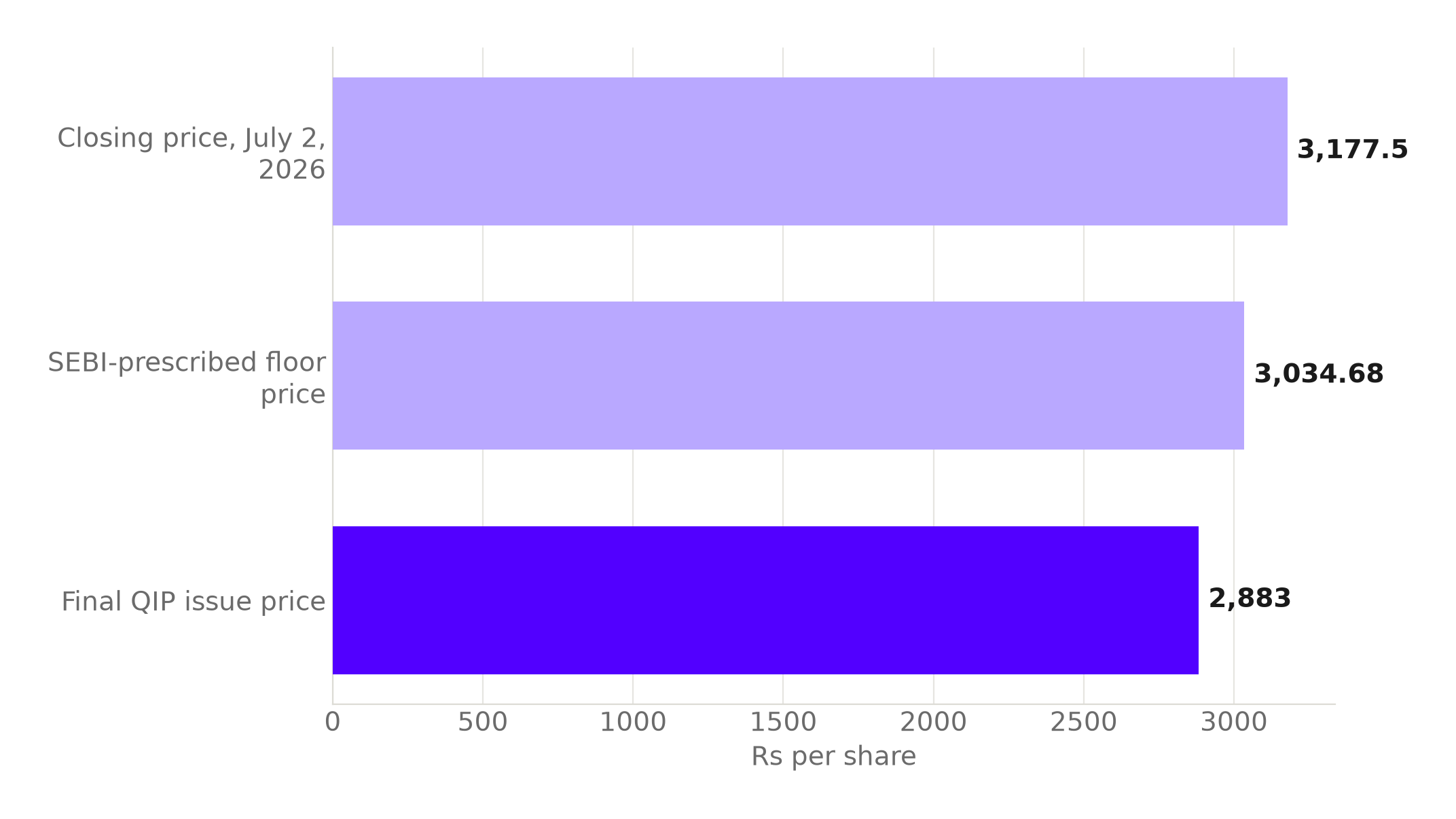

Adani Enterprises priced its qualified institutional placement at Rs 2,883 a share on July 2, 2026, a 9.27 percent discount to that day's closing price of Rs 3,177.50. The stock fell on the news. The instinctive read is the one every trading desk reaches for: a company had to cut its price by nearly a tenth to get a large placement done, so demand for a Rs 15,000 crore raise from one of India's biggest conglomerates must have been softer than the headlines suggested.

It is worth slowing down on that. The 9.27 percent figure is not a number Adani Enterprises' bankers set by reading the room. It is close to the largest discount SEBI's regulations permit a qualified institutional placement to carry, arrived at almost mechanically, before a single institutional bid came in.

