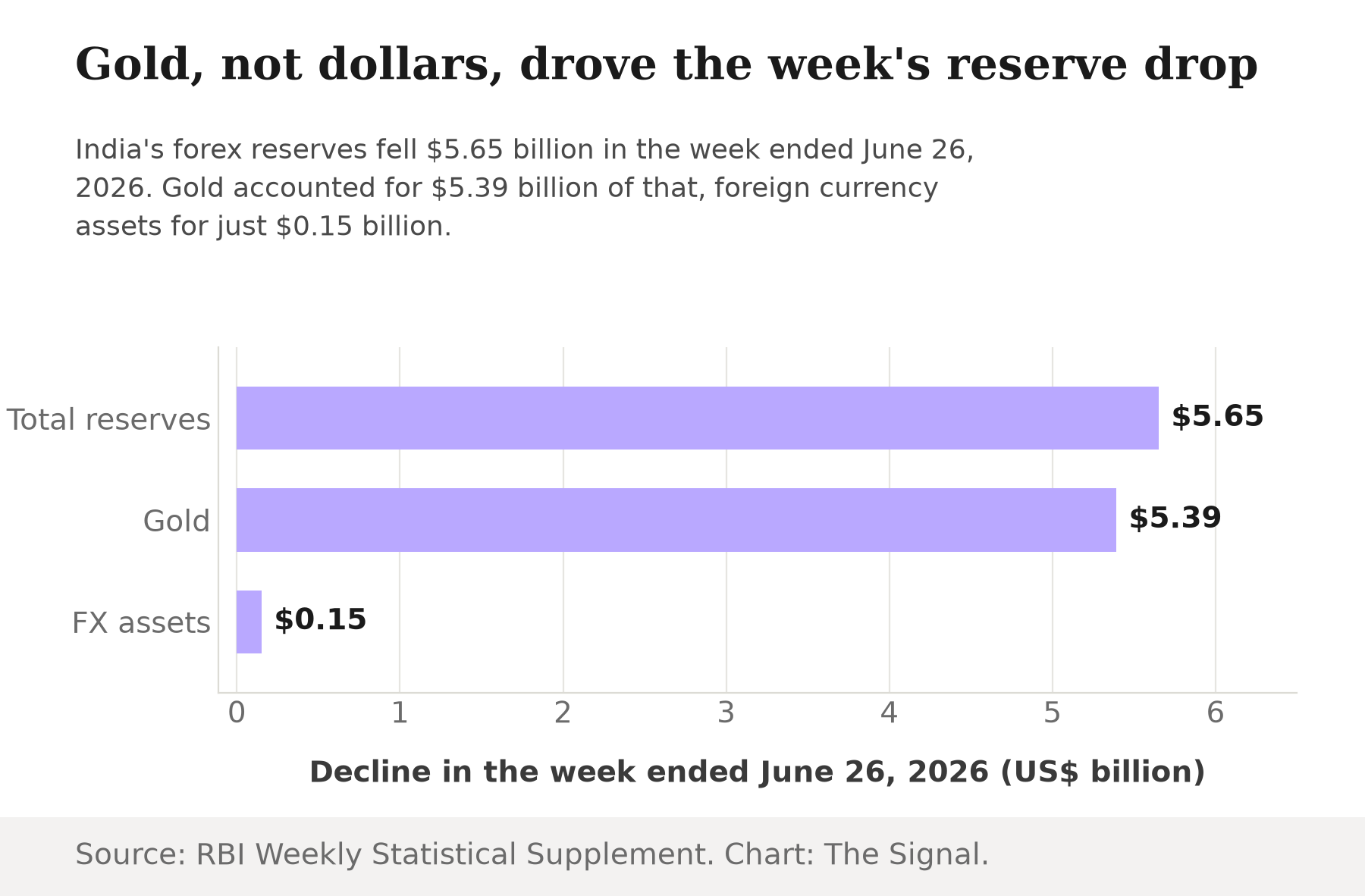

India's foreign exchange reserves fell to their lowest level in 15 months in the latest week the RBI has reported. The RBI's Weekly Statistical Supplement reports reserves dropped $5.65 billion in the week ended June 26, 2026, to $666.93 billion. The obvious read writes itself: the central bank has been selling dollars to hold up the rupee, and the war chest is thinning out.

It is worth slowing down on that read. Split the week's decline into its two components and the currency-defense story barely appears. Gold accounted for $5.39 billion of the $5.65 billion drop, while foreign currency assets, the part of the reserves the RBI would actually spend to defend the rupee, slipped just $150 million. Divide the two figures and gold's share of the week's loss comes to roughly 95 percent. Gold did almost all of the damage, and the RBI's actual dollar firepower barely moved.

