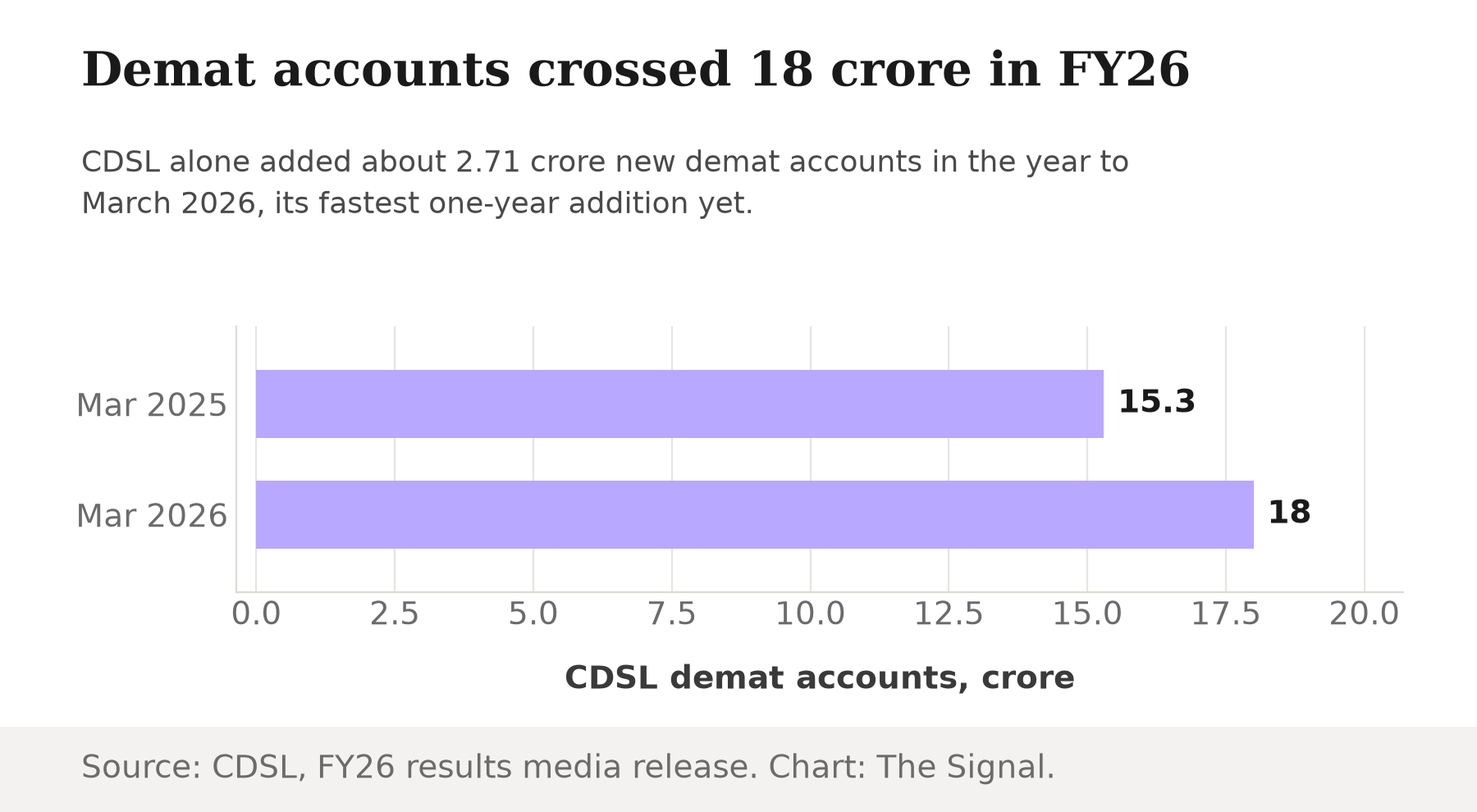

India's retail investing boom keeps setting records. Demat accounts, the accounts an investor needs to hold shares electronically, crossed 18 crore as of March 31, 2026, up from 15.30 crore a year earlier, after roughly 2.71 crore new accounts were opened during FY26 at CDSL alone. By August 2024, SEBI's own board papers counted more than 12 crore investors in the securities market. Every one of those investors, in principle, has a professional they can turn to for personalised guidance: a SEBI-registered investment adviser.

