India's primary market closed the 2025-26 financial year, April 2025 through March 2026, looking unambiguously strong. The year produced a record 366 IPOs that together raised approximately ₹1.9 trillion, a 9.5 percent increase over FY25, anchored by a record 109 mainboard listings worth ₹1.7 trillion, SEBI's April 2026 Monthly Bulletin reports. Add debt and REIT and InvIT issuance to that equity total and the whole primary market looks larger still: Indian corporates mobilised ₹13.92 lakh crore across equity, debt and REIT and InvIT issuances combined in FY26, per the same bulletin's tally of fund mobilisation by corporates. The country backed up the headline count on the world stage too. In March 2026, India was the world's second-busiest IPO market, with a 14 percent share and 20 listings, trailing only China's 24 percent share and 38 listings, SEBI's bulletin shows, citing Bloomberg data.

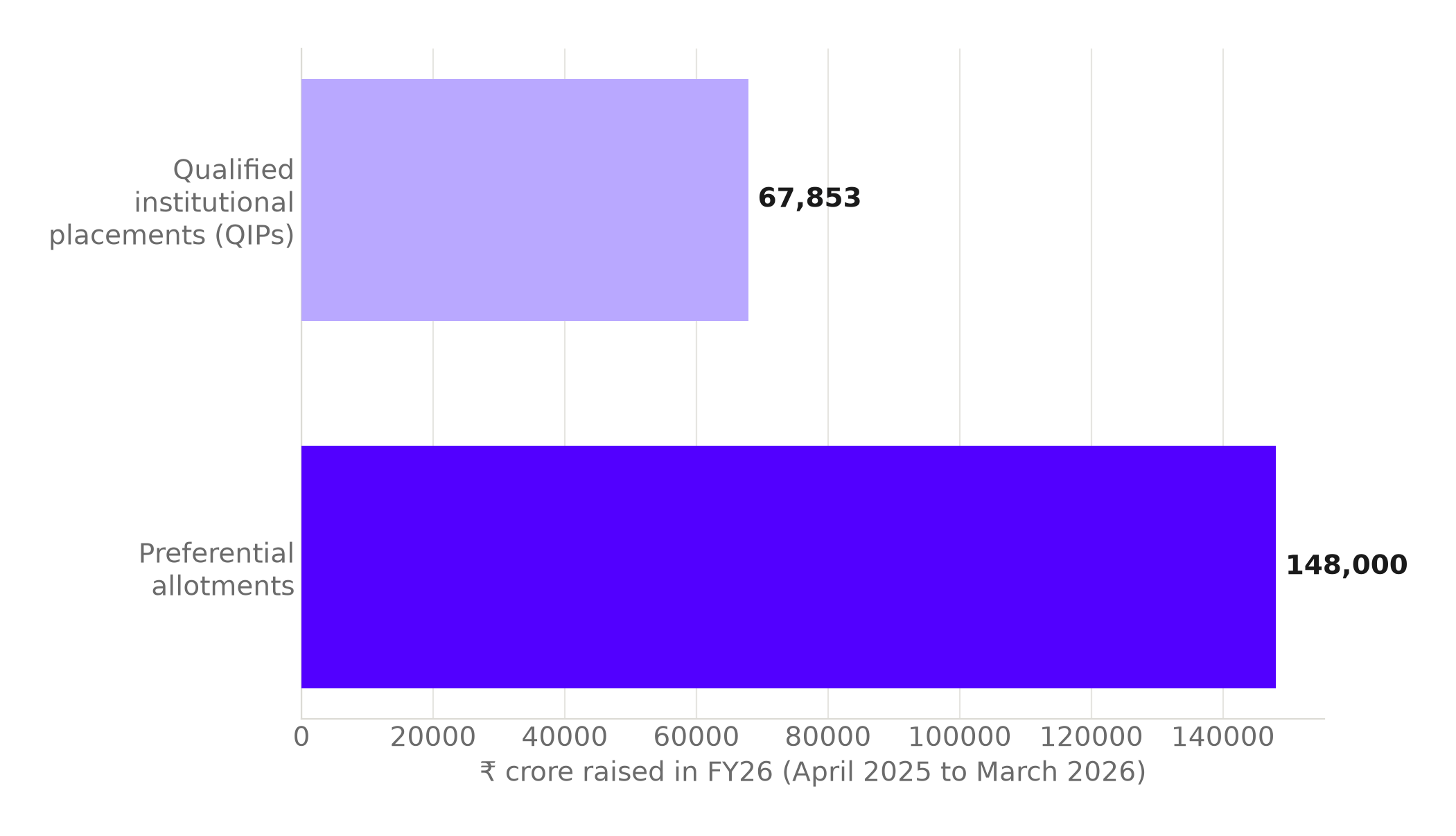

It is worth slowing down on that record before reading it as one continuous story. Even as IPOs and rights issues hit multi-year highs, capital raised through qualified institutional placements, the route open to a broad set of institutional buyers, contracted 50 percent in FY26 to ₹67,853 crore, while preferential allotments, a more negotiated and concentrated route, surged 76 percent to ₹1.48 trillion, SEBI's bulletin reports. The record year already had a narrowing current running underneath it: money was shifting toward a route negotiated directly with a smaller, chosen set of buyers, even as the headline totals climbed.

