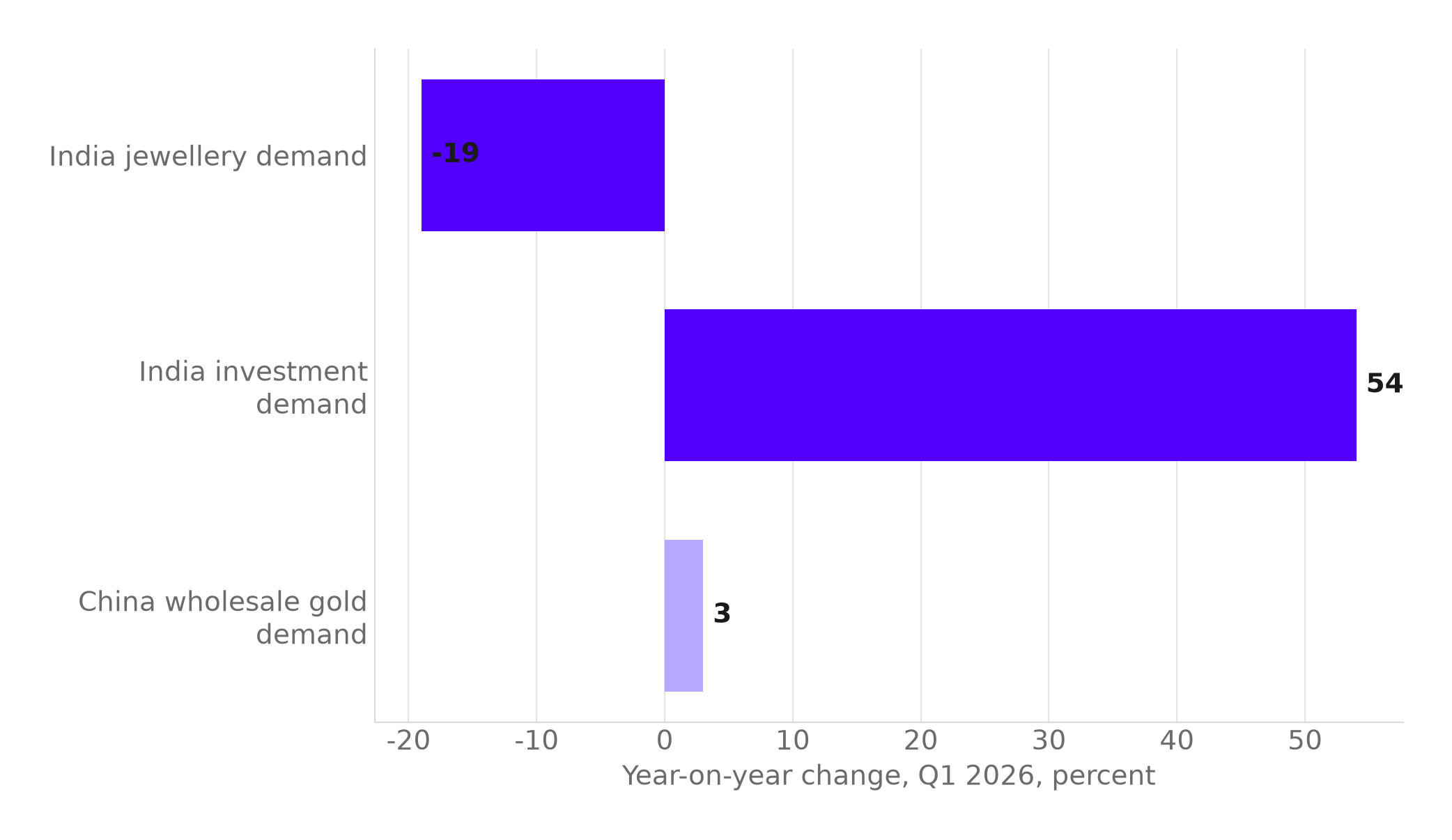

The easy read on India's gold market this year is that a record price is killing demand. It is not quite wrong. Jewellery volumes fell 19% year on year to 66 tonnes in the first quarter of 2026, the second-lowest first quarter on record since 2000, as the domestic price hit a record quarterly average of INR151,108 per 10 grams, up 81% year on year, World Gold Council data show. Every wedding-season headline about buyers walking past the counter has a real number behind it.