The number that actually moved

SEBI's ICDR Regulations cap a qualified institutional placement's discount at 5 percent below a floor price, and that floor is not the day's market price. It is the average of the weekly high and low of the closing price over the two weeks before the deal is priced. Adani Enterprises' floor came out to Rs 3,034.68 a share, already about 4.5 percent below the July 2, 2026 close of Rs 3,177.50, simply because the stock had drifted higher over that fortnight. Subtract the full 5 percent SEBI ceiling from that floor and the price comes to Rs 2,882.95, matching the actual issue price of Rs 2,883 to the rupee.

Adani Enterprises priced its QIP at the maximum discount SEBI's formula allows, not a discount its bankers chose.

Stack a lagging two-week floor under a rising stock, then apply the full regulatory discount on top, and a headline gap in the high single digits against the day's close is close to automatic. It says nothing on its own about how badly the company needed to woo buyers.

Source: ScanX; Republic World. Chart: The Signal.

What demand actually looked like

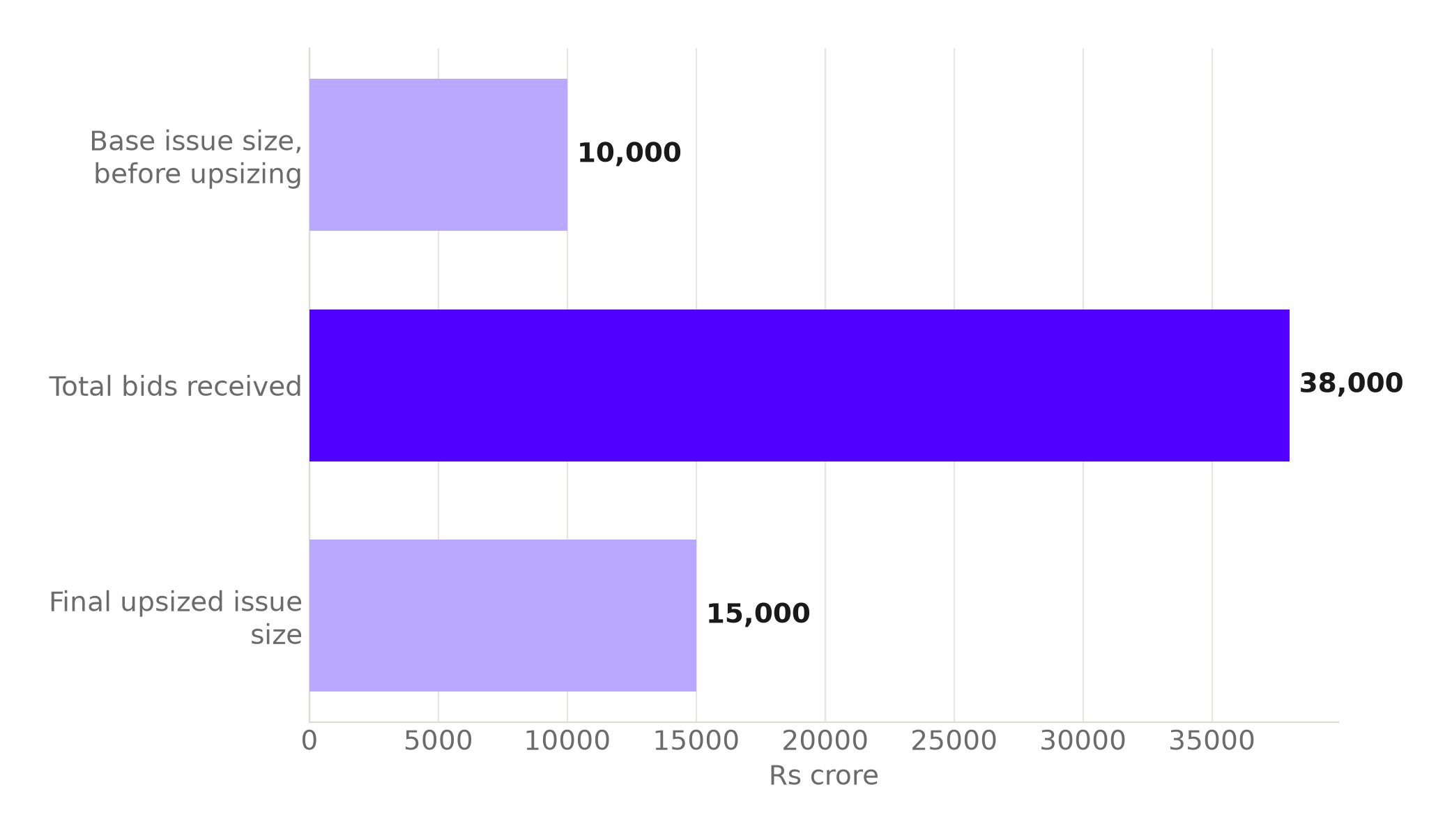

If the discount is not the demand signal, the order book is. Adani Enterprises set out to raise Rs 10,000 crore and drew bids worth about Rs 38,000 crore, 3.8 times that base size, and upsized the placement to Rs 15,000 crore in response. Even after that upsizing, the company left more than it raised on the table in unmet demand.

