing tool that is still growing every month it has existed is not yet evidence of smoothing. It is evidence of a bet still being placed.

The Signal

The headline number in every reserves story is the one the RBI publishes weekly: $666.933 billion, down $61.6 billion from February. That number is real, but it is not the size of the defense. The $106.66 billion forward book is larger, growing faster, and due on a clock the RBI does not fully control. Roughly $50.6 billion of it matures within a year, against a rupee that has not stopped weakening, and the shock behind it is still active, not fading. If the currency stabilizes before those contracts come due, the forward book unwinds quietly and the whole episode reads as prudent management. If it does not, the RBI will be buying dollars to fulfill contracts written when the rupee was stronger than it is now, and the reserves drawdown investors have been watching will turn out to have been the smaller of the two bills. Watch the forward book, not just the weekly reserves print.

Reporting basis: the fuel excise duty cut and the crude price surge are from a Press Information Bureau release by India's Ministry of Petroleum and Natural Gas. The OPEC import share is from the Petroleum Planning and Analysis Cell's monthly report. India's total foreign exchange reserves, and their split between foreign currency assets and gold, are from the RBI's own Weekly Statistical Supplement. The February 2026 reserves peak is as reported by Business Standard, citing RBI data. The forward-dollar position at end-February is as reported by Business Standard, and at end-April and end-May is as reported by Business Standard, both citing RBI data. The FY26 and FY25 spot dollar sales are as reported by Business Standard, citing RBI data, and the rupee's record closing low is as reported by Business Standard. Business Standard is the sole source for each of those figures. The July 6-7, 2026 Strait of Hormuz ship attacks and the June 14, 2026 truce they broke are as reported by Al Jazeera, and the July 8 oil-price move is as reported by Al Jazeera. The $61.6 billion reserves drawdown, the comparison between the forward book and that drawdown, the roughly $50.6 billion of the forward book maturing within a year, the foreign-currency-asset share of reserves, and the percentage changes cited are The Signal's calculations from those figures.