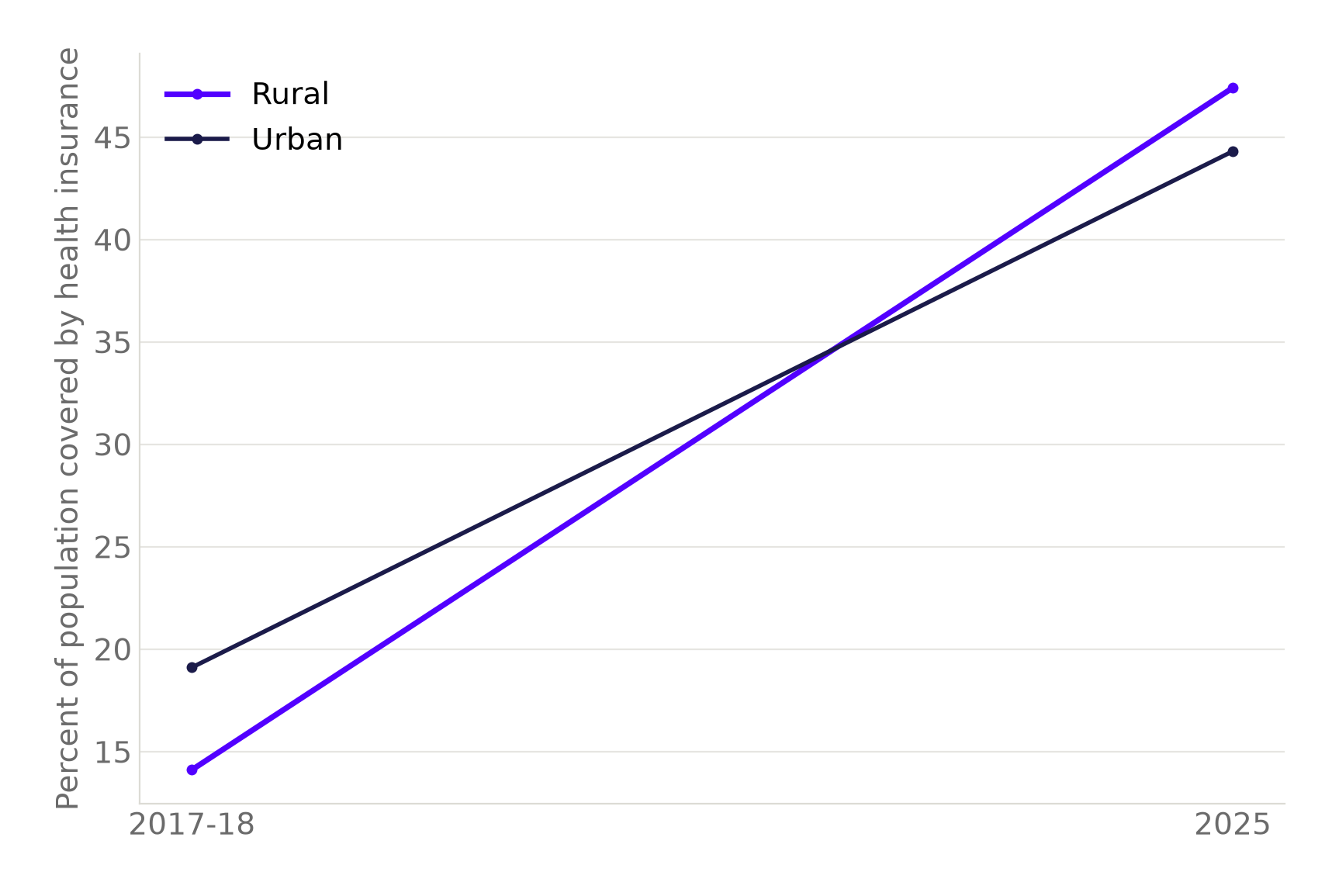

India's latest health survey delivers a clean headline. Rural health insurance coverage rose to 47.4% in 2025 from just 14.1% in 2017-18, while urban coverage rose to 44.3% from 19.1% over the same period, a Press Information Bureau note on the NSS 80th round survey reports. The two lines have crossed. For the first time on record, a larger share of rural India carries health insurance than urban India. Read only the top line and it looks like an unambiguous, uncomplicated win for a country that has spent close to a decade pushing subsidized health cover into the countryside.

Rural health insurance coverage has overtaken urban coverage for the first time on record.

Both lines climbed for eight straight years, but rural coverage climbed further and faster, closing a five-point gap and opening a three-point lead of its own.