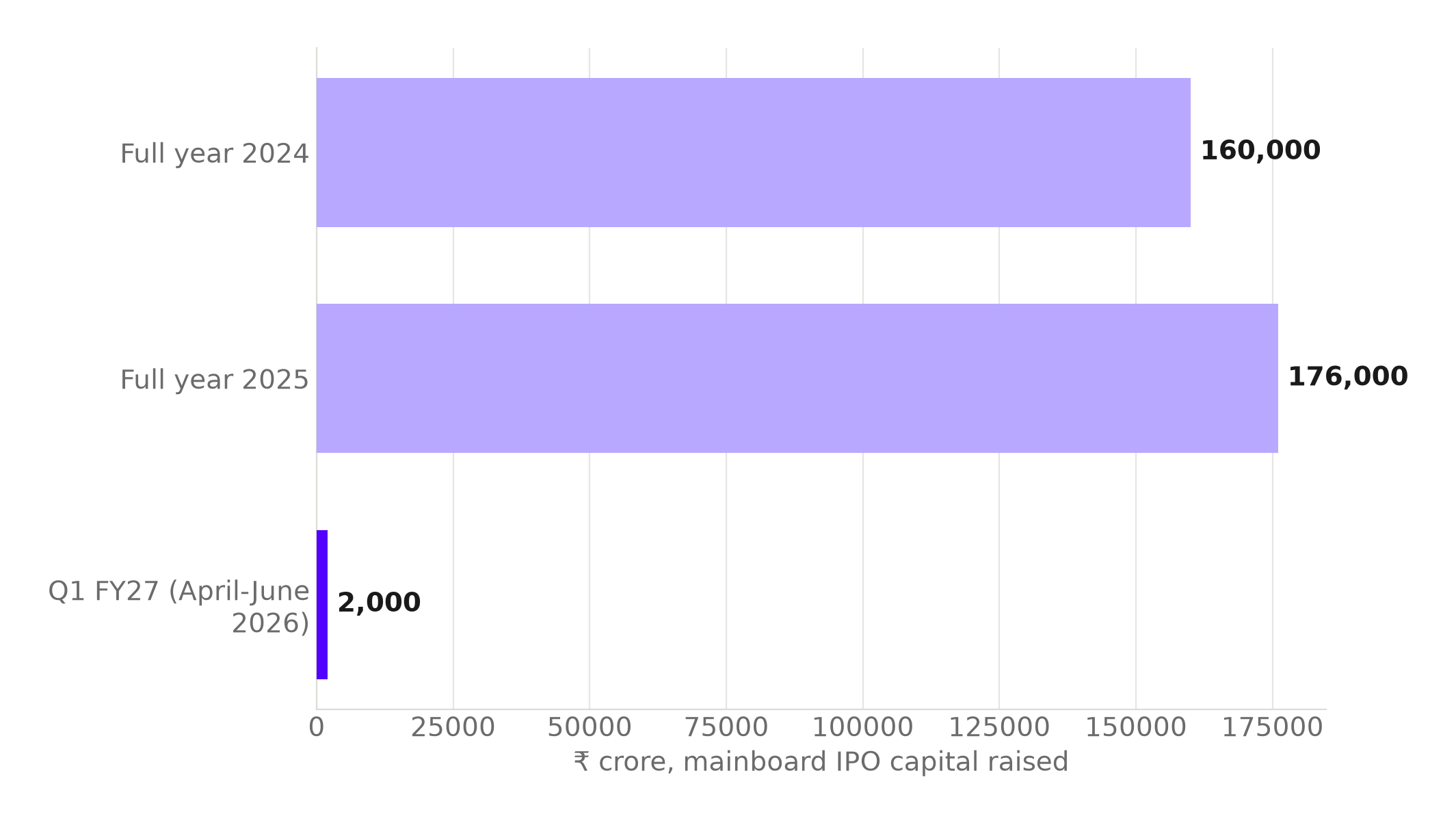

Strip out FY26 altogether and look at what came right after it, and that narrowing current turns into a full stop. Only five mainboard IPOs listed in the first three months of FY27, April to June 2026, raising a little more than ₹2,000 crore combined, against ₹1.6 lakh crore that India Inc raised in all of 2024 and ₹1.76 lakh crore in all of 2025, Business Today reports. A quarter is always smaller than a full year, but roughly ₹2,000 crore against a normal year's ₹1.6 lakh crore to ₹1.76 lakh crore is barely more than one percent of it, not a quarter's fair share.

