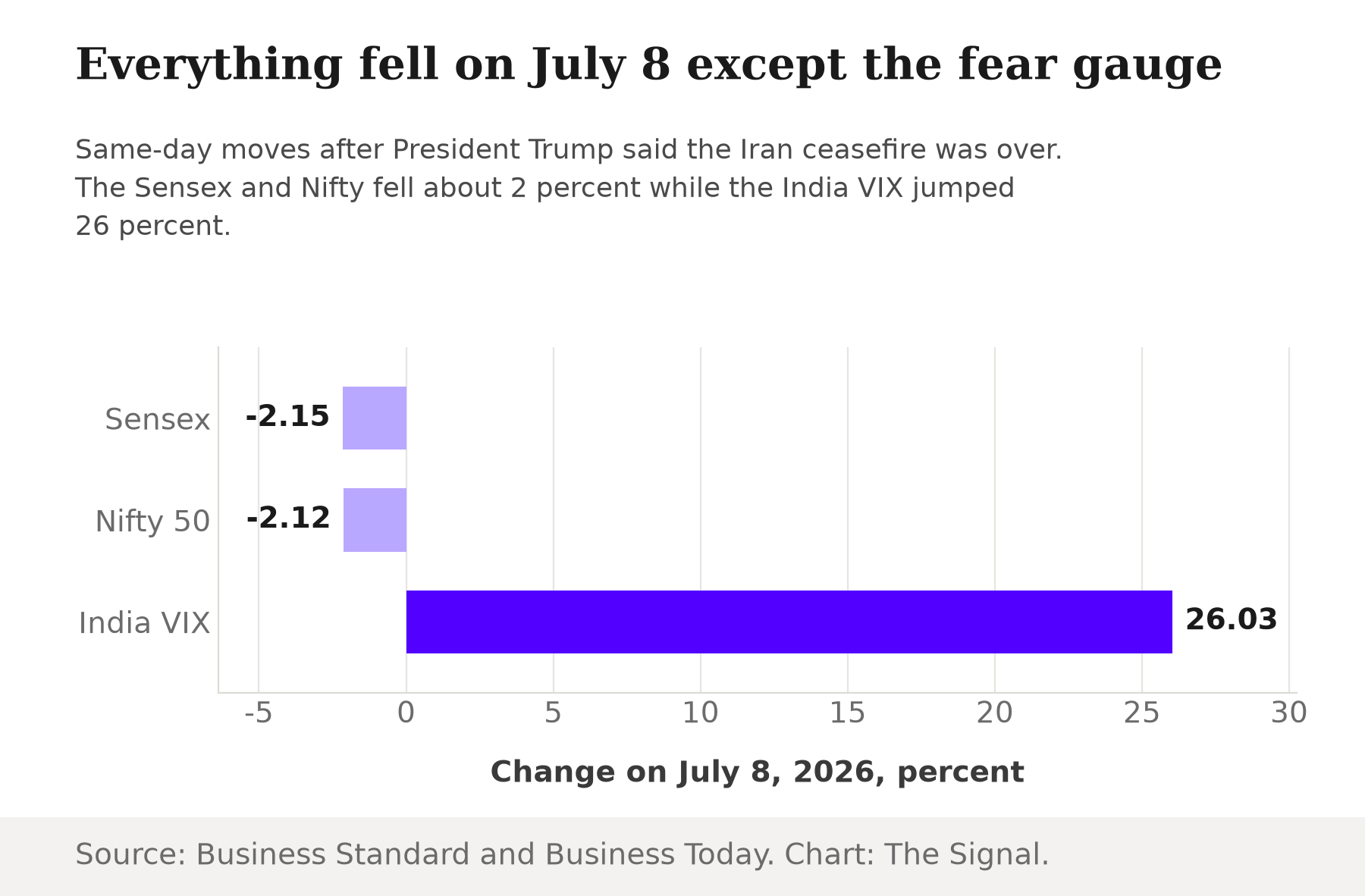

On July 8, 2026, India's markets had their worst day in months. The BSE Sensex closed 1,677.12 points, or 2.15 percent, lower at 76,503.60, and the Nifty 50 closed 516.65 points, or 2.12 percent, lower at 23,882.05, after President Trump said the interim ceasefire understanding with Iran was over. India VIX, the market's fear gauge, climbed 26.03 percent to close at 14.68, and Brent crude jumped 5.85 percent to $78.50 a barrel the same day, after attacks on commercial vessels transiting the Strait of Hormuz. Read that way, the story is simple: a geopolitical shock out of the Middle East hit a market that had nothing to do with it.