It is worth slowing down on that word, principle. The population of licensed advisers is not growing with the investor base. It is shrinking. "Today, there are around 1,000 registered investment advisers, 470 individuals and 530 non-individuals," SEBI Chairman Tuhin Kanta Pandey said in a March 2026 address, adding that "it is a matter of concern that the number of registered investment advisers has declined since 2021."

The vanishing adviser

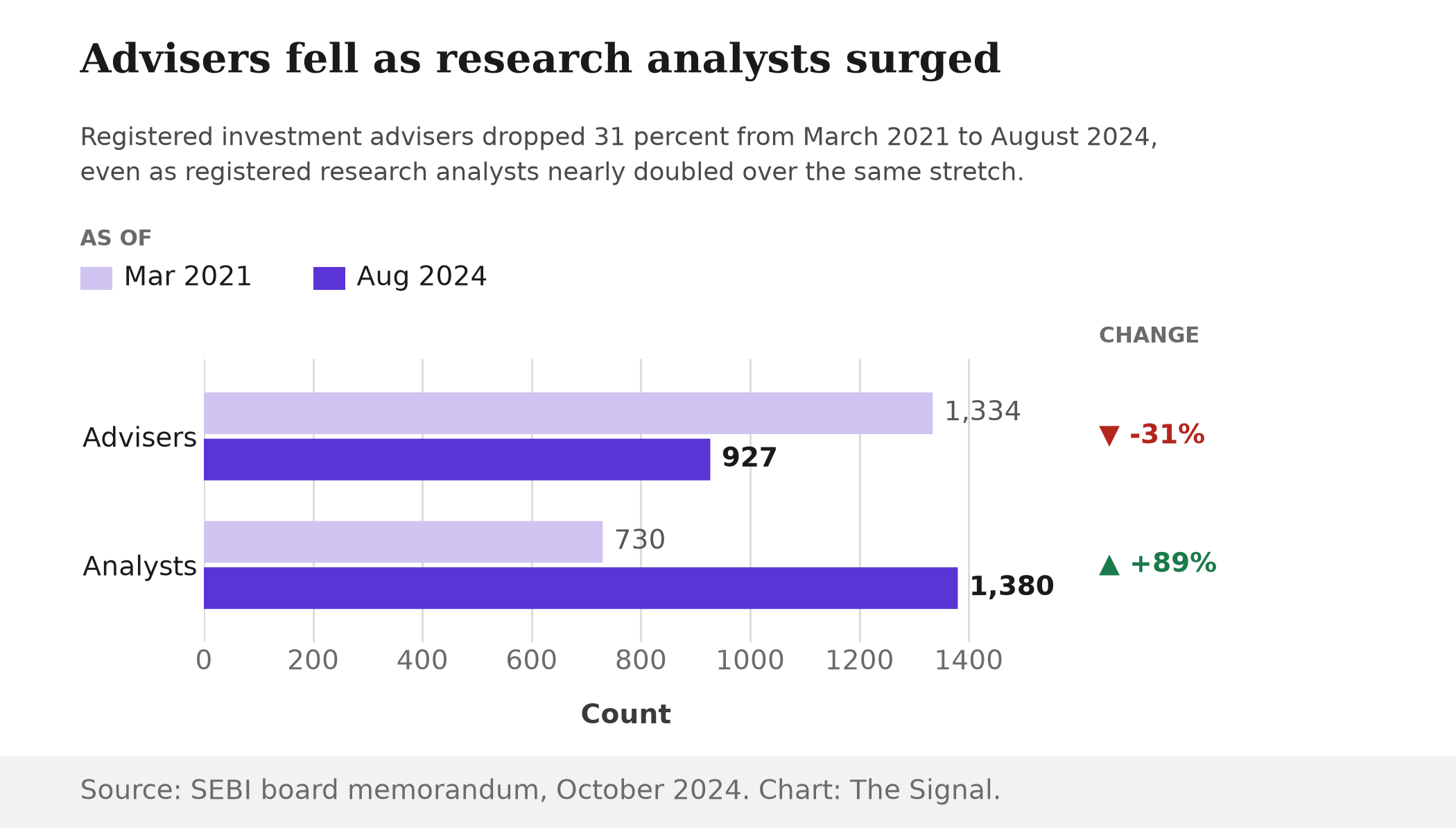

SEBI's own numbers show exactly how far the decline runs. A SEBI board memorandum dated October 2024 reports that the number of investment advisers fell from 1,334 in March 2021 to 927 by August 2024, even as the number of registered research analysts rose from 730 to 1,380 over the same stretch, while investors in the securities market numbered more than 12 crore. Divide one SEBI count by the other and the scale problem is stark: more than 12 crore investors and 927 licensed advisers works out to more than 129,000 investors for every adviser left standing, as of August 2024. The gap was already wide back when the adviser count started falling: CDSL's own investor presentation put its account count at 3.34 crore as of March 31, 2021, or roughly 25,000 accounts for every one of the 1,334 advisers then registered. By the time CDSL alone crossed 18 crore accounts in March 2026, against around 1,000 registered advisers, that ratio had widened to more than 180,000 accounts per adviser. The investor base did not just outgrow the adviser count once; it kept outgrowing it every year in between.

The price of a licence

The most concrete cost pushing advisers out is written into the regulations. SEBI's gazette notification of July 2020 raised the minimum net worth for individual investment advisers from Rs 1 lakh to Rs 5 lakh, and for non-individual advisers from Rs 25 lakh to Rs 50 lakh. That rule took effect in 2020, the same year the registered count began its slide. An individual adviser who could not show five lakh rupees in net tangible assets, or a small advisory firm that could not show fifty lakh rupees in net worth, no longer qualified to hold a licence.

SEBI raised the net worth bar for advisers in 2020.

| Adviser type | Net worth before July 2020 | Net worth after July 2020 |

|---|---|---|

| Individual | Rs 1 lakh | Rs 5 lakh |

| Non-individual | Rs 25 lakh | Rs 50 lakh |

Source: SEBI (Investment Advisers) (Amendment) Regulations, 2020.

The math advisers can't keep up with

The mismatch is not just historical. Match SEBI's own current adviser count against CDSL's own current account count and the gap for FY26 alone is just as wide: around 1,000 registered advisers against roughly 2.71 crore new demat accounts opened in the year to March 2026. That is our calculation: about 27,100 new demat accounts for every registered adviser in the country, opened in a single year. Most of those new accounts belong to people who will never sit across a table from a licensed adviser.

