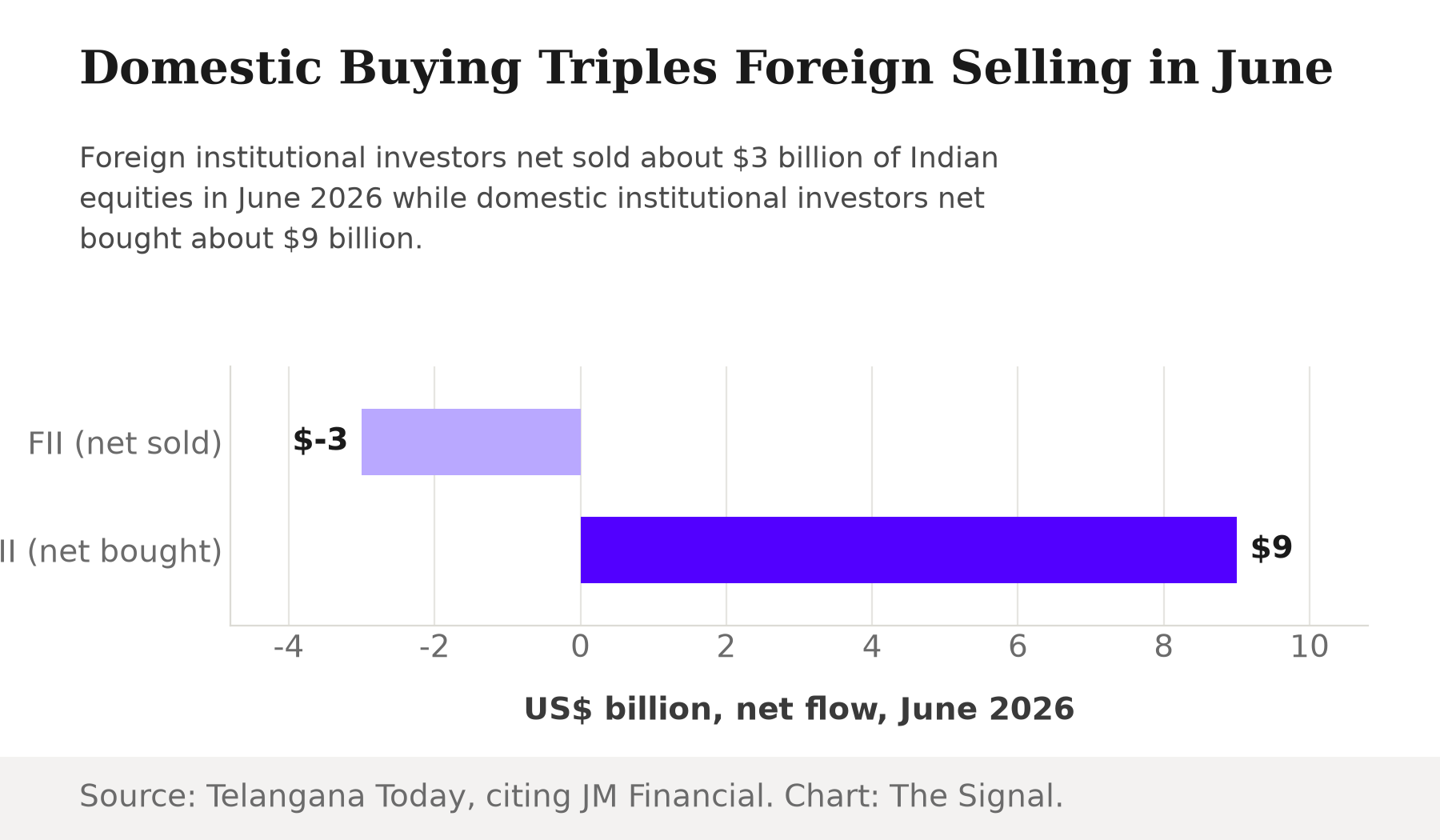

Every month now brings the same reassurance about Indian equities: foreign investors are selling, but domestic buyers are more than covering it. In June 2026, foreign institutional investors (FIIs) were net sellers of about $3 billion of Indian equities while domestic institutional investors (DIIs) were net buyers of about $9 billion, roughly three times as much, according to a JM Financial Institutional flows report cited by Telangana Today. Read only that one month and the story is a clean handoff: foreign money heads for the door, domestic money fills the room, and the index does not notice the difference.

It is worth slowing down on that framing. June was not a single strong month papering over an otherwise stable foreign base. It is the latest data point in a structural retreat that reaches back years and shows up across several different measures of Indian stock ownership.

