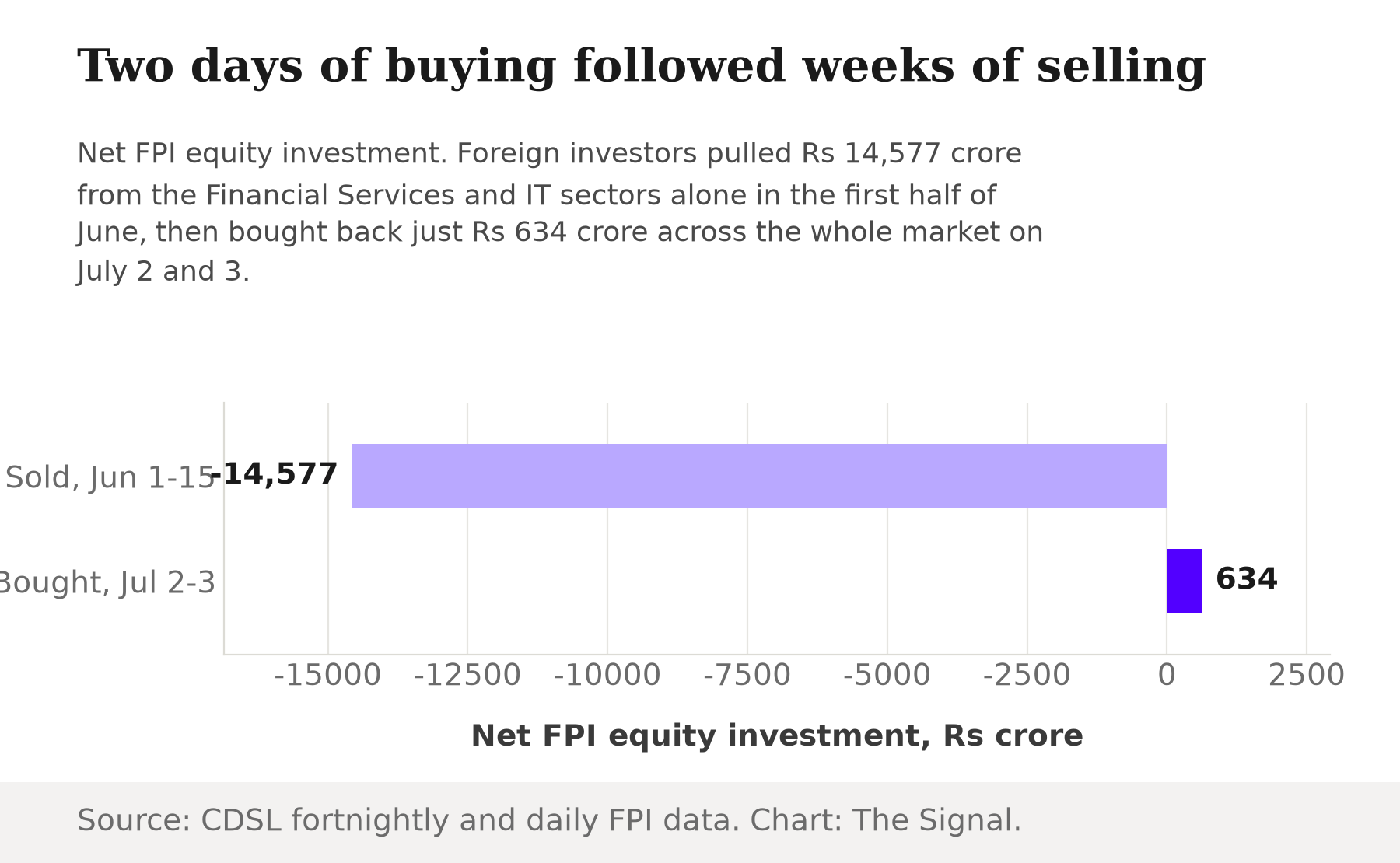

On June 9, 2026, the S&P 500 fell 1.7% and the Nasdaq Composite fell 2.9% as AI chipmakers led the slide, the opening jolt in a global selloff tied to doubts about the AI capital-spending boom. The jolts kept coming: on July 2, South Korea's Kospi dropped 7.89% to close at 7,648.09, tripping an intraday trading curb, on fears that Big Tech's AI spending may be cooling. Against that backdrop, India looked like the exception. Foreign portfolio investors, overseas funds registered to trade in Indian markets, turned net buyers of Indian equities on July 2 and July 3, the most recent two trading days CDSL has reported. They added Rs 60 crore and Rs 574 crore respectively (one crore is 10 million, so a combined Rs 634 crore). Put the two together and a tidy story appears: as the AI trade wobbles from Wall Street to Seoul, global money is parking in India instead.