Mainboard fundraising did not slow down. It stopped.

Five listings raised close to nothing next to two full years of six-figure totals.

Source: Business Today. Chart: The Signal.

Three deals are doing the lifting

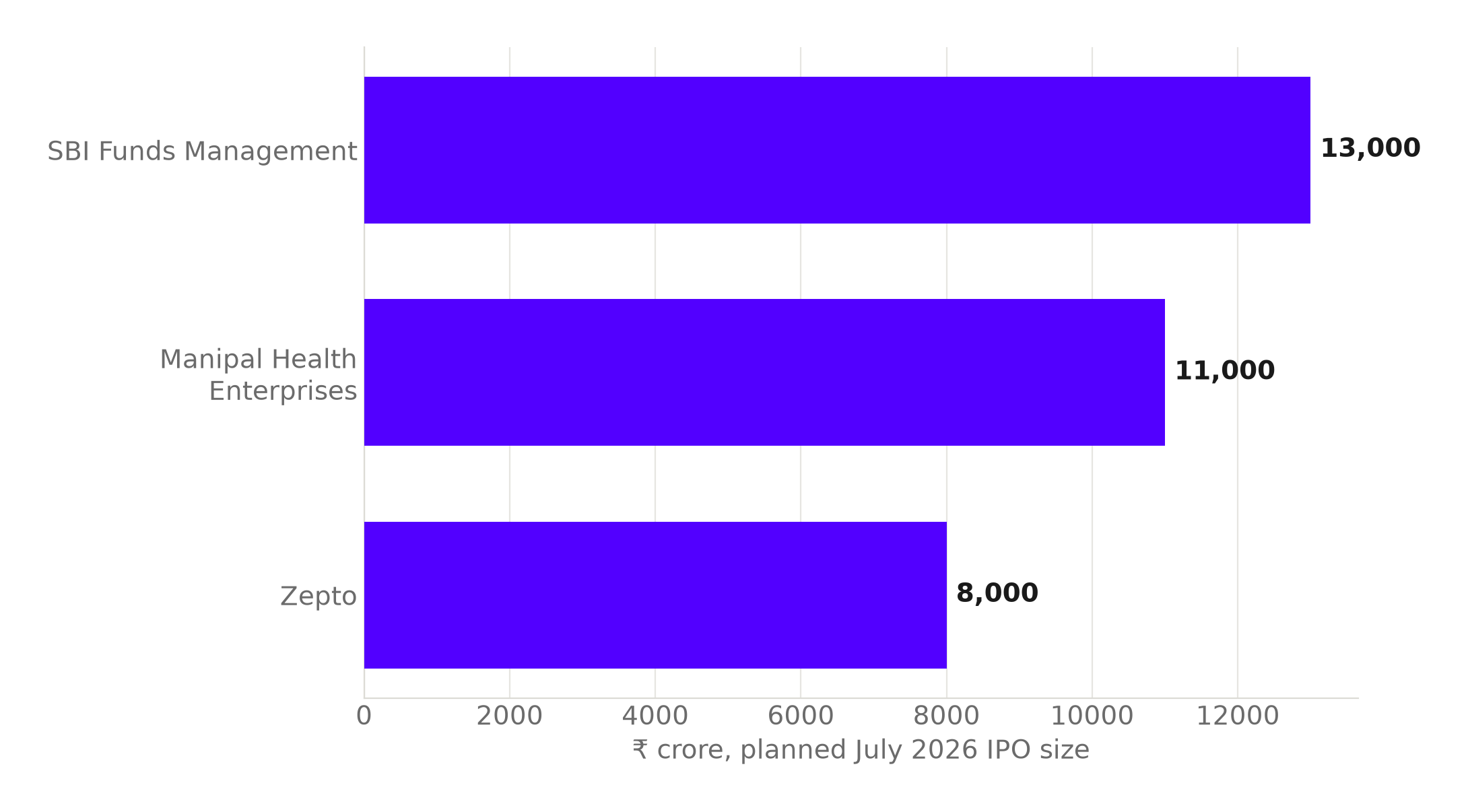

The mainboard market did not stay quiet for long. July 2026 alone lines up roughly ₹45,000 crore of mainboard IPOs, led by SBI Funds Management at around ₹12,000 to ₹13,000 crore, Manipal Health Enterprises at ₹11,000 crore and Zepto at ₹8,000 crore, Business Today reports. Nearly 65 more companies await SEBI clearance to raise over ₹2 lakh crore, the same report shows. Add up just the three named deals, SBI Funds Management's upper estimate of ₹13,000 crore, Manipal Health Enterprises' ₹11,000 crore and Zepto's ₹8,000 crore, and they alone total ₹32,000 crore, about seven-tenths of that month's ₹45,000 crore, our calculation.