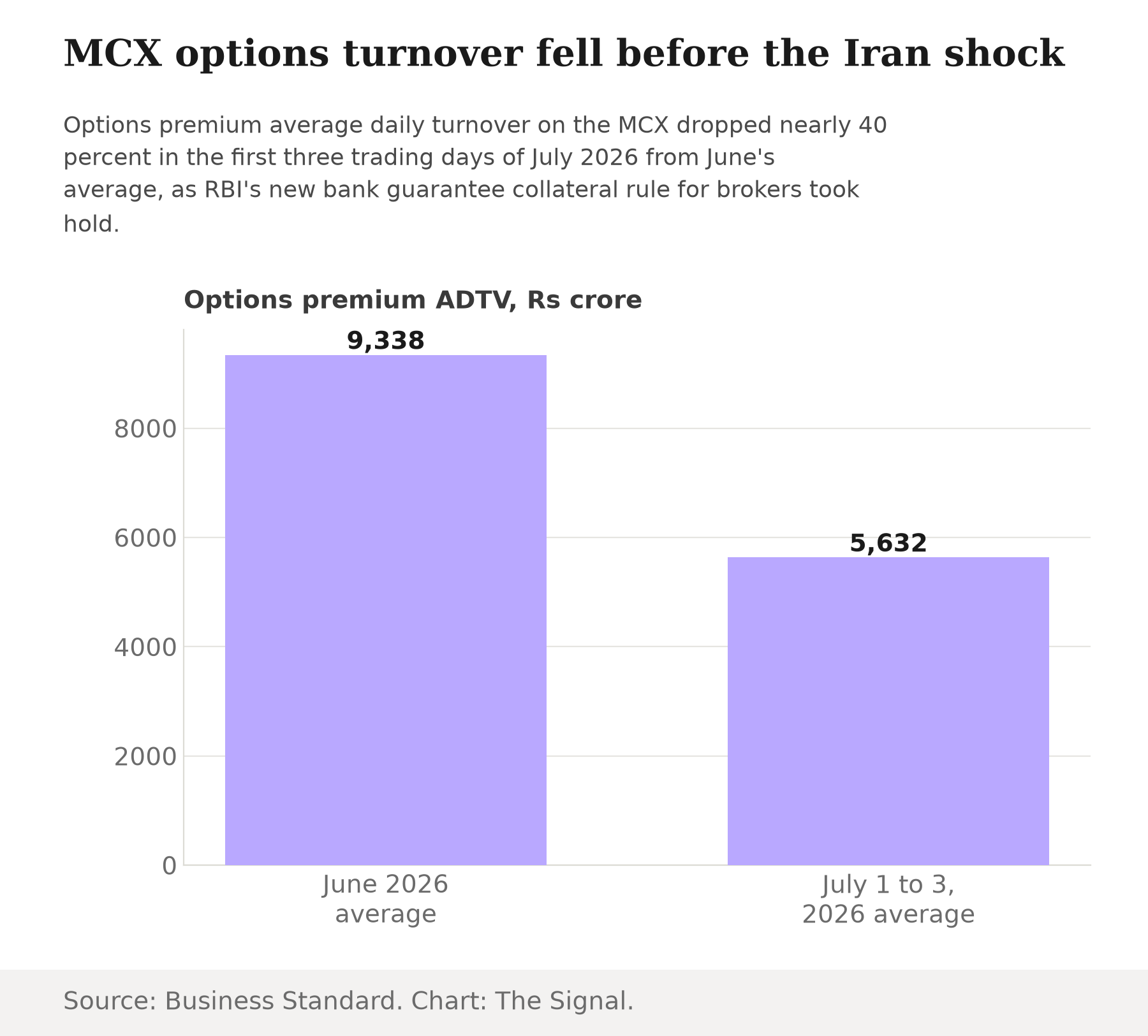

It is worth slowing down on that. In the same week, for a reason that has nothing to do with Tehran, India's own derivatives market had already gone quiet. MCX's options notional average daily turnover was down 71 percent month on month by July 7, and options premium turnover on the exchange had fallen nearly 40 percent, to Rs 5,632 crore in the first three trading days of July from Rs 9,338 crore in June. The cause sat in Mumbai, not the Gulf: a new Reserve Bank of India rule on how banks can finance brokers' proprietary trading.