From a record high to a 15-month low

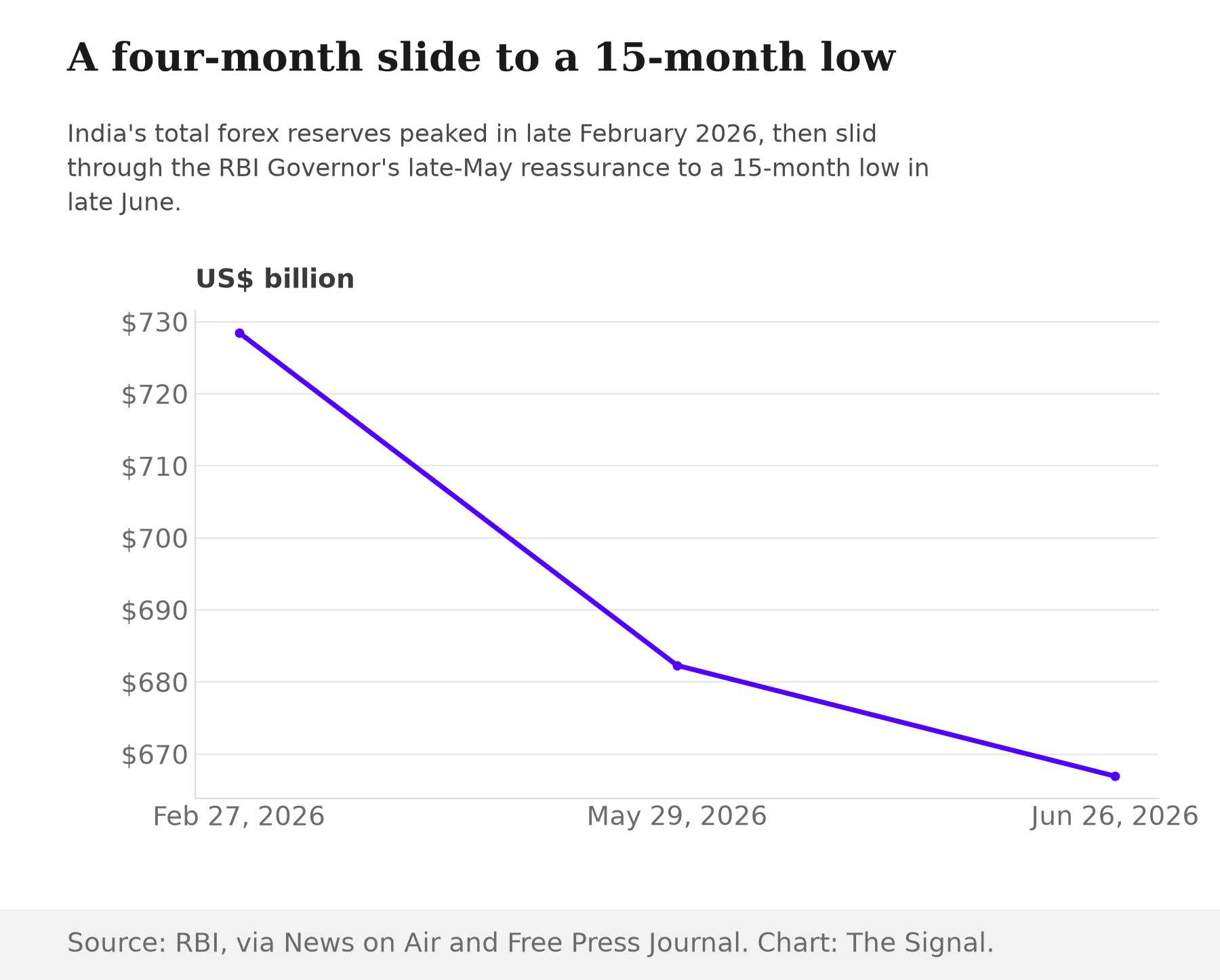

Four months earlier, reserves were at a record. They surged to an all-time high of $728.49 billion in the week ended February 27, 2026, with gold at $131.63 billion, up $4.14 billion that week alone, and foreign currency assets above $573.12 billion, government broadcaster News on Air reported, citing RBI data. Reserves eased through the spring: RBI Governor Sanjay Malhotra said on June 5, 2026 that reserves stood at $682.3 billion as of May 29, 2026, providing about 11 months of import cover, a figure he framed as a strong external buffer. Three weeks after that reassurance, the total had fallen another $15.4 billion to the 15-month low.

