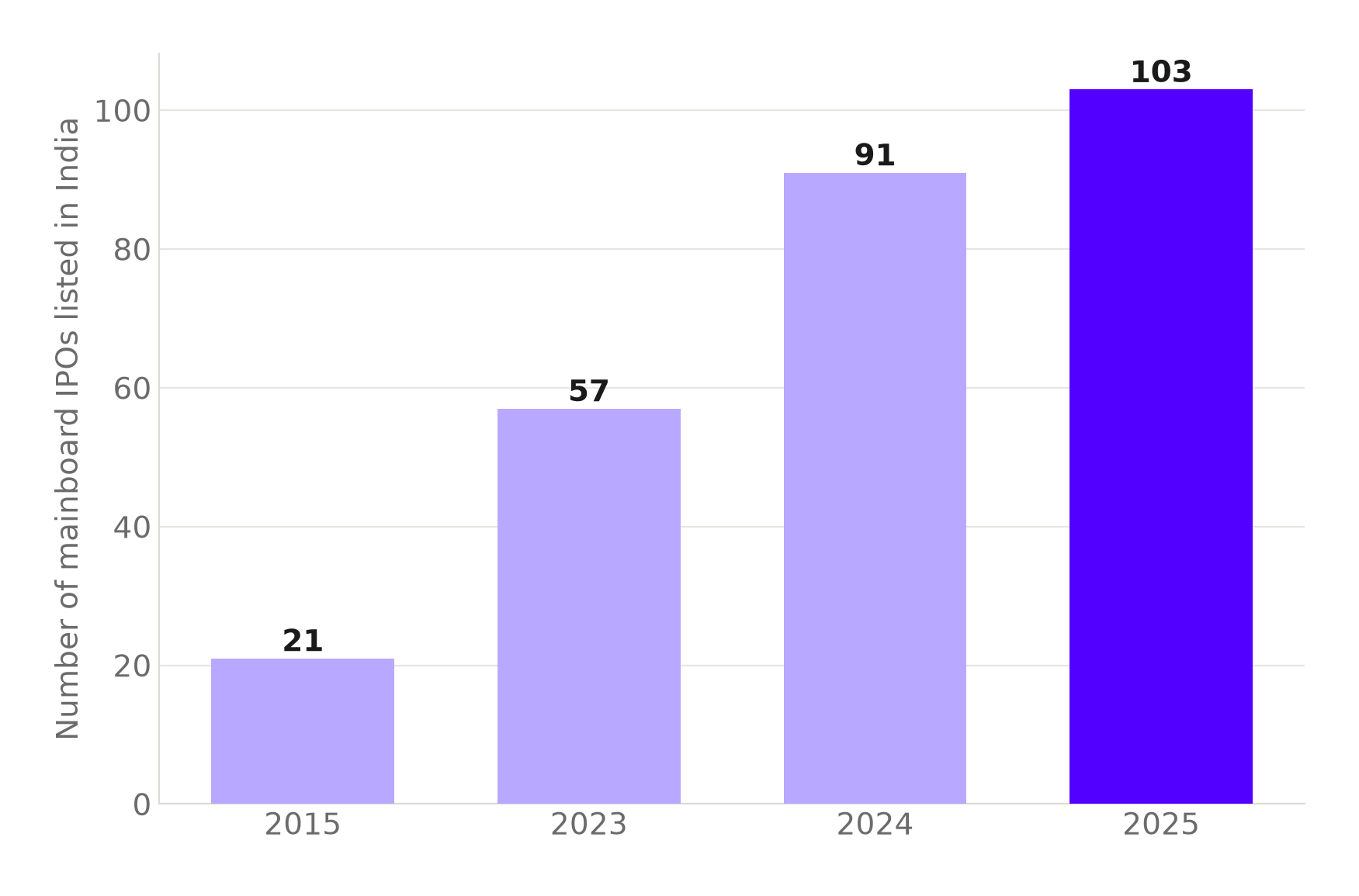

Four large India listings are in motion at once. Carlsberg A/S has confidentially filed draft papers to raise as much as $700 million by selling shares in its India unit. Coca-Cola has lined up Kotak, HDFC Group and Citibank for a roughly $1 billion IPO of Hindustan Coca-Cola Beverages, its India bottling arm. Parle Products, maker of Parle-G, is working toward a listing that could value the company above $10.5 billion. And Girnar Insurance Brokers, which runs InsuranceDekho, is weighing an IPO that could raise up to $250 million after its merger with RenewBuy. The easy read is that India's IPO market has never been hotter, and the numbers back that up: mainboard IPOs raised a record Rs 1.75 lakh crore in 2025 across 103 listings, up from just Rs 13,614 crore across 21 listings in 2015: a nearly 13-fold jump in money raised and a five-fold jump in deal count.

