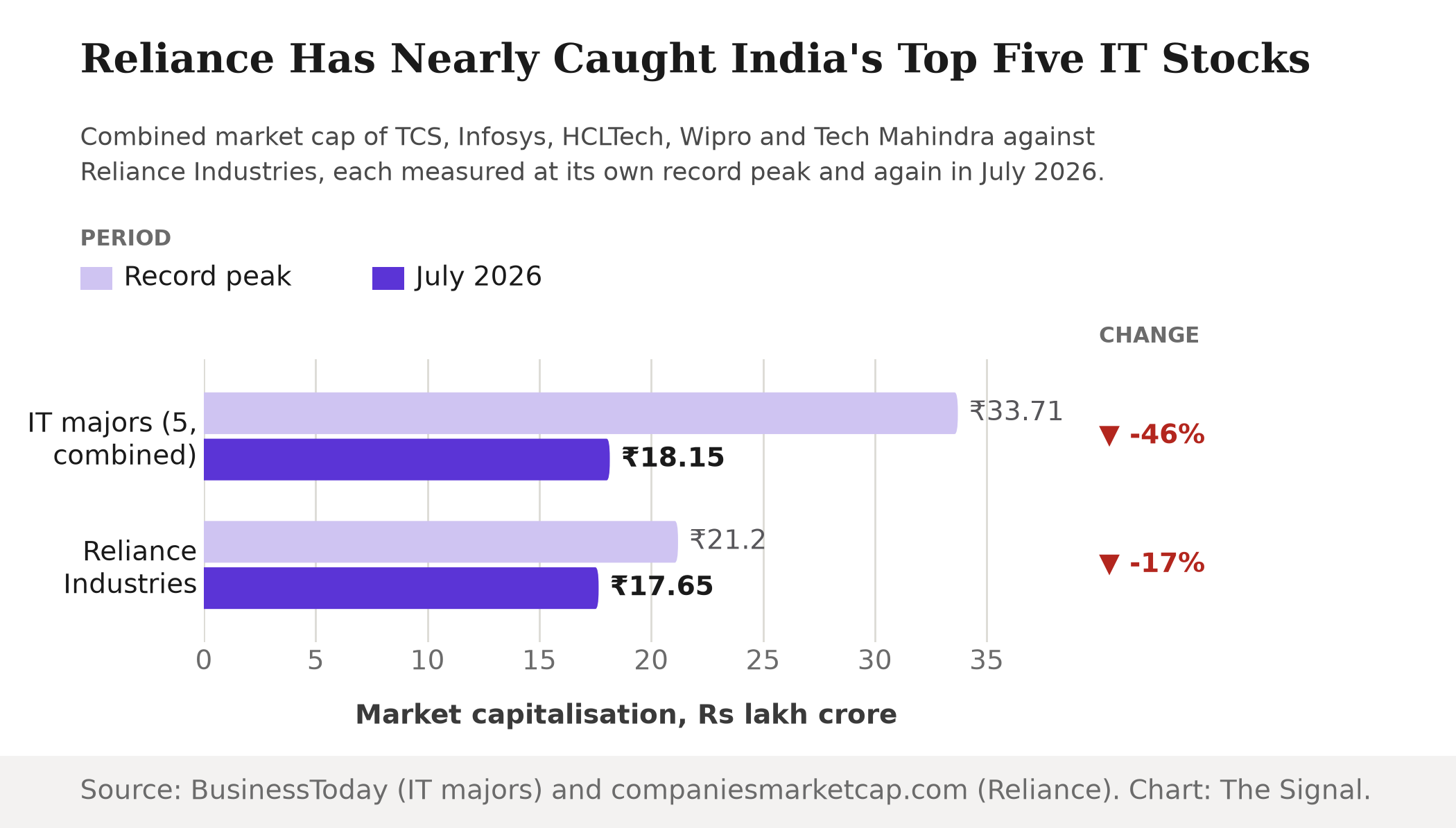

The easy read is that Reliance Industries has pulled decisively clear of India's software giants. On July 1, 2026, the Nifty IT sub-index fell 2.01% in a single session, with Infosys, TCS, Wipro and HCL Technologies all touching 52-week lows, as analysts cited macroeconomic uncertainty, AI-related disruption and geopolitical challenges weighing on the sector. Three days later, the combined market capitalisation of TCS, Infosys, HCL Technologies, Wipro and Tech Mahindra had fallen more than 46% from its record Rs 33.71 lakh crore in August 2024 to about Rs 18.15 lakh crore. That figure has all but converged with Reliance Industries' own market cap of Rs 17.65 lakh crore, itself down 16.7% from its record Rs 21.2 lakh crore in June 2024.