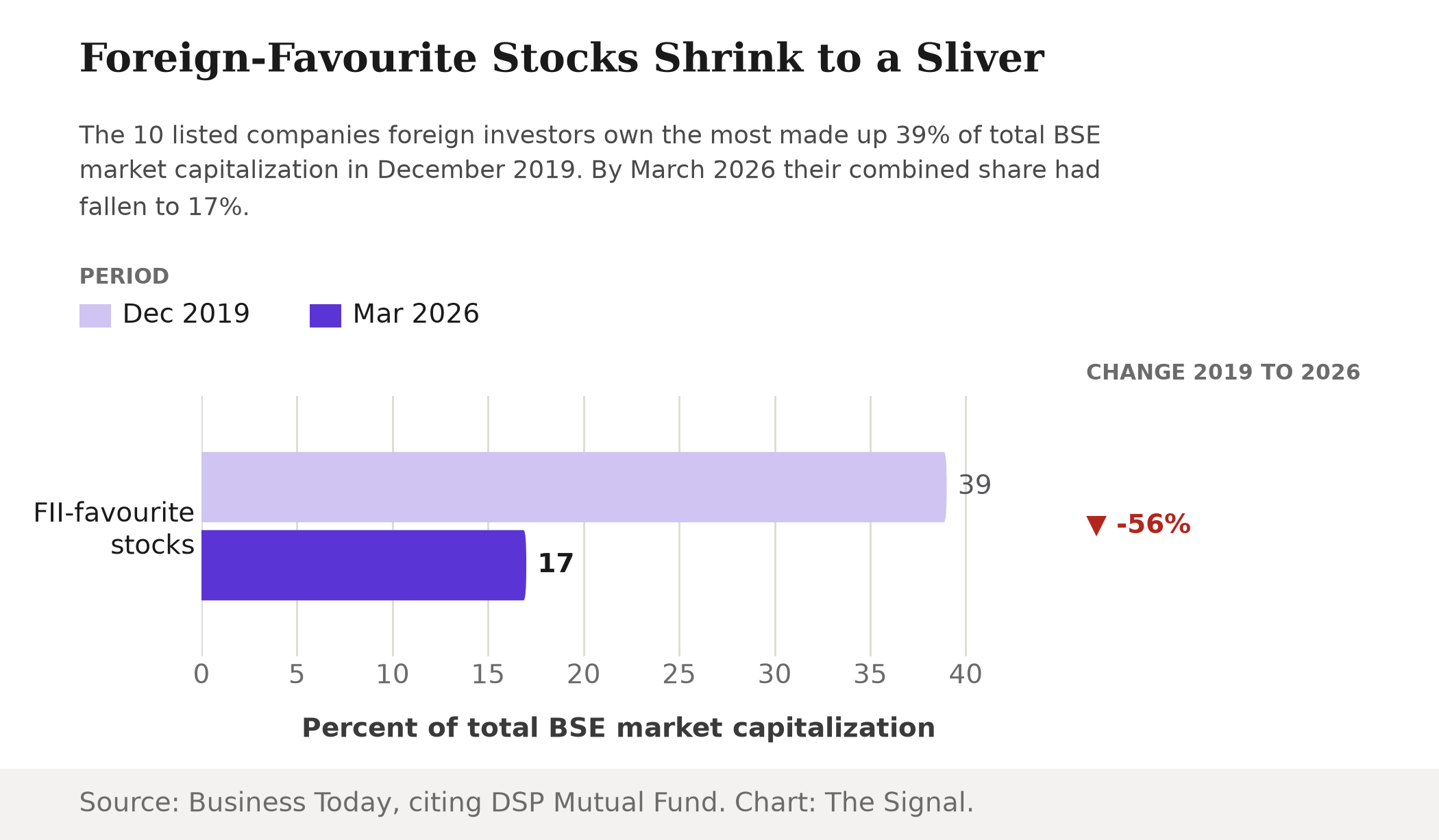

Average FII ownership across India's 10 largest listed companies has fallen to just 34% of free-float market capitalization, the lowest level in two decades, below even the 37% trough hit during the 2008 Global Financial Crisis, according to Business Today's reporting on DSP Mutual Fund's monthly Netra report, as of the quarter ended March 2026 (Business Today).

A two-decade low, confirmed a second way

The same DSP Netra analysis put a second number on the same trend. The combined market capitalization of those ten companies, the stocks foreign investors have historically owned the most, has slipped to just 17% of total BSE market capitalization, down from a 39% peak in December 2019, as of the quarter ended March 2026 (Business Today). Less than half of the December 2019 share now remains.