| Issuer | Sector | Planned IPO size |

|---|---|---|

| SBI Funds Management | Asset management | ₹12,000-13,000 crore |

| Manipal Health Enterprises | Hospitals | ₹11,000 crore |

| Zepto | Quick commerce | ₹8,000 crore |

Source: Business Today.

Three listings account for most of July's pipeline.

The rest of that month's roughly ₹45,000 crore pipeline is split across a much longer tail of smaller names.

Source: Business Today. Chart: The Signal.

Two of the biggest names are foreign parents cashing out

The pattern extends into the deals still being prepared for later this year. Coca-Cola is weighing an IPO of its Indian bottling arm, Hindustan Coca-Cola Beverages, that could raise around $1 billion, about ₹9,500 crore, and value the business at roughly $10 billion, Business Today reports, citing a Bloomberg report. Carlsberg has confidentially filed draft papers with SEBI for an IPO of its India unit that could raise as much as $700 million, with Kotak Mahindra Capital, JPMorgan and Citigroup as lead managers, Bloomberg News reported, as carried by Investing.com. Both are single-issuer, multinational-parent deals of a scale that would have stood out even in FY26's record year. Neither adds a second mid-sized company to the pipeline; each adds one more large one. The nearly 65 companies still awaiting SEBI clearance to raise over ₹2 lakh crore are the queue that could eventually widen the base again, but none of them have converted into a live listing yet.

The honest objection

The strongest case against reading any of this as concentration is that India's IPO market simply got bigger, and big markets produce big single deals. FY26's ₹1.9 trillion haul across a record 366 IPOs, up 9.5 percent on FY25, is real growth, not an illusion, and India held a 14 percent share of global IPO activity in March 2026, second only to China, a rank a market of scattered small listings could not sustain. On this view, SBI Funds Management, Manipal Health Enterprises, Zepto, Coca-Cola's bottler and Carlsberg's India unit are not a symptom of narrowing. They are what a maturing market looks like once it has room for issuers this size.

That case is real, but it does not explain why the shift away from broad participation was already visible before the quarter went quiet. Preferential allotments, the route negotiated with a small, chosen set of buyers, grew 76 percent in FY26 to ₹1.48 trillion while qualified institutional placements, the broader route, contracted 50 percent to ₹67,853 crore, inside the very year everyone points to as the boom. A market that is simply getting bigger should not need fewer, more negotiated buyers to do it. One that is quietly narrowing its base while the headline total climbs looks exactly like this.

The route open to more buyers shrank. The route negotiated with fewer grew.

Both routes sit inside the same record FY26; the shift happened while the total climbed, not after it slipped.

Source: SEBI April 2026 Monthly Bulletin. Chart: The Signal.

The Signal

FY26's record haul and July's ₹45,000 crore rebound are both real. So is the fact that three deals in July do most of the work, that Coca-Cola and Carlsberg are single foreign parents rather than a wider base of Indian issuers, and that the route open to the broadest set of buyers shrank by half in the very year the market called its best on record. The number that will say which story is true is not the pipeline's headline size. It is how many of the nearly 65 companies still waiting on SEBI clearance, worth over ₹2 lakh crore, actually list, and whether that queue shows up as dozens of mid-sized deals or as two or three more giants. If the queue converts broadly, this quarter was a pause. If it converts the way July already has, three names at a time, the market has changed shape and not just size.

Reporting basis: FY26's IPO count, mainboard totals and total fund mobilisation figures, the qualified-institutional-placement and preferential-allotment totals, and India's global IPO ranking are all per SEBI's April 2026 Monthly Bulletin, with the global ranking sourced from Bloomberg data as cited in that bulletin. The Q1 FY27 mainboard collapse and the full-year 2024 and 2025 comparison figures, July 2026's pipeline total, the SBI Funds Management, Manipal Health Enterprises and Zepto deal sizes, and the count of companies awaiting SEBI clearance are all per Business Today's reporting. Coca-Cola's bottling-arm IPO plans are per Business Today, citing a Bloomberg report; Carlsberg's confidential filing is per Bloomberg News, as carried by Investing.com. The combined share of July's pipeline held by the three named deals is The Signal's calculation from those figures.