The rule that emptied the order book

The RBI's press release requires that bank financing to capital market intermediaries for proprietary trading be backed by 100 percent collateral in cash or cash equivalents, a requirement that took effect July 1, 2026 after being deferred from an original April 1 start date. A separate RBI notification, RBI/2025-26/211, requires that bank guarantees issued to brokers for proprietary trading be secured by a minimum of 50 percent collateral, of which at least 25 percent must be cash.

What RBI's new collateral rule requires of brokers

| Facility to broker | Minimum collateral | Cash share |

|---|---|---|

| Bank financing for proprietary trading | 100% | 100%, cash or cash equivalents |

| Bank guarantees for proprietary trading | 50% | At least 25%, in cash |

Source: RBI press release; RBI notification RBI/2025-26/211.

Before July 1, a broker could carry a proprietary book against a bank guarantee or a financing line with a much thinner cash cushion than the new 100 percent and 50 percent collateral floors now require. For a business that runs on turnover, a rule that locks up capital rather than deploying it is a rule that shrinks the book, and the options-premium data above shows it happening inside the rule's first three trading days.

The bill comes due, same week

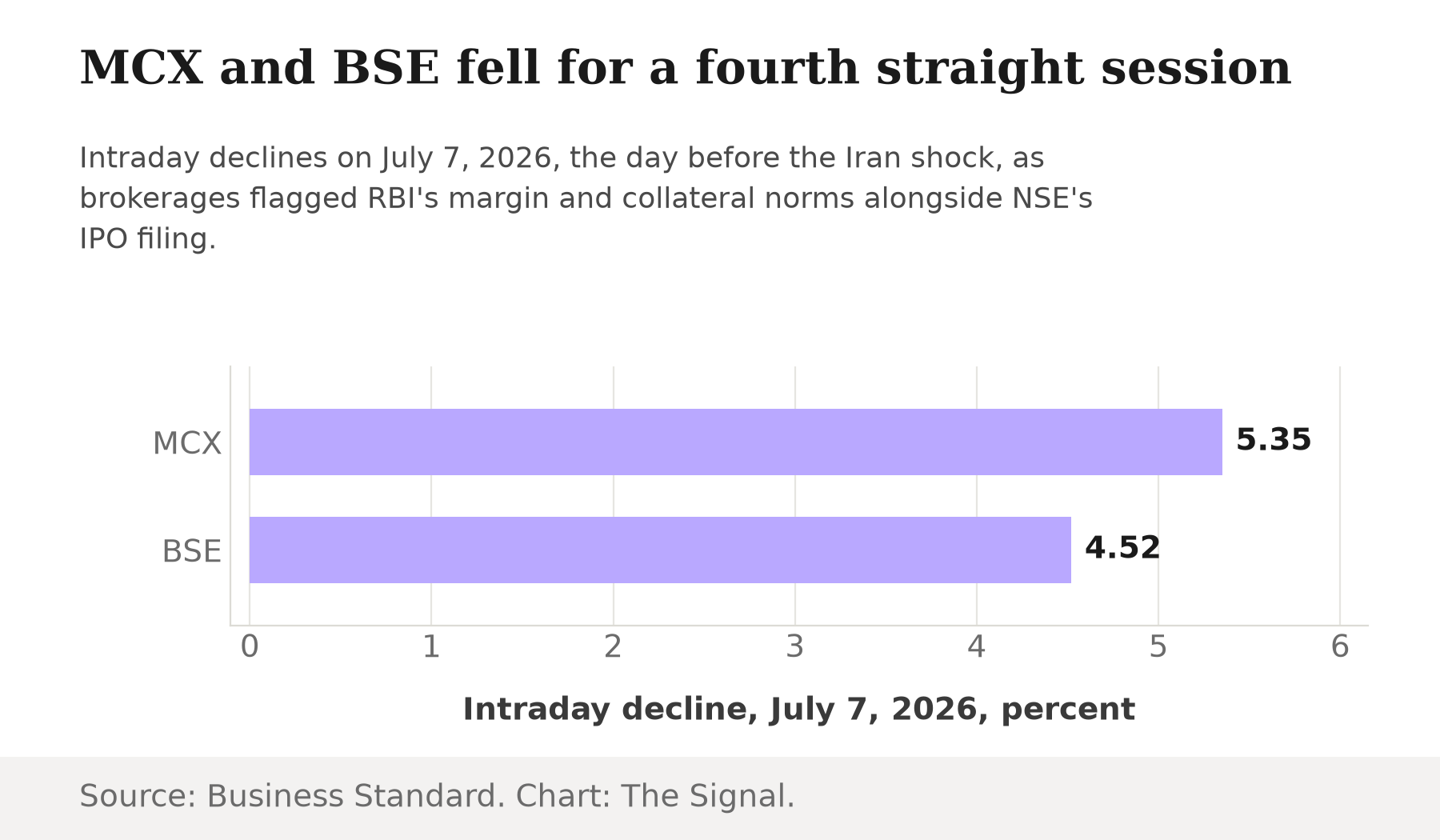

MCX and BSE shares fell for a fourth straight session on July 7, 2026, with MCX down as much as 5.35 percent intraday and BSE down 4.52 percent, and brokerages pointed directly at the new rules: SBI Securities analyst Sunny Agrawal said options notional average daily turnover had declined 71 percent month on month while options premium turnover was down 40 percent.

A second, unrelated pressure landed the same day. NSE filed draft papers with SEBI for a Rs 30,000 crore IPO, and a Jefferies note on NSE's profitability released around the same time added to the selling, with MCX and BSE shares separately reported down 5.38 percent and 4.53 percent that day. Two outlets, two slightly different cuts of the same afternoon's trading, but the direction is not in question: India's exchange stocks and its derivatives turnover were both under pressure a full day before anyone in Mumbai was pricing in the Strait of Hormuz.

Then Iran happened

Less than 24 hours later, Trump's remark gave the market an actual geopolitical shock to price. The Sensex and Nifty each fell about 2 percent and Brent crude jumped over 5 percent, but the sharpest single move belonged to volatility itself: India VIX rose 26.03 percent in a single session. A market that had spent the prior week trading less, on a thinner cushion of broker capital, absorbed a real shock the next day.