The order book ran 3.8 times the base issue size, and the company still turned away more money than it took.

Source: The Free Press Journal. Chart: The Signal.

The roster behind that demand was not a scramble of opportunistic funds. The anchor allocation drew Capital Group, Goldman Sachs, BlackRock, Blackstone and Nomura among global institutions, alongside HDFC, ICICI Prudential, Kotak, Aditya Birla Sun Life, SBI and Tata among domestic mutual funds:

| Investor type | Names in the anchor book |

|---|---|

| Global institutions | Capital Group, Goldman Sachs, BlackRock, Blackstone, Nomura |

| Domestic mutual funds | HDFC, ICICI Prudential, Kotak, Aditya Birla Sun Life, SBI, Tata |

Source: IANS.

That spread is also a function of design, not just appetite. SEBI's original QIP framework requires at least 10 percent of any placement to go to mutual funds and caps any single allottee at 50 percent of the issue, which is part of why a placement this size ends up broadly held rather than concentrated in one or two hands.

A small slice of the company, a large amount of capital

The Rs 15,000 crore raise diluted Adani Enterprises' outstanding equity by about 2.6 percent. That is the other half of what the discount framing obscures: existing shareholders gave up a small slice of the company for a large amount of fresh capital, at a price that, mechanical or not, still sat below where the stock was trading.

The raise is not standalone. It follows a Rs 24,930.30 crore rights issue Adani Enterprises completed in March 2026, part of a roughly Rs 36,000 crore FY26 capital expenditure plan spanning airports, roads, petrochemicals, metals and mining, and Adani New Industries. And the same week as the QIP, Adani Enterprises and Abu Dhabi's International Resources Holding signed a 50:50 joint venture worth about $11.5 billion, roughly Rs 1.08 lakh crore, to build an integrated aluminium project in Odisha. Two equity raises inside four months, alongside a joint venture more than four times their combined size, is the profile of a company financing an expansion, with no balance sheet in need of patching.

The honest objection

The strongest case for taking the discount seriously anyway is that "mechanical" does not mean "costless." SEBI's formula is mechanical by design precisely because it is meant to anchor pricing to where the stock has actually traded rather than to flatter the issuer. A floor that lags a rising stock, with the full legal discount stacked on top, still means new investors bought in below the day's price, funded economically by the shareholders excluded from the placement. The fact that the ceiling was hit by formula rather than by negotiation does not erase that transfer, and a promoter-controlled company at the legal maximum on a placement this size is a fair thing for existing shareholders to note, whatever set the number.

That case is real, but it explains a cost. It says nothing about demand. SEBI's 5 percent statutory ceiling applies whether an issue is undersubscribed or oversubscribed several times over. What actually varies with demand is whether a company can upsize at all, and Adani Enterprises upsized by half against an order book nearly four times its original target.

The Signal

The 9.27 percent discount and the 3.8 times oversubscription happened on the same deal because they answer different questions. The discount tells you what SEBI's floor formula and its 5 percent ceiling produced when applied to a rising stock. Capital Group, BlackRock, Goldman Sachs and India's largest mutual funds were the ones actually willing to pay for a 2.6 percent slice of Adani Enterprises, and that willingness is what the order book measures. Any large-cap issuer weighing a similar raise this year should read the second number, not the first: the discount headline will look similar almost automatically. The subscription ratio is where the real judgment on appetite for Indian secondary capital lives. A ceiling set by formula is not a verdict on demand.

Reporting basis: the QIP issue price and its discount to the July 2, 2026 close are per Republic World's report of Adani Enterprises' exchange disclosure. The floor price is per ScanX's report of the same disclosure. Both figures trace to SEBI's Issue of Capital and Disclosure Requirements Regulations, 2018 and SEBI's original Qualified Institutions Placement guidelines, the regulations governing QIP pricing and allotment. The base issue size, total bids and oversubscription ratio are per The Free Press Journal's report of the exchange disclosure. The anchor investor roster is per IANS's report of the same. The dilution percentage is per Business Today's report. The March 2026 rights issue and FY26 capex plan are per Outlook Business's report of Adani Enterprises' corporate disclosures. The Odisha joint venture is per The Tribune's report of the companies' joint statement. The implied maximum-discount price and the description of the order book as 3.8 times the base issue are The Signal's calculations from those figures.