It is worth slowing down on that framing, because the same release shows total Indian gold demand did not fall at all. India's total gold demand actually rose 10% year on year to 151 tonnes in Q1 2026, driven by a 54% jump in investment demand to 82 tonnes, World Gold Council data show. Strip out the ornament counter and gold is not leaving India. It is moving to a different shelf.

India's jewellery demand fell 19% while its investment demand rose 54%, in the same quarter.

Bars in violet are India; the paler bar is China's comparable wholesale demand.

Source: World Gold Council, World Gold Council. Chart: The Signal.

The counter is shrinking just as the tax on it rises

That reframe is about to run into a second, unrelated shock. India's government raised the Basic Customs Duty on gold, silver and platinum from 5% to 10%, lifting the total effective import levy to 15%, with the new rates effective 13 May 2026, specifically to curb non-essential imports by discouraging discretionary gold demand through price signals, Business Today reports. The World Gold Council separately describes the same move as the steepest gold and silver import duty increase on record, from 6% to 15%, and projects it alone will cut India's 2026 jewellery, bar and coin demand by 50 to 60 tonnes, roughly 10% year on year, the World Gold Council reports.

That is a forecast, not a settled fact, but it is possible to put a rupee figure on what it would mean using only the numbers already on the page. At the Q1 2026 average domestic price of INR151,108 per 10 grams, the 50 to 60 tonnes of projected 2026 demand decline works out to roughly INR75,554 crore to INR90,665 crore of demand that would not materialise (our calculation, converting the World Gold Council's projected tonnage using its own Q1 average price). That range is illustrative, since the price will move through the rest of 2026, but it puts a scale on the duty hike: tens of thousands of crore of gold buying removed from a market already splitting between ornament and asset.

China's buyer never stopped, at any price

Across the border, the same global rally produced a very different response, because the buyer is different. The People's Bank of China bought 8 tonnes of gold in April 2026, its 18th consecutive monthly reserve addition and the largest single-month purchase since December 2024, World Gold Council data show. A central bank building a strategic reserve prices gold on entirely different terms than a household budgeting for a wedding. It buys on a schedule, not a discount.

That is not one good month; it is a year and a half of the same behaviour. The PBoC's reserves stood at 2,264 tonnes in November 2024, the month it ended a six-month hiatus and resumed buying with a 5-tonne addition, World Gold Council data show, the starting point of the streak that had reached 2,322 tonnes by April 2026 (our calculation, from two separate World Gold Council releases): 58 tonnes added over 18 consecutive months, through a rally, a price dip and everything in between.