The honest objection

The strongest case against linking these two stories is that they measure different things. RBI's rule targets bank financing and guarantees for brokers' proprietary trading books, a narrow corner of market plumbing on a commodity exchange. India VIX is computed from Nifty options prices and reflects how expensively the whole equity market is pricing near-term uncertainty, not how much cash a handful of brokers have tied up in collateral at MCX. A thinner options book on one exchange does not mechanically transmit into a higher volatility reading on an entirely different market. On this view, the coincidence of dates is just a coincidence: a prudential rule doing its intended job of derisking broker balance sheets happened to land in the same week an unrelated oil shock arrived.

That case holds for causation, but not for timing. Whatever the mechanism connecting them, or not, India's own derivatives market was carrying sharply less turnover and less broker capital in the exact week a real shock arrived to test it. The rule may be sound risk management on its own terms. It does not change the fact that the market had the least room to spare exactly when it needed the most.

The Signal

None of this makes RBI's collateral rule wrong. Requiring cash-backed collateral for proprietary trading is the kind of tightening regulators are supposed to do between crises, not during one, and India would rather have this fight in a calm week than a chaotic one. But the sequence itself is worth remembering regardless of causation: the country tightened the plumbing of its derivatives market in the same week a geopolitical shock arrived to test how that market absorbs stress. Watch what happens to MCX and BSE turnover over the next month. Recovering volumes, as brokers adjust their capital structures to the new rule, would mark this down as a one-time transition cost. If turnover stays this thin every time a shock like Iran's lands, India will have learned that a safer rule and a deeper market do not automatically arrive together, and on July 1 it chose the rule.

Reporting basis: RBI's collateral requirements for bank financing and bank guarantees to brokers are per the Reserve Bank of India's own press release and its notification RBI/2025-26/211. The MCX turnover declines are as covered by Business Standard, citing market analysts' data and quoting SBI Securities analyst Sunny Agrawal; the NSE IPO filing and Jefferies note angle is per Business Today's separate account of the same day's trading, an independent origin from Business Standard's. The Sensex and Nifty closing levels are per Business Standard; the India VIX figure is per Business Today; the Brent crude figure is per CNBC.