The gold price did this, not a change in policy

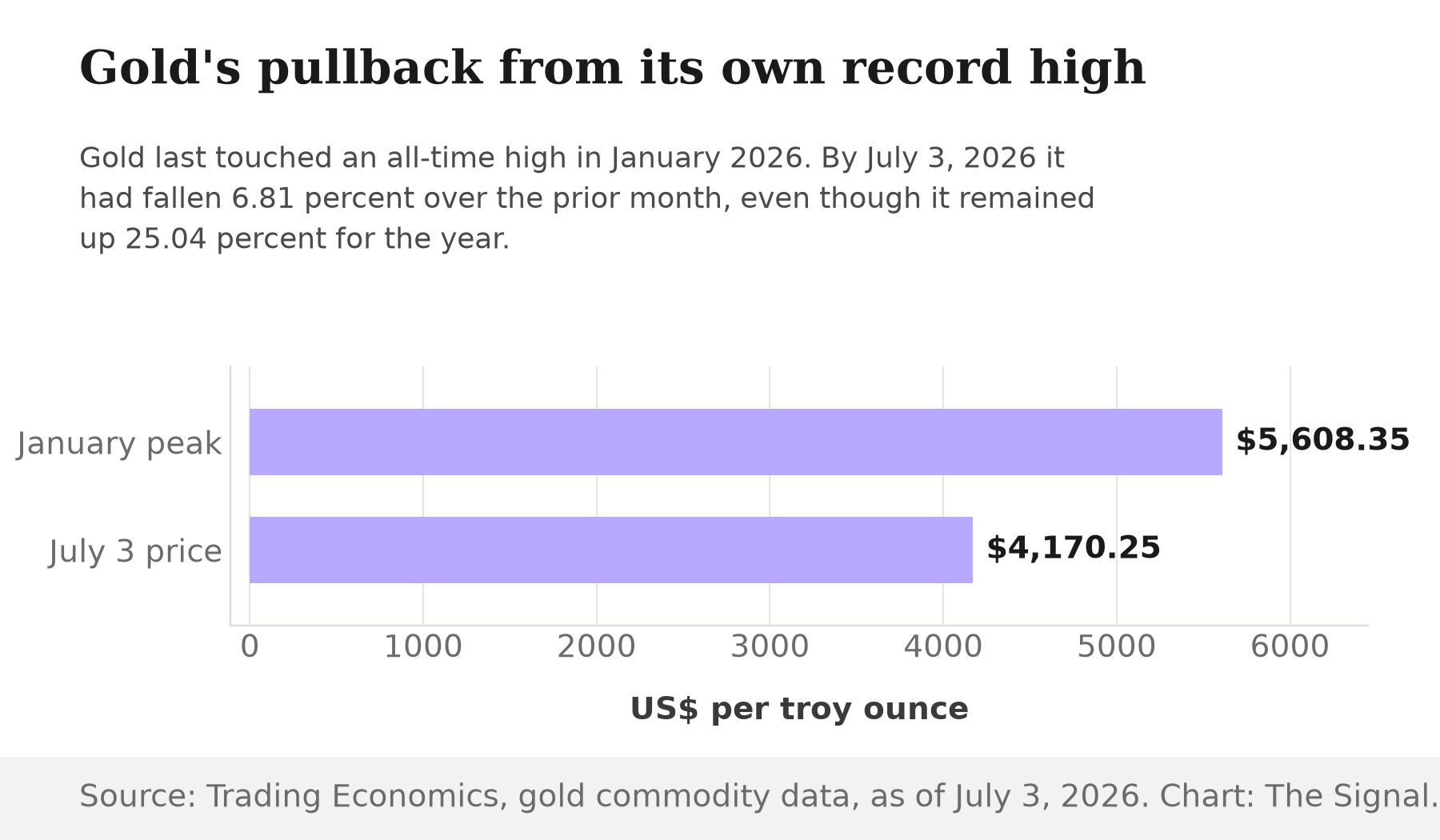

The reason gold's dollar value fell $5.39 billion in a single week has little to do with the RBI trading metal. Gold itself was down 6.81 percent over the month to July 3, 2026, trading at $4,170.25 a troy ounce, well off the $5,608.35 all-time high it touched in January 2026. A reserve manager does not have to sell a single bar for the dollar value of its gold holdings to fall. If the metal's own price retreats, the balance sheet marks the holding down automatically, exactly as it would mark up a currency position that moved the other way.

Even after that pullback, gold remained up 25.04 percent for the year to July 3, 2026, which reads far more like a rally cooling off than the start of a reversal. A metal still up a quarter for the year can give back six percent in a single month without its longer climb being over.

The tonnage data backs this up directly. RBI's physical gold tonnage rose from 879.58 tonnes on March 31, 2025 to 880.52 tonnes on March 31, 2026, and on June 3, 2026 the RBI issued an official clarification stating its physical stock remained unchanged at 880.52 tonnes, refuting media reports it had sold roughly $12 billion of gold. The tonnage was never in question that week; only the metal's price was.