Nearly five times as many mainboard IPOs list in India now than in 2015.

Deal count has climbed every year data is available, and SEBI's approved 2026 pipeline points to another leg higher still.

Source: The Economic Times, citing Prime Database. Chart: The Signal.

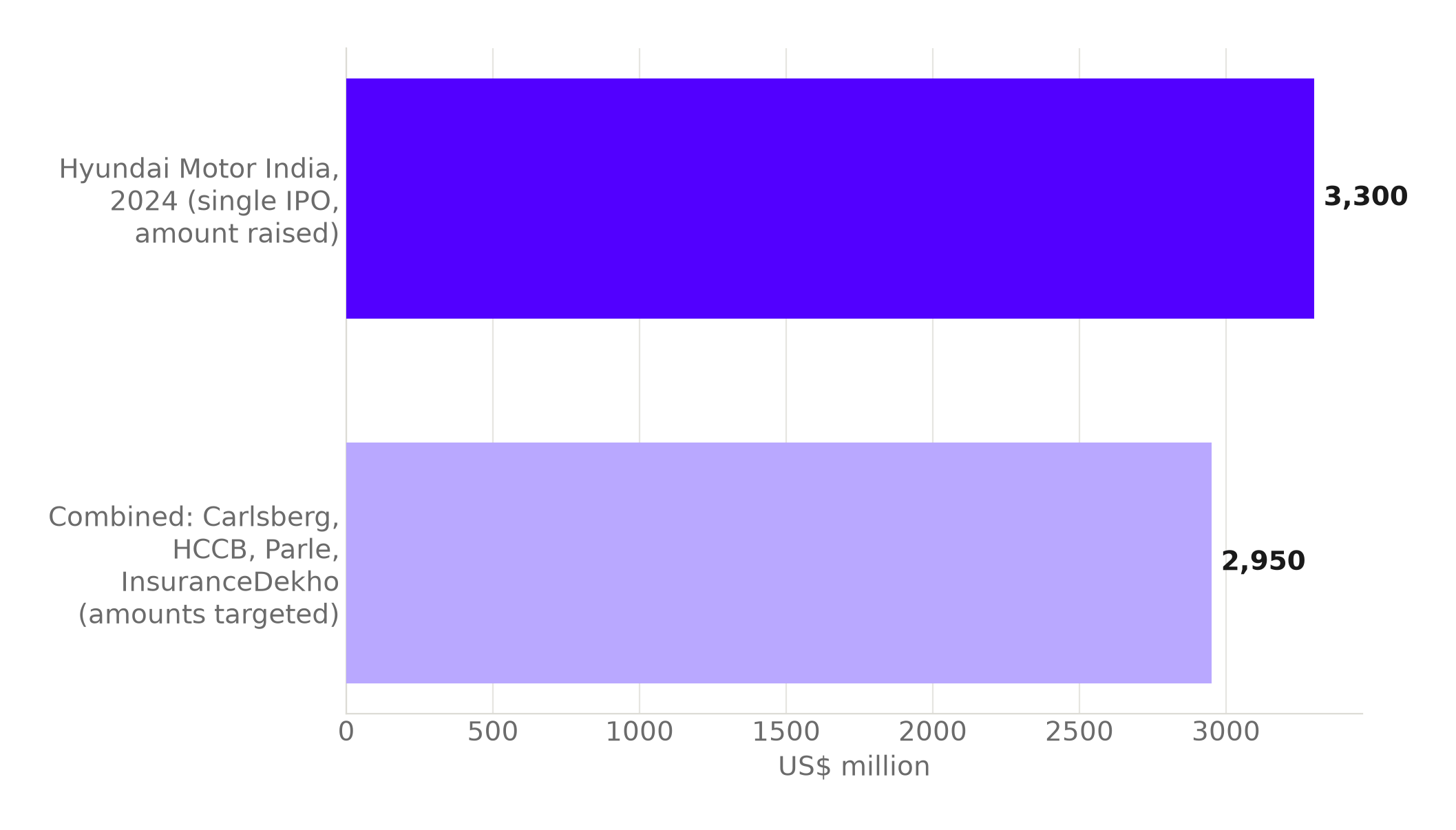

It is worth slowing down on that framing. Two of these four names, Carlsberg and Coca-Cola, are genuinely foreign multinationals monetising a slice of an India subsidiary. Parle and Girnar are Indian-owned companies simply riding the same open market. And even added together, the four are not especially large by India's own recent standard: Carlsberg's $700 million, Coca-Cola's roughly $1 billion, Parle's stated raise of over $1 billion and Girnar's up to $250 million sum to about $2.95 billion. Hyundai Motor India's single 2024 listing raised Rs 27,870 crore, about $3.3 billion, on its own: more than all four of 2026's marquee filings combined.