It is worth slowing down on that convergence, because the two lines did not arrive at the same point the same way.

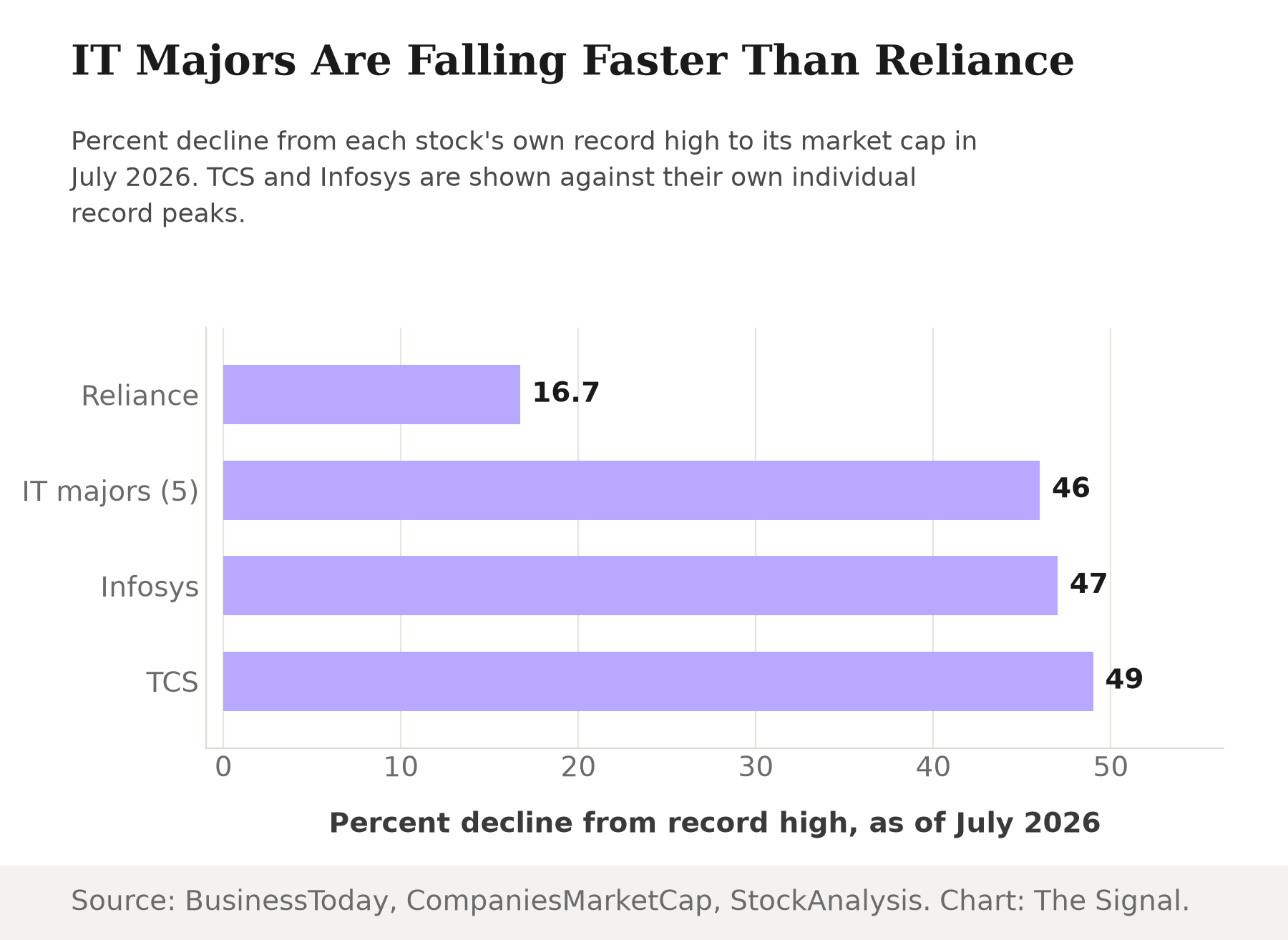

At those 2024 peaks, the gap between the two stood at Rs 12.51 lakh crore: Rs 33.71 lakh crore for the IT majors against Rs 21.2 lakh crore for Reliance. Today it is about Rs 50,000 crore, Rs 18.15 lakh crore against Rs 17.65 lakh crore. Reliance did not close that gap by rising. It closed because the IT majors are falling at roughly two and three-quarter times Reliance's own rate of decline, 46% against 16.7% from each side's own peak.