Who is filling the gap

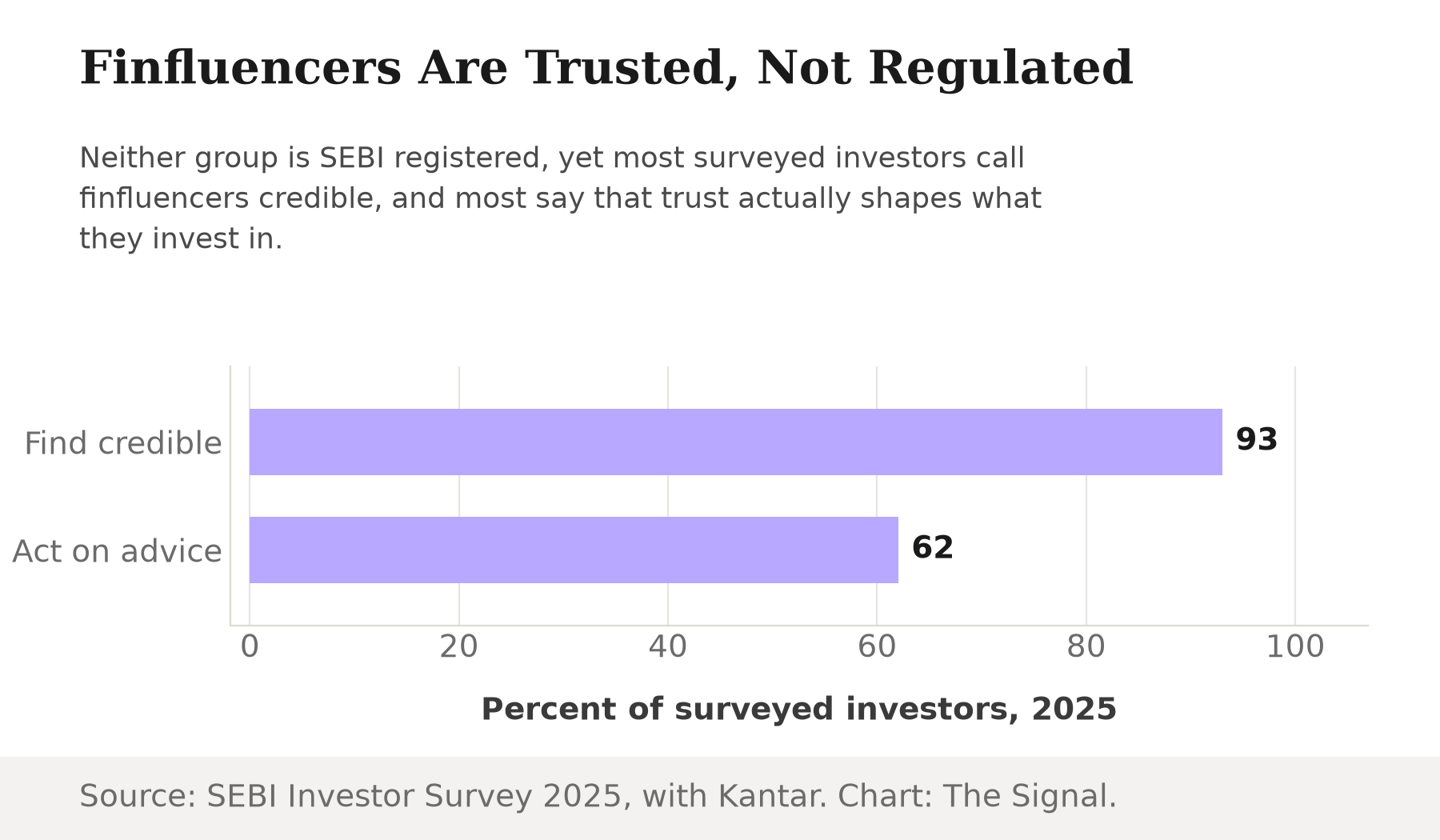

The gap is not going unfilled. It is being filled by people SEBI has not licensed at all. SEBI's Investor Survey 2025, conducted with Kantar, found that 62 percent of investors make some or most of their investment decisions based on recommendations from financial influencers on social media. The same survey found that 93 percent of investors consider these finfluencers moderately to highly credible, a trust level no licensing exam ever tested.

The honest objection

The strongest case against reading this as a hollowing-out is the research-analyst number itself. Registered research analysts, who publish securities research rather than manage client portfolios, rose from 730 in March 2021 to 1,380 by August 2024, nearly doubling over the same stretch that advisers fell. Perhaps advisers did not vanish so much as relicense: a firm priced out of the costlier investment-adviser tier could register as a research analyst instead and keep serving clients under a different label. SEBI's own figures cannot rule that possibility out.

But it does not explain the finfluencer numbers. A registered research analyst is still someone SEBI can examine, discipline, or delist. Ninety-three percent of investors calling an unlicensed social-media voice credible is not a relicensing story. It is a gap that a relicensed analyst, sitting inside the same shrinking pool of regulated professionals, does not fill.

The Signal

SEBI's own chairman called its registration trend "a matter of concern", even as the regulator counts more than 12 crore investors in the securities market. The compliance bar for a licence went up in 2020. The licensed population has been falling ever since. The investors did not stop arriving. They just stopped waiting for a licensed adviser to show up first.