Source: Press Information Bureau, citing the NSS 80th round survey. Chart: The Signal.

It is worth slowing down on that crossover. Government-sponsored scheme coverage in rural India rose from 12.9% in 2017-18 to 45.5% in 2025, more than tripling, while urban government-scheme coverage rose from 8.9% to 31.8% over the same period, the National Statistics Office's NSS Report no. 596 shows. Rural coverage overall reached 47.4%. Government schemes alone account for 45.5 of those 47.4 percentage points.

Almost all of rural India's coverage gain rode in through a government scheme, not a commercial policy.

| Segment | 2017-18 | 2025 |

|---|---|---|

| Rural, government-scheme coverage | 12.9% | 45.5% |

| Urban, government-scheme coverage | 8.9% | 31.8% |

Source: National Statistics Office, NSS 80th Round Report no. 596. Table: The Signal.

Strip the scheme numbers out of rural India's insurance story and there is barely a story left. The coverage crossover is real. What crossed over is mostly subsidized cover, not a wave of households choosing to buy commercial health insurance on their own.

What insurers are actually being handed

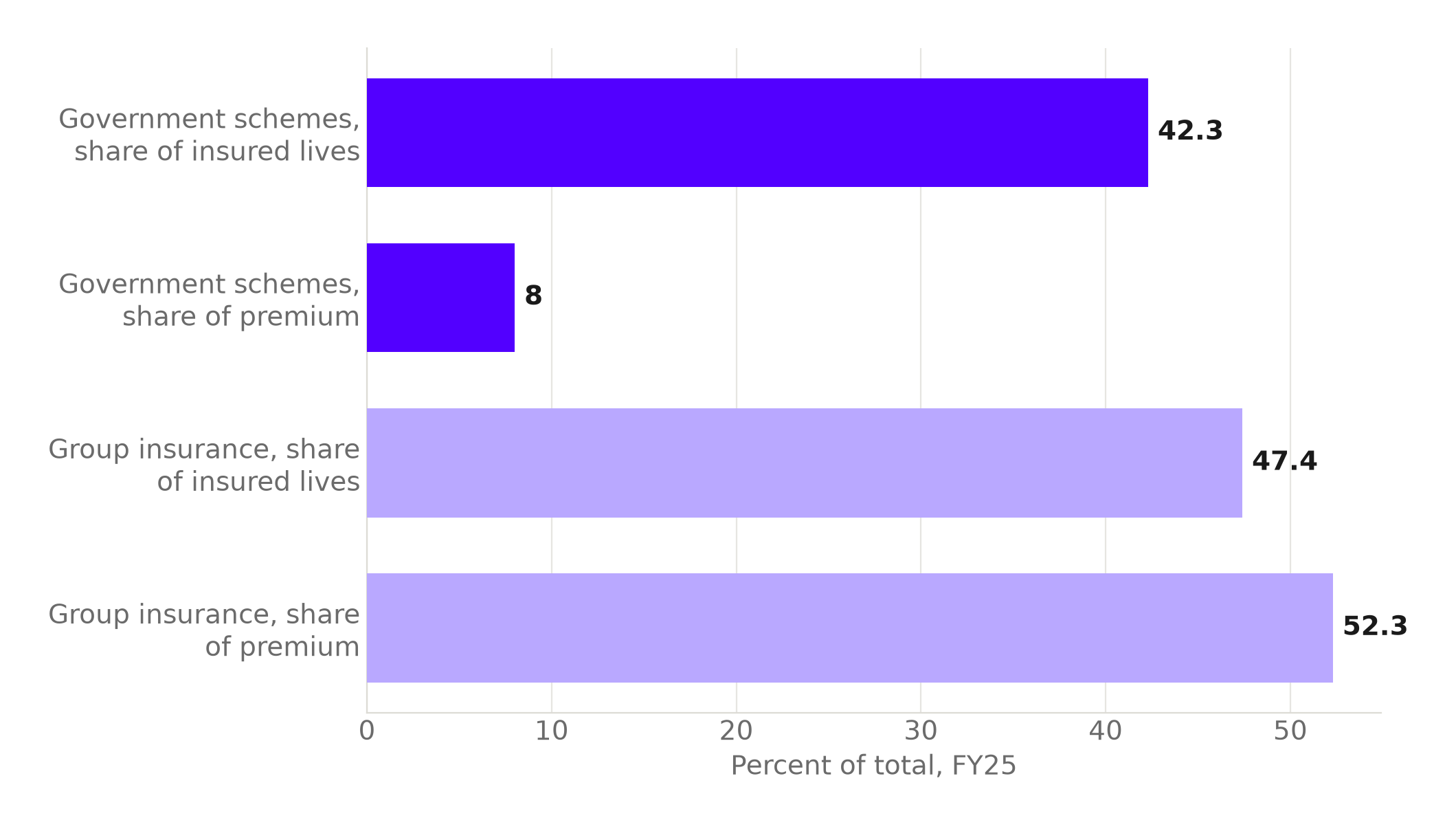

Government-sponsored schemes cover 42.3% of all insured lives in India but generate just 8.0% of total health-insurance premium, while group insurance covers 47.4% of lives and brings in 52.3% of premium, IRDAI's Annual Report 2024-25 shows. Group insurance earns roughly its proportional share of the premium pool it holds in lives. Government schemes, with a nearly identical share of lives, earn about a fifth of theirs. The rural surge is a lives story. On the money side, it barely registers.

Violet bars are the government-scheme book; lavender bars are the group-insurance book it is being compared against.

Source: IRDAI Annual Report 2024-25. Chart: The Signal.

India's total insurance penetration, premiums measured against GDP, held flat at 3.7% in FY25, roughly half the global average of 7.3%, the Swiss Re Sigma World Insurance Report, as cited in IRDAI's Annual Report 2024-25, shows. The rural scheme wave has not moved that number. It has added tens of millions of policyholders without adding a proportional rupee of premium, which is exactly what a subsidized public scheme is designed to do. That is precisely why it does not, on its own, solve insurers' scale problem.