Hyundai's single 2024 IPO still outraises this year's four combined.

Hyundai's India IPO alone exceeds the combined target of Carlsberg, Coca-Cola's bottler, Parle and InsuranceDekho.

Source: The Hindu; Moneycontrol; The Economic Times. Combined figure is The Signal's calculation. Chart: The Signal.

So this is not a record-breaking wave by size. What it is, for Carlsberg and Coca-Cola specifically, is a bet on a gap that has held for years and shows no sign of closing.

The premium already sitting on the board

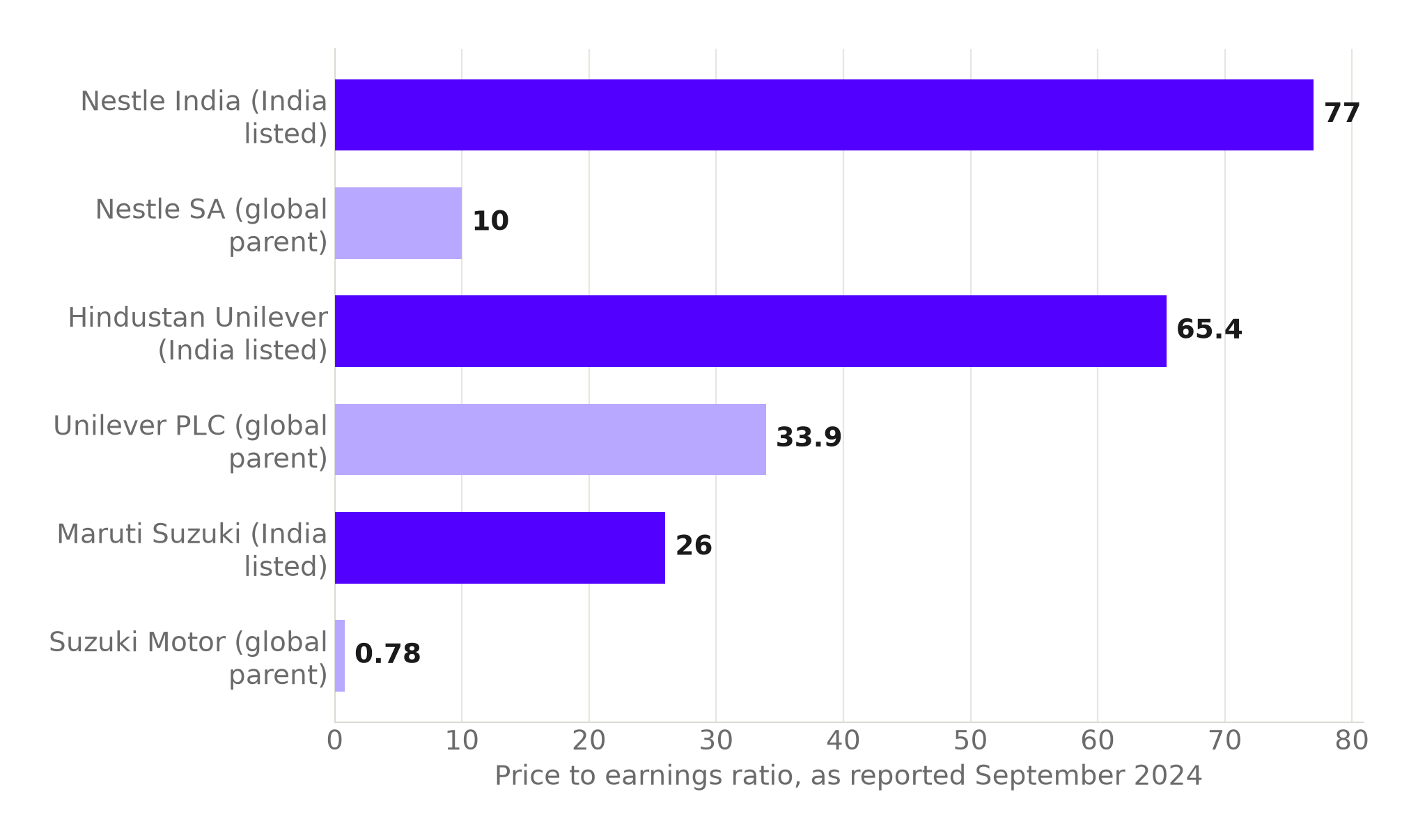

India already runs a live experiment in what a subsidiary is worth once it trades on its own exchange, separate from its global parent's stock price. In The Economic Times' September 2024 comparison, Hindustan Unilever traded at a price-to-earnings ratio of 65.4, against parent Unilever PLC's 33.9: nearly double. Nestle India traded at a PE of 77, against Nestle SA's 10: close to eight times over. Maruti Suzuki's India-listed PE of more than 26 against parent Suzuki Motor's 0.78 in the same September 2024 snapshot is a more extreme reading, because Suzuki's own multiple was unusually depressed in that period. But the direction is identical three times running: the India-listed twin prices richer than the global parent.