Watch what SEBI does next, not what it says. SEBI has already put a concrete fix on the table: an August 2024 consultation paper proposed scrapping the minimum net worth requirement for advisers and research analysts altogether, replacing it with a deposit lien-marked to a stock exchange instead. If that proposal, or something like it, actually clears the compliance bar SEBI itself built in 2020, the adviser count should turn. Tighten the finfluencer channel instead, without cutting that cost, and investors will simply have fewer places to go for advice they already trust ahead of the licensed kind. A regulator can rewrite its rules faster than it can add names to its own register of advisers. Until it does, a source of investment advice that answers to no one keeps gaining ground on the one that does.

Reporting basis: the adviser and research-analyst counts for 2021 and 2024, and the more-than-12-crore investor figure, are from a SEBI board memorandum dated October 2024. The current adviser count, its individual and non-individual split, and the "matter of concern" characterisation are from SEBI Chairman Tuhin Kanta Pandey's March 2026 address at ARIA Aspire 2026, per SEBI's own record of that speech. The finfluencer trust and decision-influence figures are from SEBI's Investor Survey 2025, conducted with Kantar. The 2020 net worth thresholds are from SEBI's gazette notification of that year. The demat account totals are from CDSL's own FY26 results media release; the March 2021 investor-account figure is from CDSL's own investor presentation for that quarter. The proposal to replace the net worth requirement with a deposit is from SEBI's August 2024 consultation paper on the IA/RA framework. The investors-per-adviser ratios and the new-accounts-per-adviser figure are The Signal's calculations from those figures.