The pattern repeats market-wide, and crosses over

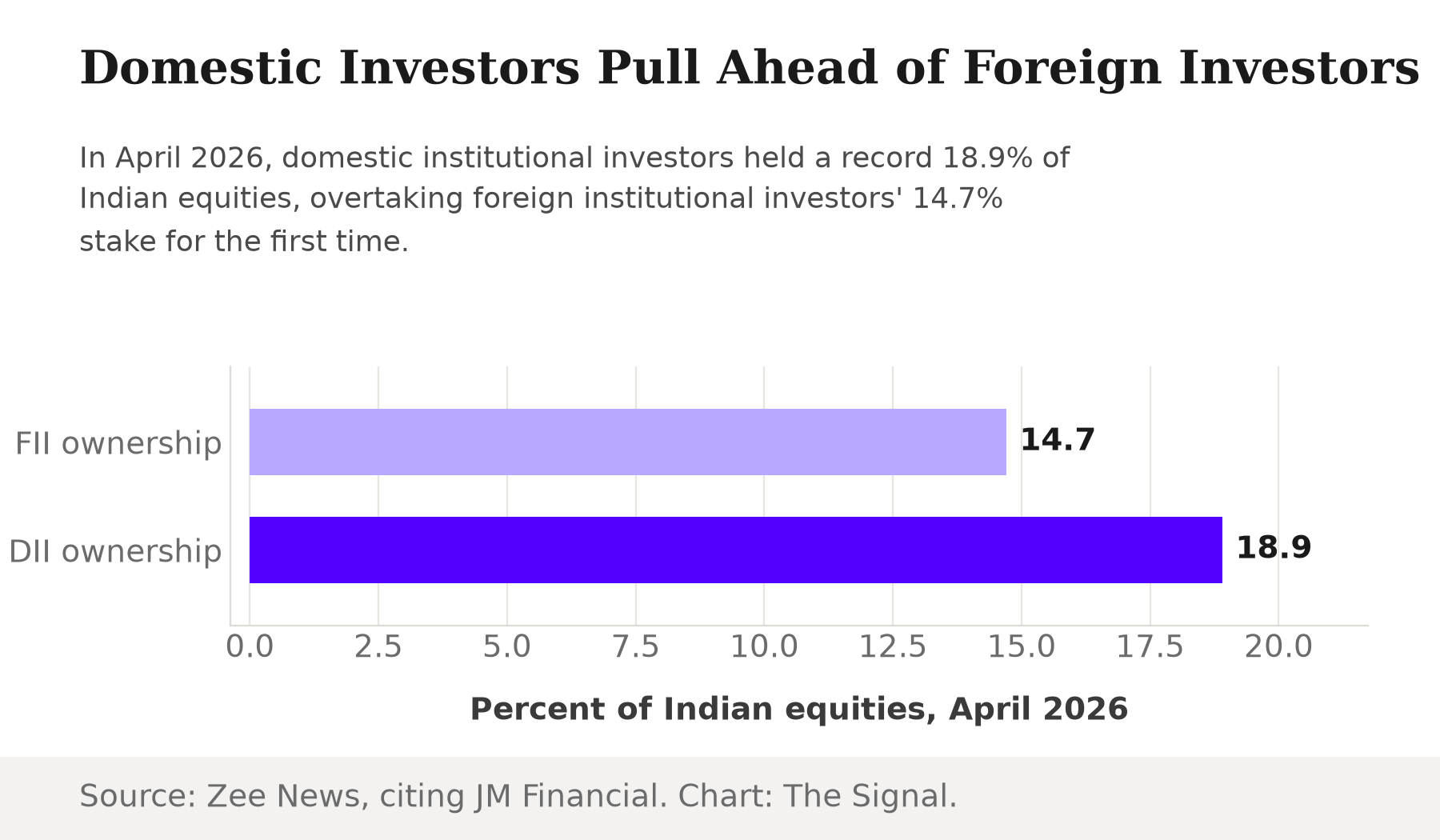

Zoom out from the ten largest names to the whole market and the same direction shows up, with an added twist. FII ownership of Indian equities fell to 14.7% in April 2026, its lowest level since June 2012, down from 19.9% in April 2016, more than five percentage points lower in a decade, according to JM Financial's Fundamental Research report, cited by Zee News. In the same month, DII ownership climbed to a record 18.9%, the first time domestic institutions have owned more of India's listed companies than foreign investors (Zee News).