It is worth slowing down on that. In the first half of June, foreign investors sold Rs 7,844 crore out of Financial Services and Rs 6,733 crore out of Information Technology alone, a combined Rs 14,577 crore pulled from just two sectors in two weeks. The "return" now being read as a safe-haven signal, Rs 634 crore bought back across the entire market on July 2 and 3 combined, is a small fraction of what left those two sectors alone the month before.

The July "return" is a fraction of what left in June.

Source: CDSL fortnightly sector-wise FPI data; CDSL daily FPI data. Combined figures are The Signal's calculations. Chart: The Signal.

Two sectors, not one, did the selling

The sector that led June's exodus was not the one most obviously tied to artificial intelligence. Financial Services lost Rs 7,844 crore to foreign selling in the first half of June, more than the Rs 6,733 crore pulled from Information Technology. If foreign money were fleeing an AI slowdown specifically, IT should have taken the bigger hit, since Indian IT services firms count large US technology clients among their customers. Instead banks and financial firms lost more, which points to broad de-risking across Indian equities generally, the kind that shows up whenever global risk appetite turns, not a narrow bet against Indian tech.

Why the market barely flinched

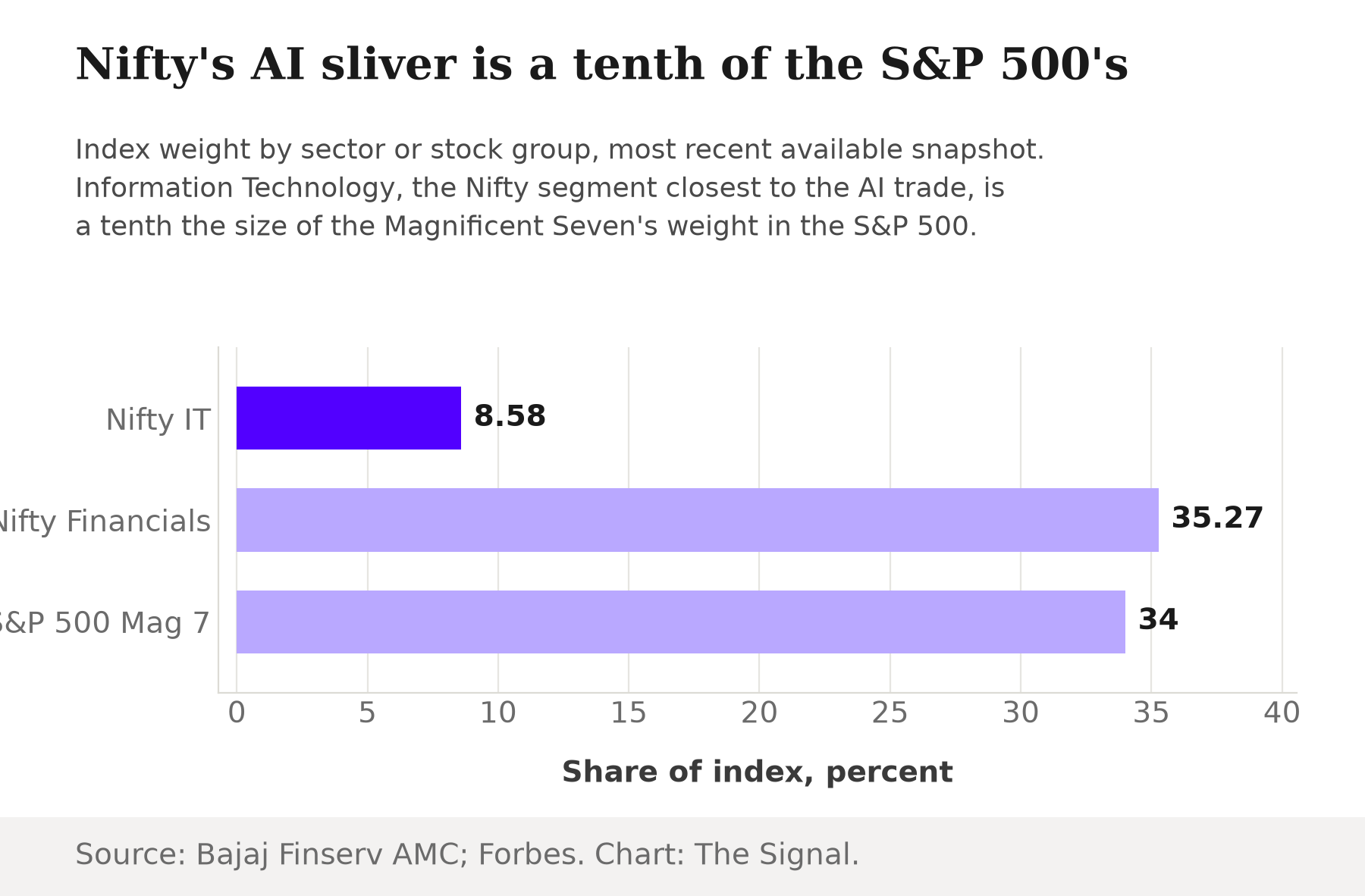

Even with money leaving, the Nifty never came close to the drop that hit Seoul. The reason has less to do with conviction than with arithmetic. Financial Services carries a 35.27% weight in the Nifty 50, more than four times Information Technology's 8.58%, as of April 30, 2026. The Magnificent Seven, the AI-exposed cohort at the center of the US rout, made up about 34% of the S&P 500 as of June 2026. Nifty's AI-adjacent slice is roughly a tenth the size of the American one, and the rest of the index, consumer staples, energy, autos, telecom, has little direct line to a US AI capex slowdown at all. A selloff in AI capital spending was never going to move India's index the way it moved Wall Street's or Seoul's, regardless of what foreign investors did with two days of buying.

Nifty's AI-exposed slice is a tenth the size of Wall Street's.

Source: Bajaj Finserv Asset Management; Forbes. Chart: The Signal.

