National Stock Exchange of India has filed a Draft Red Herring Prospectus with SEBI for what is being called India's biggest stock market debut. NSE first filed for an IPO back in 2016; regulatory hurdles tied to its co-location scandal delayed the listing for years, with SEBI still flagging litigation, governance and technology issues as of March 2025, even after NSE settled a related Rs 643 crore penalty in October 2024. This filing is the payoff of that decade-long clearing process rather than a fresh decision to go public. The offering is estimated at over Rs 30,000 crore, enough to surpass Hyundai Motor India's Rs 27,859 crore October 2024 listing and become the largest IPO in Indian history. State Bank of India is offering up to 24,750,000 equity shares, the single largest allotment among the ten selling shareholders in the filing. Read that far and NSE looks like it is about to raise a record sum to fund its next phase as a public company.

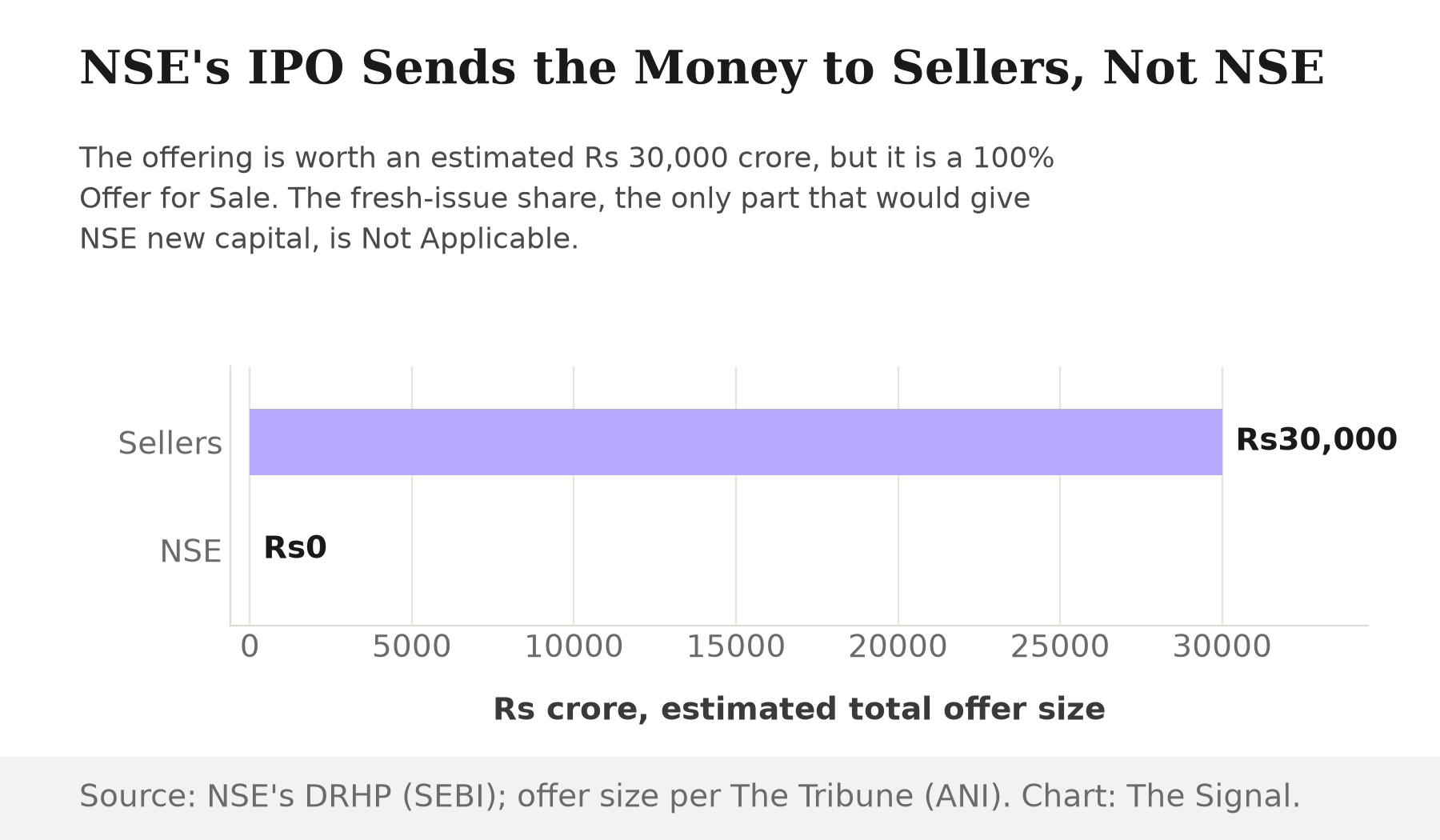

It is worth slowing down on how that number is actually built. The DRHP structures the entire offer as an Offer for Sale of up to 148,905,525 equity shares, about 6.02% of paid-up capital, with the fresh-issue portion marked "Not applicable". An Offer for Sale transfers existing shares from current owners to new buyers; no new shares are created and no proceeds land on the company's own balance sheet. Whatever the final price works out to, NSE itself is not the one raising the Rs 30,000 crore. Its shareholders are.