That crossover is the detail that separates a rotation from a regime change. A single month of DII buying outrunning FII selling is a flow story: it can reverse the moment sentiment turns. Domestic institutions now owning more of the market than foreign institutions, for the first time on record (Zee News), describes who actually holds the shares, not who traded them last month. That kind of position does not unwind in a single quarter of contrary flows.

The flow data keep agreeing with the ownership data

Three separate readings of 2026, two different data sources, point the same way.

| Period | Net FPI equity flow | Source |

|---|---|---|

| April 1 to June 2, 2026 | -$13.4 billion | The Reserve Bank of India's Governor's Statement |

| January to June 2026 (H1) | -$29.28 billion (Rs 2.74 lakh crore) | NSDL depository data, via Business Today |

Source: the Reserve Bank of India's Governor's Statement; Business Today, citing NSDL depository data. Table: The Signal.

The two figures cover overlapping but distinct windows and come from different compilers, a central bank statement and a depository's own record of settled trades, yet they describe the same direction at a similar scale: tens of billions of dollars of foreign money leaving Indian equities across H1 2026. Ownership figures capture the holders themselves; flow figures capture the money still moving in and out right now. Both point out of the country.

The backdrop the RBI just flagged itself

This retreat is not happening against a backdrop of accelerating growth. If India's economy were speeding up, foreign selling could be read as simple impatience: investors chasing faster returns elsewhere. That backdrop is missing. At its June 2026 policy review, the Reserve Bank of India cut its own FY 2026-27 real GDP growth projection to 6.6%, down from the 6.9% it had projected in April 2026, while holding the repo rate at 5.25% (Reserve Bank of India). A central bank trimming its own growth forecast in the same window that foreign ownership of its market's biggest companies hits a two-decade low is not proof of cause and effect. But it removes the easiest counter-argument: that foreign investors are leaving a strengthening economy for no good reason. The RBI's own numbers say growth is cooling, not accelerating.

The honest objection

The strongest case against reading any of this as alarming is that a rising domestic ownership share is exactly what a maturing market is supposed to produce. Indian mutual funds have spent years building a systematic monthly inflow from retail savers, insurers and pension funds have grown their own domestic equity books, and a market less dependent on footloose foreign capital is, on paper, a more stable one. On this view, FIIs are not fleeing India, they are simply being out-bid by a domestic buyer base that has grown structurally larger and is not going anywhere, and the record 18.9% DII ownership figure (Zee News) is the healthiest number in this entire piece.

That case is real, and the domestic buyer base is genuinely larger and stickier than it was a decade ago. But it does not explain why the retreat shows up on the narrowest slice of the market, the 10 companies foreign investors have historically favoured most (Business Today), at a level below the 2008 financial crisis trough. A structurally larger domestic base can coexist with steady or even rising foreign ownership if foreign capital is also growing; it should not require foreign ownership of the market's biggest, most liquid names to fall further than it did during a global banking collapse. Domestic money filling the gap and foreign money actively retreating from India's safest, largest bets are two different stories, and the evidence here supports both happening together.

The Signal

The headline every month will keep being about whether foreign investors are "returning" or "still selling," because that is the number that moves with the news cycle. What barely moves is the share of India's own companies foreigners actually own, and it now sits lower than it did in the worst month of the 2008 crisis (Business Today), while domestic investors have finally taken the larger seat at the table. Watch that ownership share, not the monthly flow print. If it stabilizes even as flows stay volatile, India's market has genuinely re-based around domestic capital. If it keeps falling, the domestic buying of 2026 is absorbing an exit, not replacing a partner.

Reporting basis: the average FII ownership of India's top 10 listed companies, the combined market cap share of those companies, and the two-decade low reading are all from a single Business Today report of DSP Mutual Fund's monthly Netra report, and rest on that one analysis. Market-wide FII and DII ownership figures, including the April 2026 crossover, are per Zee News, citing a JM Financial Fundamental Research report, and are also a single-source reading. Net FPI equity outflows for April 1 to June 2, 2026 are from the Reserve Bank of India's own Governor's Statement. The six-month 2026 FPI equity outflow figure is NSDL depository data, as reported by Business Today. The June 2026 FII and DII flow split is per Telangana Today (IANS), citing a JM Financial Institutional flows report. The FY 2026-27 GDP growth projection and repo rate are from the Reserve Bank of India's Monetary Policy Committee resolution. The "less than half" comparison of the 2019 and 2026 top-10 ownership shares is The Signal's calculation from those two figures.