Every India-listed subsidiary in the sample trades above its global parent.

The gap ran from roughly double to nearly eightfold across three long-listed names, and it predates the current filing wave by years. Violet bars are the India-listed subsidiaries; lavender bars are their global parents.

Source: The Economic Times, September 2024. Chart: The Signal.

That is the arithmetic Carlsberg and Coca-Cola are filing against. Their India units already generate real earnings; the question a bank asks before an IPO is simple: would this business be worth more inside the parent's stock, or listed in Mumbai and priced against Hindustan Unilever and Nestle India's multiples instead of Unilever's and Nestle SA's. For a beer maker and a bottler with decades of India distribution built in, the answer has increasingly been to test the Indian market's price directly rather than leave it embedded in a global multiple.

Parle and InsuranceDekho are a different trade

Parle Products and Girnar Insurance Brokers are not foreign parents cashing out an India arm; they are homegrown companies choosing to list into an unusually open window. That window is wide for reasons that have nothing to do with valuation arbitrage. SEBI has already approved 96 IPOs worth around Rs 1.25 lakh crore waiting to launch, with another 106 companies seeking about Rs 1.40 lakh crore still in the approval queue: a queue of more than 200 companies. India's primary markets, equity and debt combined, had already mobilised Rs 10.7 lakh crore in FY26 through December 2025, and Rs 53 lakh crore over the five years to FY26, against an economy with nominal GDP estimated at Rs 357.14 lakh crore for FY26. Against a pipeline and a market that size, Parle and Girnar are two more names filing into a favourable calendar, not evidence of the same subsidiary-arbitrage logic driving Carlsberg and Coca-Cola.

The honest objection

The strongest case against calling this an arbitrage is that Indian equities may simply deserve a persistent premium: faster nominal earnings growth, a much larger pool of domestic retail and mutual-fund buyers than global staples stocks get, and benchmark-weight fund flows that keep demand for large India-listed names structurally higher than for their parents. On that view, Hindustan Unilever and Nestle India are not mispriced, they are correctly priced for a market with better growth and thinner float, and Carlsberg and Coca-Cola are simply following sound corporate finance by listing where the multiple is genuinely higher.

That case is real, but it strains once the gap runs to eight times, as it did for Nestle in September 2024. A faster-growing market can justify a richer multiple; it cannot easily justify one an order of magnitude apart, sustained across three unrelated sectors, for years, without ever converging. A persistent, multi-sector, multi-year gap that size looks less like a growth premium and more like a structural one: too few India-listed shares chasing too much domestic demand, with any new float from a subsidiary IPO absorbed into that same scarcity rather than closing it.

The Signal

The 2026 filings are not a story about IPO volume; India has seen bigger years and bigger single deals. They are a live test of whether the India premium is a price or a mirage. If Carlsberg and Coca-Cola's bottler list at multiples closer to Hindustan Unilever's than to their own parents', the arbitrage read holds, and every multinational with an unlisted India arm has just been handed its corporate-finance homework. If the queue of more than 200 approved and pending IPOs dilutes the scarcity that inflated the premium first, the gap these two are counting on may not survive their own listings. Either way, the number to watch is not the size of the raise. It is the multiple on day one.

Reporting basis: the Carlsberg, Hindustan Coca-Cola and Parle filing details are per Moneycontrol's reporting on the confidential filings; the InsuranceDekho plan is per The Economic Times. IPO counts and totals for 2015 through 2025 are Prime Database figures, as reported by The Economic Times, and the 2026 approved-and-pending pipeline is per The Economic Times' report of SEBI approvals. The September 2024 price-to-earnings comparison of India-listed subsidiaries and their parents comes from a single Economic Times analysis and is the only source for those multiples. Primary-market mobilisation is from the Economic Survey 2025-26 and nominal GDP from MoSPI's First Advance Estimates, both via Press Information Bureau releases. Hyundai Motor India's 2024 raise is as reported by The Hindu. The combined totals and the parent-to-subsidiary multiples are The Signal's calculations from those figures.