Source: NSE's Draft Red Herring Prospectus, filed with SEBI. Chart: The Signal.

What the sellers paid, and what buyers now pay

State Bank of India's stake is the clearest illustration of what is changing hands. SBI's weighted-average cost of acquiring its NSE shares works out to Rs 0.80 per share of Rs 1 face value. In the year before the DRHP was filed, NSE shares changed hands between existing holders at prices from Rs 1,350 to Rs 2,260 apiece, with a weighted-average price of Rs 1,909.02. Eighty paise against a weighted average of Rs 1,909.02 is a gap of roughly 2,386 times, our calculation from those two DRHP disclosures.

SBI's cost basis sits nowhere near the price the market paid in the year to the DRHP's June 2026 filing.

| Rs per share | |

|---|---|

| SBI's weighted-average acquisition cost | 0.80 |

| Recent secondary trades, low to high (last year before filing) | 1,350.00 to 2,260.00 |

| Weighted-average price across those trades | 1,909.02 |

Source: NSE's Draft Red Herring Prospectus, filed with SEBI. Multiple is The Signal's calculation.

That gap is not evidence of anything improper; it is simply what decades of holding an equity stake in a business that later becomes scarce and sought-after looks like on paper. But it does mean the drama in an OFS-only listing sits entirely in the price the new buyer pays, not in the capital the company receives.

SBI is not selling alone. Nine other shareholders are offering stock alongside it: MS Strategic (Mauritius) Limited, Canada Pension Plan Investment Board, Aranda Investments (Mauritius), Bank of Baroda, Stock Holding Corporation of India, General Insurance Corporation of India, The New India Assurance Company, National Insurance Company and United India Insurance Company, in allotments ranging from 16 million shares down to 6 million. The sell-down spreads across public-sector banks, state-owned insurers and a foreign pension fund; no single institution is cashing out alone.

The business behind the filing

NSE's public shareholder base is already unusually broad for an unlisted company: 209,376 public shareholders as of the beneficiary position statement of June 15, 2026. The IPO changes liquidity and price discovery on the exchange; the size of that shareholder base stays the same.