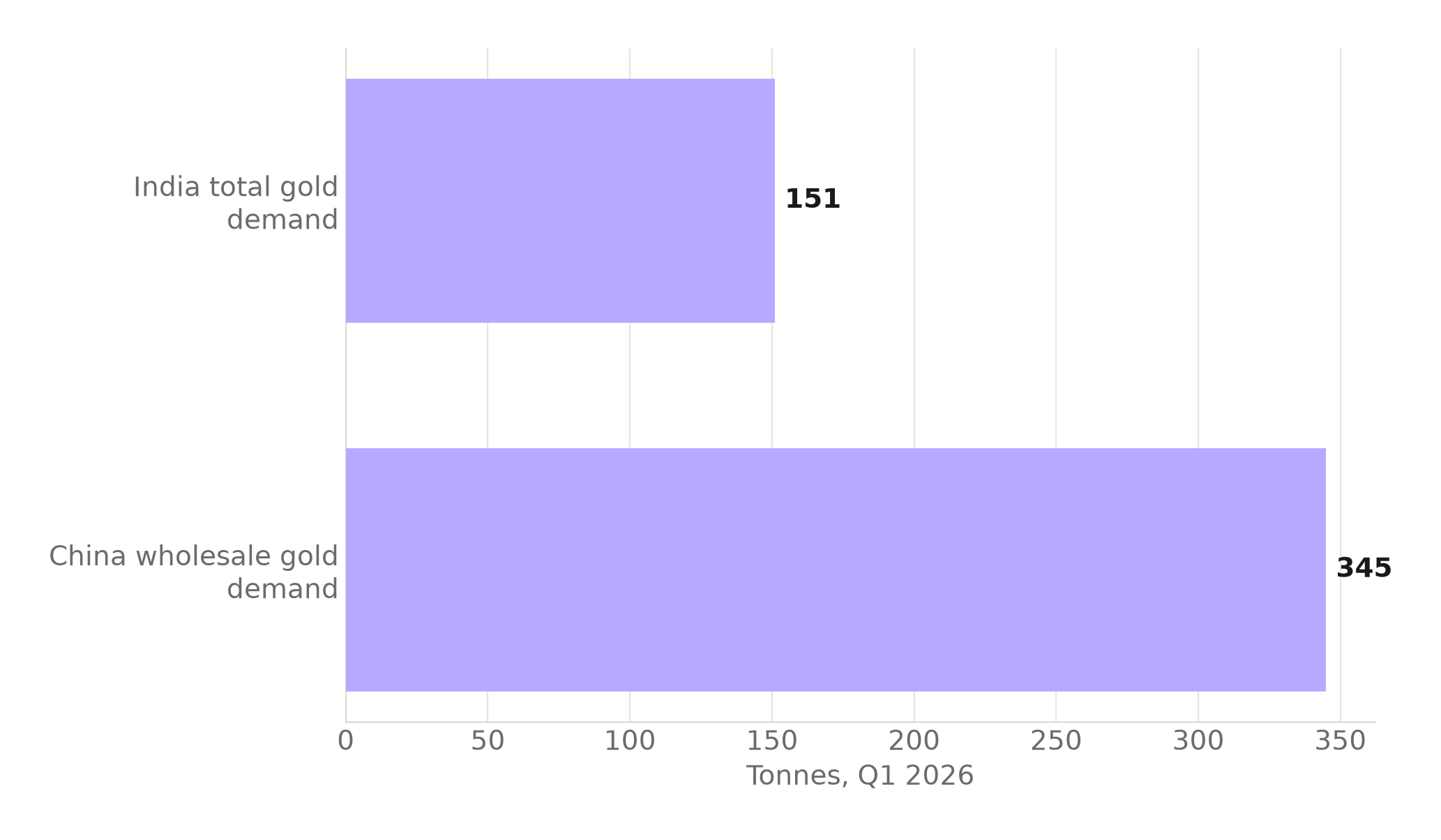

China's broader retail and industrial market shows the same pattern as India's, just less dramatic. China's Q1 2026 wholesale gold demand, measured by bank, jeweller and refiner withdrawals from the Shanghai Gold Exchange, rose to 345 tonnes, up 3% year on year, as strong investment demand offset persistent weakness in jewellery consumption, World Gold Council data show. Investment money is doing the same job in both countries: propping up a total that jewellery alone could not sustain. The difference is that China's wholesale volume that quarter, 345 tonnes, was more than double India's total, 151 tonnes, largely because a state institution kept buying regardless of price while India's market is still dominated by price-sensitive households.

China's Q1 2026 wholesale gold demand ran more than double India's total demand.

The two are not identical measures (India's is total demand; China's is wholesale exchange withdrawals), but both are the World Gold Council's own headline volume for the same quarter, and the gap is the point.

Source: World Gold Council, India Q1 2026; World Gold Council, China Q1 2026. Chart: The Signal.

Even the one month when global gold prices actually fell shows the split. Global gold prices fell 2.8% in April 2026, according to the World Bank's Pink Sheet commodity price data, dragging the broader precious metals index down 2.7% for the month, World Bank Pink Sheet data show. That was the same month the PBoC made its largest single purchase since December 2024. A cheaper month for gold did not slow China's central bank; it may have helped.