Tier-3 India is buying a different product

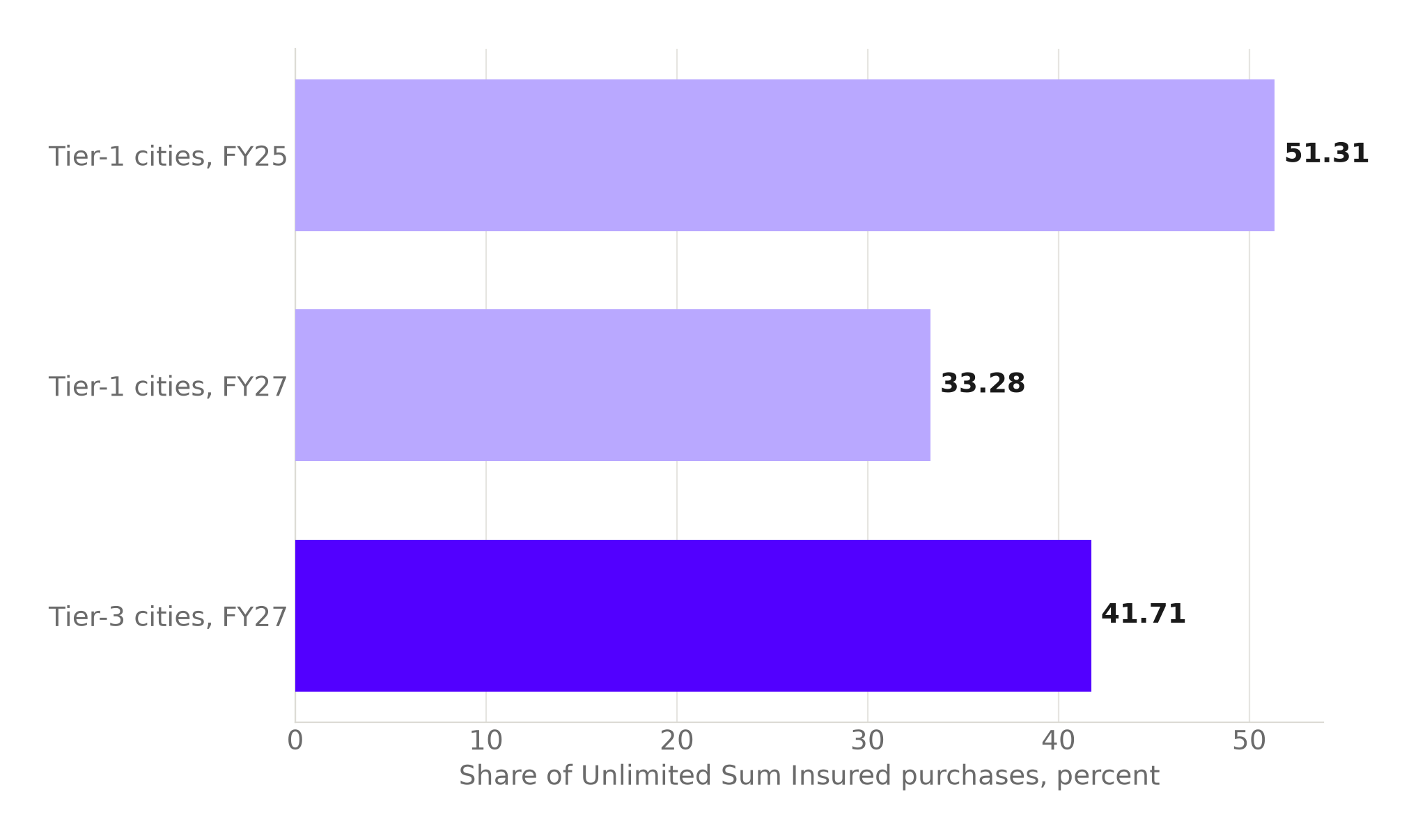

Tier-3 cities' share of Unlimited Sum Insured health-insurance purchases rose to 41.71% in FY27, overtaking Tier-1 cities, whose share fell to 33.28% in FY27 from 51.31% in FY25, Policybazaar data, as reported by Business Today, show. Surat posted the steepest premium ticket-size growth of any Indian city, up 45%, followed by Hyderabad at 43%. This is not the rural scheme story wearing a different label. Unlimited Sum Insured is a full commercial product that a buyer chooses and pays a real premium for, and its growth has shifted to cities one rung below the metros, not to villages.

Tier-3 cities now buy a bigger share of India's highest-end commercial health cover than Tier-1 metros do.

Source: Policybazaar data, via Business Today. Chart: The Signal.

Put the two trends side by side and India's health-insurance market is splitting into two distinct books at once. Rural India is gaining coverage mostly through subsidy. Non-metro urban India, cities like Surat and Hyderabad, is buying the same full-price commercial products metros already buy. Only one of those two books currently pays insurers what a group or individual commercial policy does.

The honest objection

The strongest case against reading this as a margin problem is that scale and access are the point, not a distraction from it. Average out-of-pocket medical expenditure per hospitalization in 2025 was actually lower in rural India, at Rs 31,484, than in urban India's Rs 38,688, against a national average of Rs 34,064, the NSS Report no. 596 shows, even though rural households have lower average incomes to draw on. Institutional deliveries in rural India rose to 95.6% in 2025 from 90.5% in 2017-18, while urban institutional deliveries rose to 97.8% from 96.1% over the same period: a basic access gap is closing alongside the insurance numbers. On this reading, subsidized scheme coverage is doing precisely the job a public program is built for, protecting families from catastrophic cost, and today's low premium is simply the price of building a policyholder base insurers can sell more to later, as rural incomes rise.