The asymmetry, stock by stock

TCS and Infosys, the two most valuable of the five, have fared no better looked at individually than the group did combined.

TCS and Infosys have each shed close to half their peak market value.

| Company | Record peak | Market cap, July 2026 | Decline |

|---|---|---|---|

| TCS | Rs 14.82 lakh crore (Dec 31, 2024) | Rs 7.57 lakh crore (Jul 2, 2026) | ~49% |

| Infosys | Rs 8.02 lakh crore (Dec 31, 2021) | Rs 4.24 lakh crore (Jul 2, 2026) | ~47% |

Source: stockanalysis.com, TCS; stockanalysis.com, Infosys.

TCS's market cap has fallen from a record Rs 14.82 lakh crore on December 31, 2024 to Rs 7.57 lakh crore on July 2, 2026, a decline of nearly 49%. Infosys has fallen further back in time, from a peak of Rs 8.02 lakh crore on December 31, 2021 to Rs 4.24 lakh crore on July 2, 2026, a decline of nearly 47%. Neither company has had a single catastrophic quarter; both have simply kept losing ground for years, and the market has kept marking them down for it.

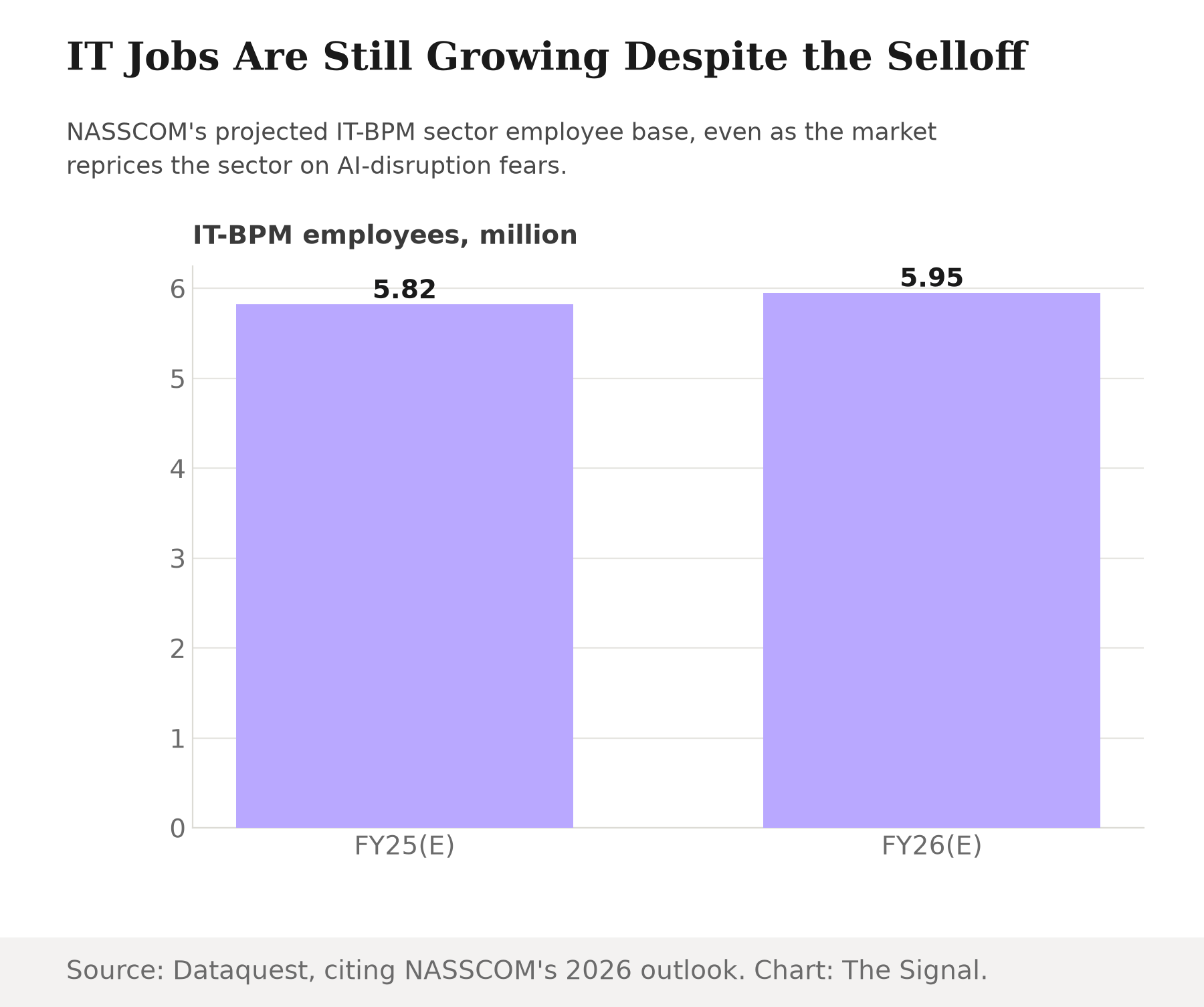

The fundamentals have not caught up with the fear

None of this shows up yet in the sector's underlying business, at least not in the most recent numbers available. India's exports of software services rose 7.3% to US$204.7 billion in the year to March 2025, per the Reserve Bank of India's annual survey of exporting companies, the latest such survey published. On staffing, NASSCOM projects the IT-BPM sector's employee base will grow from 5.82 million in FY25(E) to 5.95 million in FY26(E), a net addition of about 135,000 jobs, per the industry body's Technology and Leadership Forum 2026 outlook, as reported by Dataquest. Both figures are annual estimates, not live prices, so they will not move as fast as the stock does in either direction. But they are the most current published reads on the actual business, and neither shows contraction.

That gap, a shrinking share price sitting on top of still-growing exports and still-growing headcount, is exactly what a market looks like when it is repricing an assumption about the future (that AI will hollow out the outsourcing model) rather than a fact already visible in the numbers.

The mechanism passive funds cannot escape

There is a second-order effect the share prices alone do not show. SEBI's mutual fund regulations cap a scheme's exposure to any single company at 10% of net asset value, but explicitly exempt index funds, which must instead mirror the weightings of the scrips in the index they track. As the IT majors' combined weight in the Nifty shrinks and Reliance's holds up in relative terms, every rupee that flows into a Nifty index fund is mechanically directed toward more Reliance and less of each IT major, not because any fund manager chose that tilt, but because the rule requires it. A repricing that started as a sector story becomes a concentration story for anyone holding a passive Nifty fund, without that investor making a single active decision.