The deficit that a smaller gold bill did not fix

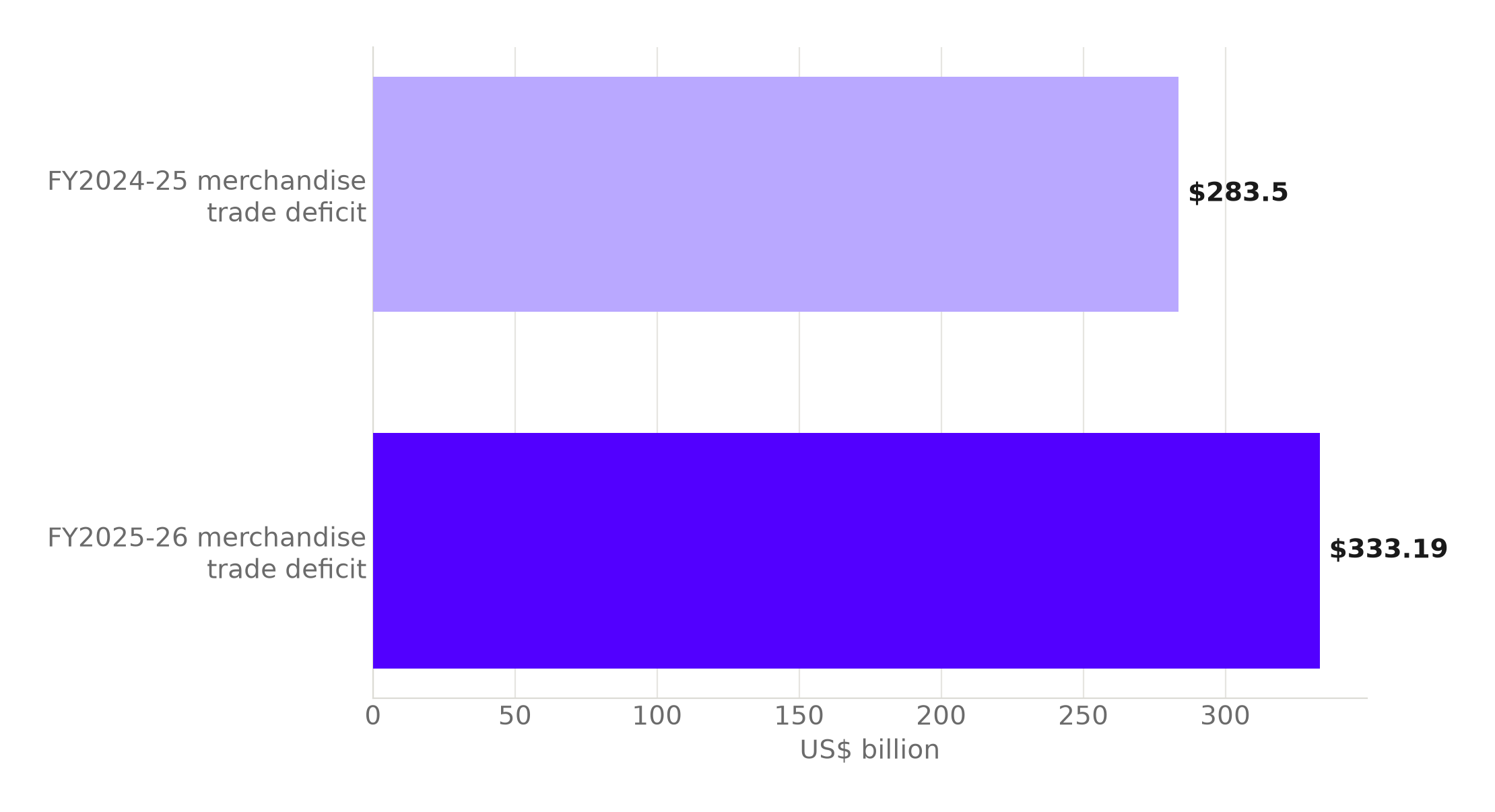

Here is where the divergence has a second-order cost for India specifically. India's gold imports fell 31.63% year on year in March 2026, even as the country's merchandise trade deficit widened to a record US$333.19 billion in FY2025-26 (April to March), from US$283.50 billion a year earlier, India's Ministry of Commerce and Industry reports. A smaller gold import bill is usually treated as automatic relief for the trade balance. It was not enough. The deficit set a record anyway.