That case is real, and the access numbers back it. But it describes a bet on the future, not a return today. India's total insurance penetration has held flat at 3.7% of GDP, a number that would move if the rural scheme wave were converting into commercial premium at any meaningful pace. It has not, at least not yet. A regulated insurance industry cannot fund claims, reserves and capital on a promise that today's low-margin lives eventually upgrade. It prices the book it holds now, and the book it holds now is heavily weighted toward the segment that pays it least.

The Signal

The rural crossover is the number an eight-year subsidized-insurance push was always going to produce eventually, and it deserves to be read as real progress on access. But the more consequential number sits one document over: 42.3% of the lives insurers now cover bring in 8.0% of their premium. Watch two things next. Whether Tier-3 cities like Surat and Hyderabad keep outpacing the metros in commercial purchases, because that book pays insurers what the rural scheme book does not. And whether India's stalled 3.7% penetration ratio finally moves, because until it does, rural India's new insurance card is a coverage statistic before it is a business one.

Reporting basis: the rural and urban health-insurance coverage figures, the government-scheme coverage breakdown, the out-of-pocket hospitalization figures and the institutional-delivery figures all originate with the Ministry of Statistics and Programme Implementation's NSS 80th Round document no. 596, with the headline coverage crossover also carried in a Press Information Bureau note drawing on the same round. The insured-lives and premium-share breakdown by government scheme and group business, and India's insurance-penetration ratio against the global average, both originate with IRDAI's 2024-25 annual filing, with the penetration figure itself credited there to Swiss Re Sigma. The Tier-1 and Tier-3 city figures are Policybazaar's own numbers, carried via Business Today, a single secondary source for those city-level figures. The proportional comparison between government schemes' share of lives and share of premium is The Signal's calculation from the IRDAI figures.