The currency defense is real, it just shows up elsewhere

The rupee's own defense is a separate, and genuinely active, story, just not the one the gold line tells. The rupee weakened to an all-time low of about 97.11 per dollar on May 19, 2026, before recovering to trade near 94.51 to 95.29 per dollar by July 1, 2026. On June 5, 2026, the RBI said it would bear the full FX hedging cost for banks raising fresh three to five year FCNR(B) deposits through September 30, 2026, a step MUFG Research notes echoes the central bank's 2013 playbook for defending the currency under pressure. That tool works on the currency side of the balance sheet. It has no reason to touch the gold line at all, and in the week that produced the 15-month low, it did not: foreign currency assets fell only $150 million.

The wider gold story India's dip does not fit

Set against the global picture, India's one-week gold markdown looks even more like noise than signal. A World Gold Council survey of 76 central-bank reserve managers, fielded between February 5 and May 19, 2026, found a record 45 percent expect their own institution's gold holdings to grow over the next 12 months, and 89 percent expect global central-bank gold holdings to rise.

A record share of the world's reserve managers plan to keep adding gold.

| What the survey asked reserve managers | Share expecting an increase |

|---|---|

| Their own institution's gold holdings, next 12 months | 45% |

| Global central-bank gold holdings overall, next 12 months | 89% |

Source: A World Gold Council survey, reported by Kitco News. Survey fielded February 5 to May 19, 2026.

A record 45 percent of central banks plan to add to their own gold holdings over the next 12 months. Against that backdrop, India's single week of gold-price-driven markdown should not read as a reversal of appetite.

The honest objection

The strongest case against treating this as a valuation blip is that one week is a thin reed. Gold fell 6.81 percent over the month to July 3, 2026, and if that slide continues, next week's RBI release could show a further markdown even without the RBI selling anything, which would start to look like a genuine multi-week drag rather than a rounding effect. It is also true that the RBI does periodically rebalance the composition of its reserves between gold and currency, and the weekly release reports the value changes without explaining the reasons behind them, so in principle a deliberate sale could not have been ruled out from the weekly value data alone. But the RBI's own tonnage record closes that gap: physical holdings rose over the year to March 2026, and the central bank's June 3, 2026 clarification put the tonnage at an unchanged 880.52 tonnes, just three weeks before the week this piece covers.

That case is real, but it sits awkwardly with the timeline. Gold remained up 25.04 percent for the year even after its monthly slide, an odd week to start unwinding a position still deep in profit. And the RBI's own crisis-defense tool, the FCNR(B) hedging offer announced June 5, 2026, was aimed squarely at the currency side of the ledger, precisely where you would expect a central bank to spend effort if the underlying story here were really about defending the rupee.

The Signal

The headline number invites a currency-crisis read: reserves at a 15-month low, therefore the RBI must be burning dollars to hold the line. The accounting says otherwise, at least for the week that produced the number. Gold, not the currency book, did roughly 95 percent of the damage, and gold moved because the metal's own price came off a January 2026 peak. India's reserve managers never changed their minds about holding it. A record share of the world's central banks plan to add gold over the next year, by the World Gold Council's count, and India's own reserve managers followed the same pattern: RBI's physical gold tonnage grew over the year to March 2026. The line to watch for the real tell is foreign currency assets. If FCA starts falling by billions in a single week, that is the RBI spending down its actual firepower. If gold keeps swinging while FCA stays flat, the reserves number is just doing what a market price does when a rally cools. A 15-month low sounds like a warning. This one is mostly an accounting artifact of a metal correcting from its own record high.

Reporting basis: the weekly reserves and gold/foreign-currency-asset breakdown for the week ended June 26, 2026, is per the RBI's Weekly Statistical Supplement. The February 27, 2026 all-time high is per News on Air's account of RBI data. RBI Governor Sanjay Malhotra's May 29, 2026 reserves figure and import-cover statement are per the Free Press Journal's account of his announcement. Gold's spot price, its January 2026 all-time high, and its monthly and year-to-date changes are per Trading Economics market data as of July 3, 2026. The rupee's 2026 trading range is per Pound Sterling Live's daily exchange-rate history. The RBI's FCNR(B) hedging measure and its 2013 parallel are per MUFG Research's note on the central bank's policy announcement. The World Gold Council survey findings are as carried by Kitco News. RBI's physical gold tonnage figures and its June 3, 2026 clarification are per The Federal's account of the central bank's statement. The share of the week's decline attributable to gold, and the four-month change from the February 2026 peak to the June 2026 low, are The Signal's calculations from those RBI figures.