The buyers holding up the floor are Indian

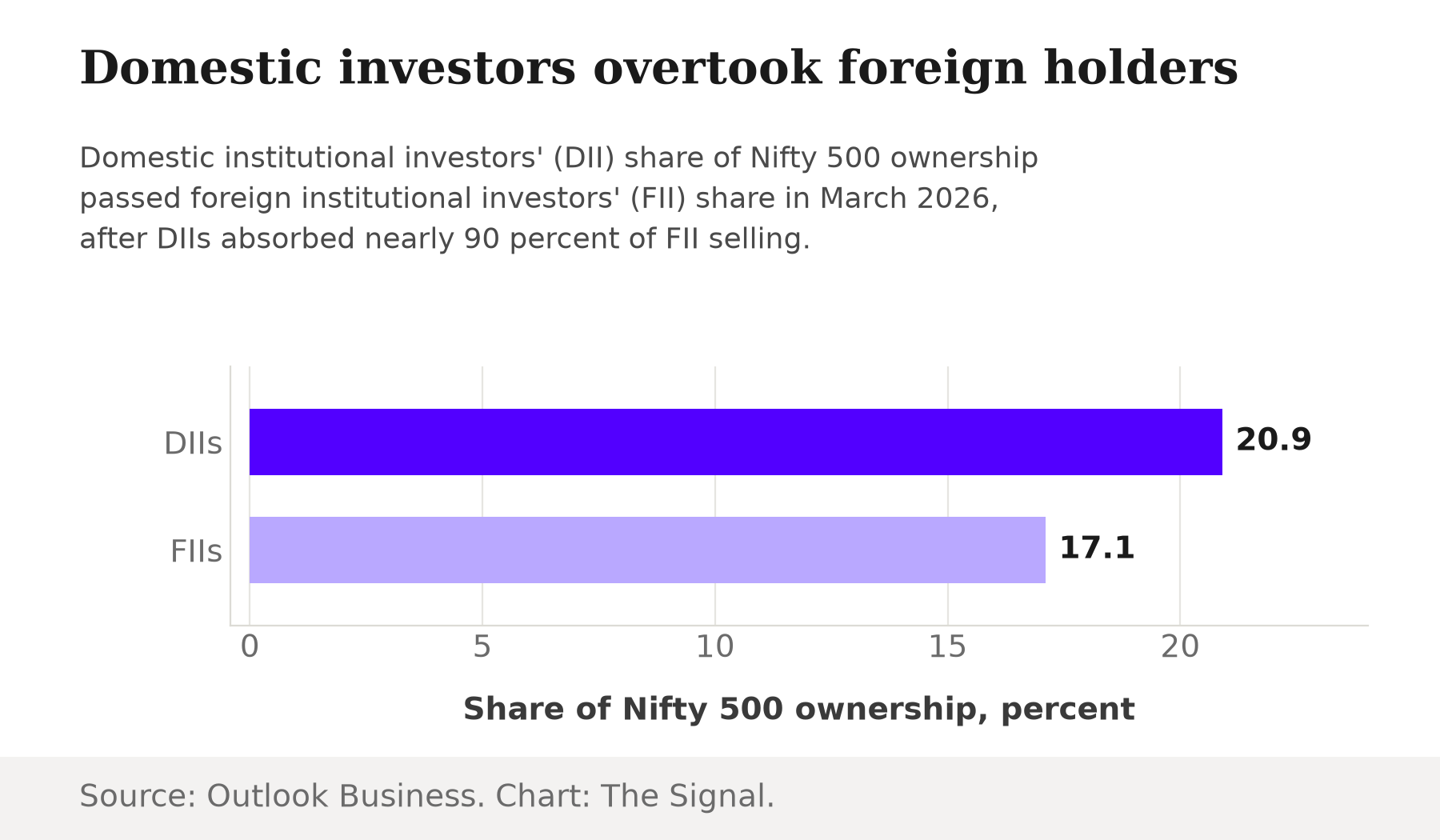

The steadier hand behind Indian equities through 2026 has been domestic, not foreign, money, and that shift predates the current selloff by months. Foreign institutional investors, FIIs, are the older name for the same foreign portfolio investors tallied above; both terms describe overseas funds holding Indian shares. Domestic institutional investors' ownership of the Nifty 500 climbed to a record 20.9% by March 2026, overtaking foreign institutional investors' 17.1% for the first time, as DIIs absorbed nearly 90% of FII selling. Two days of foreign buying in July did not change that balance. It landed on top of a market where the marginal buyer has been Indian mutual funds and insurers for months already.

The Nifty 500's ownership balance has tipped toward domestic funds.

Source: Outlook Business. Chart: The Signal.

The honest objection

The strongest case for the safe-haven read is valuation, not flow. The Nifty 50 traded at a price-to-earnings ratio of 20.9 on July 3, 2026, below its own five-year average of 22.3. A market that is not expensive by its own history has room to absorb real foreign buying without looking overheated, and if AI jitters persist, more of that money could plausibly find its way to India precisely because the valuation case does not require heroic assumptions. That argument is real.

But it describes a market that could absorb a re-rating, not one that is being re-rated. Two days of Rs 634 crore is not the kind of flow that moves a 20.9 multiple anywhere; it is a rounding error next to the Rs 14,577 crore that left financials and IT alone three weeks earlier. Cheap valuations make a future inflow plausible. They do not make the inflow that already happened bigger than it was.

The Signal

None of this makes India a false safe haven, only an accidental one. The Nifty held up because its dominant sector is banks, not chipmakers, and because Indian mutual funds have been the buyer of last resort since long before Wall Street's AI trade wobbled. If foreign investors are genuinely testing India as an alternative to AI-exposed markets, the number to watch is not the two-day tally CDSL just published. It is whether that daily net turns positive and stays there for weeks, not days, once the Nasdaq stops moving the headlines. Until then, the shelter is real, but nobody is renting it yet.

Reporting basis: the US equities selloff of June 9, 2026 is per Fortune, and the Kospi figures for July 2 are per The Korea Herald. Fortnightly sector-wise and daily net FPI investment figures are from CDSL, India's securities depository, drawing on its official fortnightly and daily publications. The Nifty 50's price-to-earnings ratio and its five-year average are from Trendlyne. The Magnificent Seven's weight in the S&P 500 is per Forbes, and the Nifty 50's sector weights are from Bajaj Finserv Asset Management's published composition data. The domestic-versus-foreign ownership crossover in the Nifty 500 is per Outlook Business. The combined Rs 14,577 crore outflow figure, the combined Rs 634 crore inflow figure, and the comparison between them are The Signal's calculations from those CDSL figures.