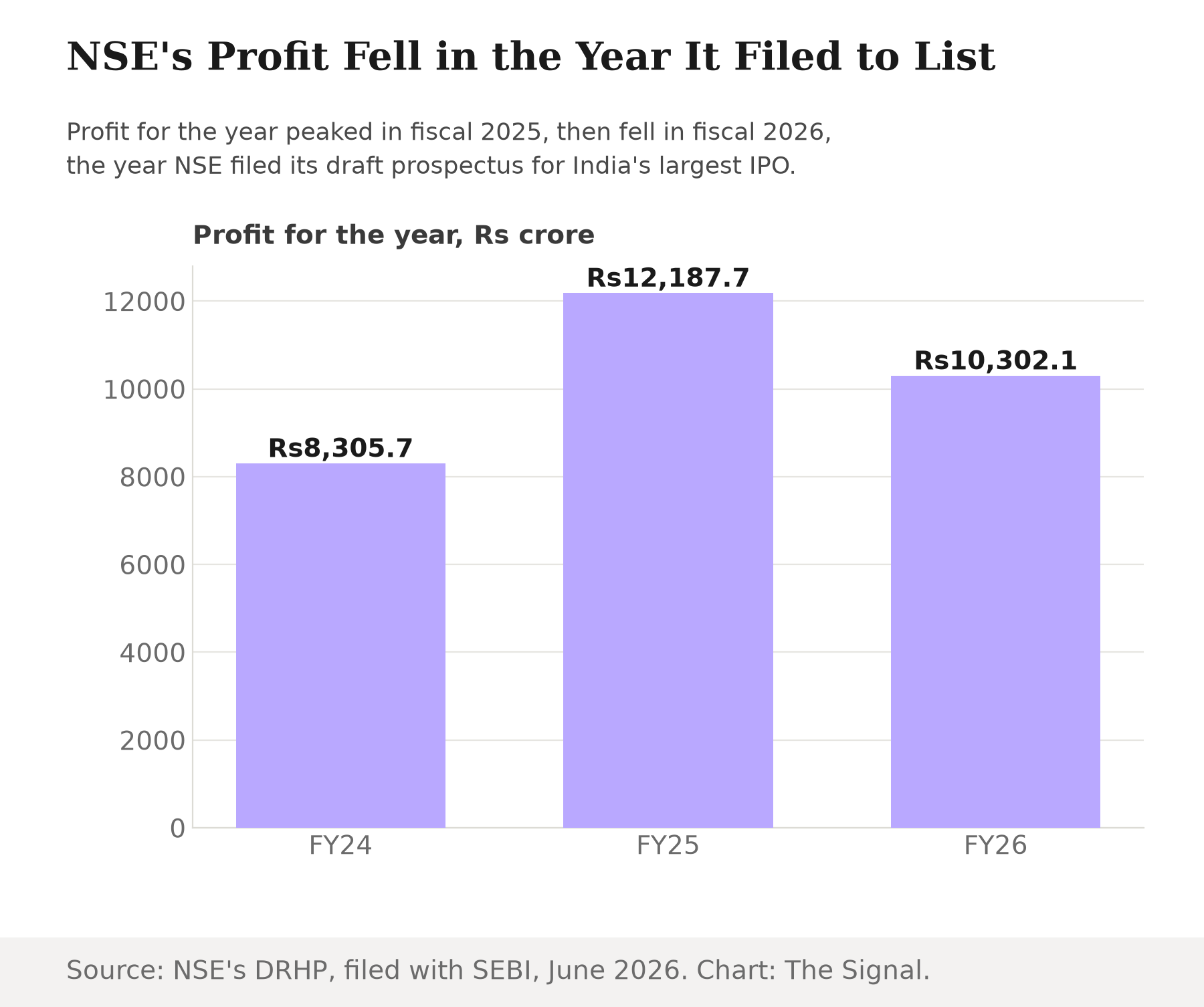

The underlying business the new buyers are pricing is not on an unbroken upward run. NSE's profit for the year was Rs 103,020.61 million, about Rs 10,302 crore, in fiscal 2026, down from Rs 121,876.89 million in fiscal 2025. NSE also derived 78.65% of its fiscal 2026 revenue from transaction charges, largely from its options and futures businesses, down from 79.55% the year before: a business that still leans heavily on trading volumes for its revenue, and where that lean eased only slightly.

Source: NSE's Draft Red Herring Prospectus, filed with SEBI. Chart: The Signal.

There is also an overhang the prospectus discloses on its own terms. As of the DRHP, 18 criminal proceedings, 43 tax proceedings and 6 statutory or regulatory actions are pending against NSE, alongside material civil litigation totalling Rs 26,056.66 million, about Rs 2,606 crore. None of that disqualifies a listing; a buyer is simply pricing it in alongside the brand and the market position.

The one shareholder not selling

LIC is not among the ten shareholders offering stock in this OFS. Instead, LIC used its statutory right under Section 6A of the LIC Act to nominate a director, proposing Shri Dinesh Pant to NSE's governing board in a representation letter dated March 5, 2026. Where SBI is realising a decades-old paper gain, LIC is doing the opposite: deepening its governance role in NSE just as the IPO window opens. One legacy institutional owner is heading for the exit while another is settling in more deeply.

The honest objection

The strongest defence of this structure is that an OFS-only IPO is exactly what a mature, cash-generative, debt-light exchange should run. NSE does not need fresh capital to build a factory or fund a product launch; listing here mainly serves liquidity, governance discipline and price discovery for a company that already has 209,376 shareholders and a functioning secondary market in its unlisted shares. Seen that way, SBI, and any other institutional holder selling into the OFS, is doing exactly what equity ownership is for: realising value built up over years, at whatever price the market is willing to pay.

That case holds up. But it does not change what a retail investor is actually buying into on day one. The Rs 30,000 crore is a valuation being tested; none of it is capital being put to work inside NSE. A buyer who reads that this would be the largest IPO in Indian history and pictures growth capital flowing into the exchange has the wrong transaction in mind. What is actually on offer is a queue of existing owners, led by a public-sector bank that paid 80 paise a share, cashing in at whatever price the book-building process sets.

The Signal

NSE's IPO will be measured, fairly, by its size and its subscription numbers. But size is a fact about the sellers, not the company. The number worth watching is not the headline Rs 30,000 crore. It is the day-one price against SBI's Rs 0.80 acquisition cost and against the Rs 1,909.02 weighted-average secondary price that came before it: if the IPO prices near or above that secondary range, the market is confirming what long-term holders already believed their stake was worth. If it prices well below that range, the record label will have done more work than the valuation could support.

Reporting basis: every figure in this piece, the offer structure, the fresh-issue status, the shareholder acquisition costs and share counts across all ten selling shareholders, the secondary-market trading range, the profit and revenue figures, the shareholder count, the pending litigation, and the LIC board nomination, comes from NSE's Draft Red Herring Prospectus, filed with SEBI in June 2026. The estimated Rs 30,000 crore offer size and the comparison with Hyundai Motor India's 2024 IPO are as carried by The Tribune, an ANI wire item. The history of NSE's decade-long, co-location-scandal-delayed path to this filing is as reported by Outlook Business. The gap between SBI's acquisition cost and the weighted-average secondary price is The Signal's own calculation from those DRHP disclosures.