The honest objection

The strongest case against reading this as an IT-specific unraveling is that Reliance has fallen too. Its own market cap is down 16.7% from its June 2024 peak, which looks like broad market weakness dragging everything down together, not a verdict on outsourcing specifically. On that reading, the "convergence" is coincidence: two large-cap stocks drifting lower in the same soft market, meeting in the middle by chance.

That case is real, but it does not survive the size of the gap. A stock down 17% and a sector down 46% are living through two different markets. Nifty IT alone fell 2.01% in a single session on July 1, 2026, with four of its biggest constituents hitting 52-week lows together, a sector-specific move rather than an index-wide one. Broad weakness explains a shared direction. It does not explain a nearly three-fold difference in speed.

The Signal

The headline that Reliance has "overtaken" India's IT majors is not quite right yet. On the numbers, the five combined, at Rs 18.15 lakh crore, are still slightly ahead of Reliance's Rs 17.65 lakh crore. The crossover may happen within a quarter at current trend lines, but the widening distance between what the market is pricing and what the industry is reporting matters more: a share price collapse running nearly three times faster than Reliance's own, sitting on top of software exports and headcount that were still growing as of the last annual reads available. Markets are allowed to price the future before it arrives. The number to watch next is whether NASSCOM's and the RBI's next annual figures start bending down too. That is the difference between a market correctly pricing a coming disruption and a market that got ahead of itself.

Reporting basis: the combined market cap of the five listed IT majors and the July 1, 2026 Nifty IT session are per BusinessToday's reporting of NSE and BSE data, including its separate report on the July 1 Nifty IT session. Reliance Industries' market cap is per companiesmarketcap.com's exchange-sourced tracker. TCS's and Infosys's individual peak-to-present figures are per stockanalysis.com's NSE-sourced market-cap histories, for both companies. Software-export growth for 2024-25 is from the Reserve Bank of India's annual survey of exporting companies. The IT-BPM employment projection for FY25(E) and FY26(E) is from NASSCOM's Technology and Leadership Forum 2026 outlook, as reported by Dataquest. The mutual-fund single-stock cap and its index-fund exemption are per SEBI's Mutual Fund Regulations. The decline percentages, the ratio between the IT majors' and Reliance's respective drawdowns, and the rupee gap between the two peak-to-present are The Signal's calculations from those figures.