It was not enough partly because the "smaller gold bill" framing does not survive the full year. The value of India's gold imports actually rose from US$58.01 billion in FY2024-25 to US$71.98 billion in FY2025-26, even as physical volumes fell, because the unit price of imported gold climbed from US$76,617.48 per kg to US$99,825.38 per kg, Doordarshan News reports, citing Ministry of Commerce and Industry data. March's volume plunge was real, but a smaller quantity of gold at a much higher price still cost the country more dollars for the year than the year before.

India's gold imports fell 32% in March 2026. The trade deficit still hit a record for the year.

| FY2024-25 | FY2025-26 | |

|---|---|---|

| Merchandise trade deficit | US$283.50 billion | US$333.19 billion |

| Gold imports, March, year on year | n/a | -31.63% |

Source: Ministry of Commerce and Industry, via PIB.

Source: Ministry of Commerce and Industry, via PIB. Chart: The Signal.

This piece does not claim to know which other import lines drove the wider deficit; the point is narrower. A falling gold import bill is not, on its own, a reliable lever for India's trade balance. India remains gold's second-largest market by volume, with average net demand of roughly 800 tonnes a year, the World Gold Council reports, so gold's import weight is real. But a 32% drop in one month's gold imports coincided with, rather than prevented, a record annual deficit.

The honest objection

The strongest case against reading any of this as a slowdown is that Indians are not buying less gold, they are buying it differently, and that is arguably the healthier trade. Investment demand up 54% while jewellery falls 19% looks like households treating gold as a hedge against a weak rupee and a volatile world, exactly the response gold is supposed to produce when policymakers elsewhere talk about de-dollarisation and reserve diversification. On that reading, China's central bank and India's investment buyers are doing the same thing for the same reason, just through different channels, and the jewellery decline is a shift in form, not a loss of appetite.

That case holds for the investment number alone. It strains once the duty hike is added, because a policy specifically designed to shrink the physical, discretionary end of the market, gold and silver import duty raised to what the World Gold Council calls the steepest increase on record, is not a household choosing to hedge. It is the state pushing the same direction the price already was. Two forces now point the same way on the same segment.

The Signal

Two of the world's largest gold markets are answering the same price rally on opposite terms. China's central bank bought gold on a fixed monthly cadence through April 2026, a month when global prices fell, the surest sign that price is not the variable driving that buyer. India's households are still price-sensitive, and the World Gold Council's own projection says the segment that responds to price, jewellery, bar and coin demand, is set to shrink by another 50 to 60 tonnes this year on the back of a fresh duty hike, worth on the order of INR75,000 to 90,000 crore of forgone demand at Q1 prices. Watch India's jewellery volumes through the rest of 2026: if they keep falling even as investment demand holds up, gold in India has permanently split into two markets with two different buyers, and only one of them cares what the price does next.

Reporting basis: India's Q1 2026 gold demand, its price data and the duty hike's projected demand impact are from two separate World Gold Council releases, its Gold Demand Trends India focus and its India market update on import tightening; China's Q1 2026 wholesale demand, the PBoC's April 2026 purchase and its November 2024 reserve level are from three further World Gold Council releases, its China market update on the seasonal demand rebound, its update on the rise in China's gold reserves, and its central bank gold statistics for November 2024; India's average annual net demand is from the World Gold Council's mid-year 2026 outlook. All six are counted as one origin, the World Gold Council, since each is that body's own primary data release rather than a secondary account of it. India's March 2026 gold import decline and the FY2025-26 merchandise trade deficit are from India's Ministry of Commerce and Industry, released via the Press Information Bureau; the FY2025-26 gold import value figures are from the same ministry's data, as reported by Doordarshan News. The April 2026 global gold price move is from the World Bank's Pink Sheet commodity data. The duty hike's mechanics, the Basic Customs Duty moving from 5% to 10% with a total effective levy of 15%, are as reported by Business Today, citing the Government of India's Ministry of Finance. The rupee range for the duty hike's projected demand impact and the 58-tonne cumulative gain in China's reserves over its buying streak are The Signal's own calculations, from the World Gold Council's tonnage projection and Q1 2026 average price, and from two of the World Gold Council's own reserve-level figures respectively.