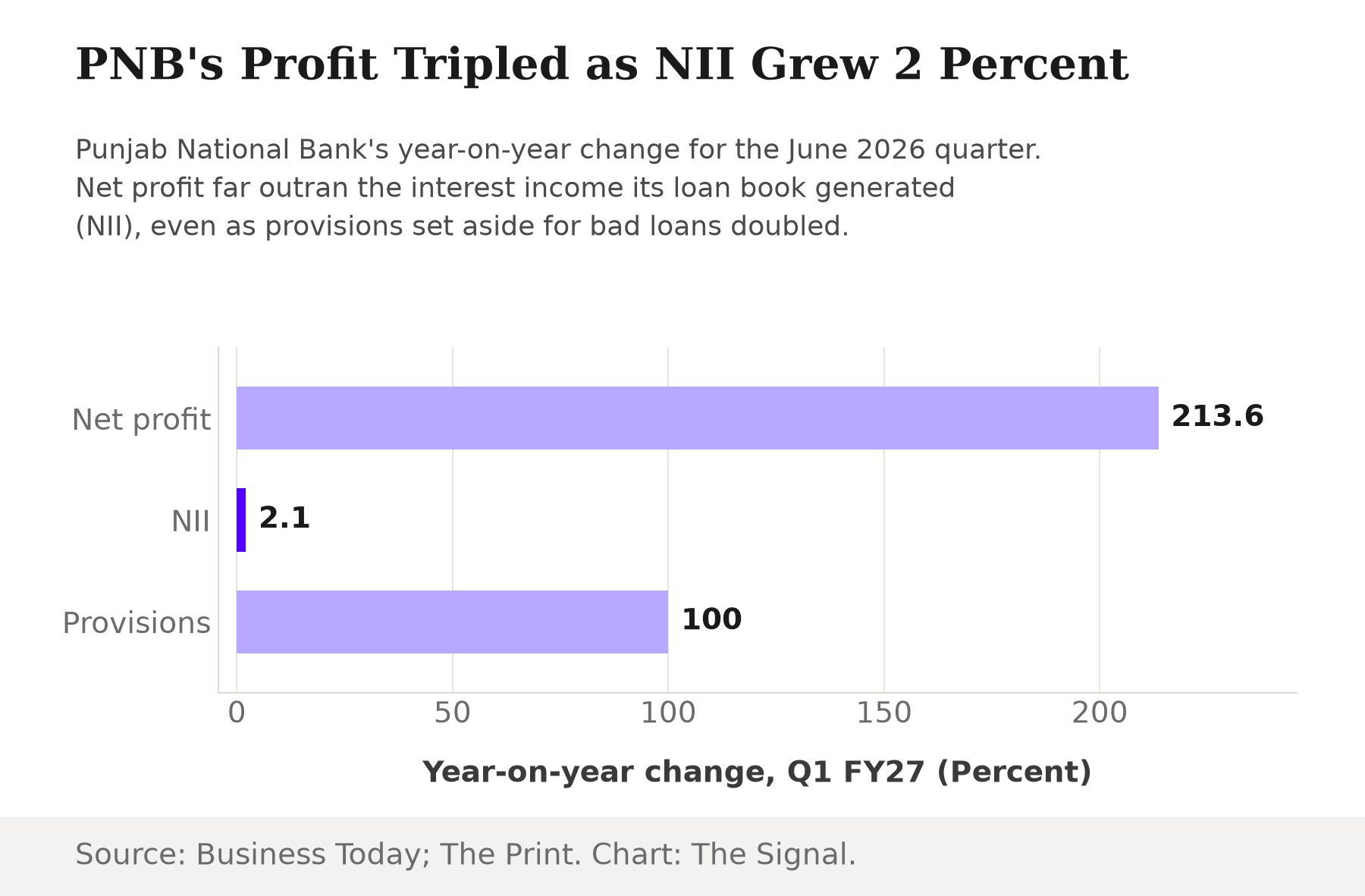

Punjab National Bank reported its June quarter results this week, and the headline number is the kind that leads an earnings season: net profit up 213.6 percent year-on-year to Rs 5,253 crore, against Rs 1,675 crore a year earlier. Read only that line and the story writes itself: a public-sector lender that spent a decade working through bad loans is now printing money.

It is worth slowing down on that. PNB's net interest income, the core lending income a bank earns from the spread between what it charges borrowers and what it pays depositors, rose just 2.1 percent to Rs 10,798 crore in the same quarter. A bank's lending business is supposed to be the engine of its profit. Here the engine barely turned over while the profit line tripled.

The obvious next guess, a common one when a bank's headline profit outruns its lending income, is that the bank simply set aside less money to cover bad loans this time. PNB did the opposite. Provisions for bad loans rose to Rs 792 crore in the June quarter, from Rs 396 crore a year earlier, a doubling. The profit tripled while both of the numbers that would normally explain a profit swing, the lending income and the provisioning, moved against it.

Source: Business Today (profit, net interest income); The Print (provisions). Chart: The Signal.

The same gap, in five more results this week

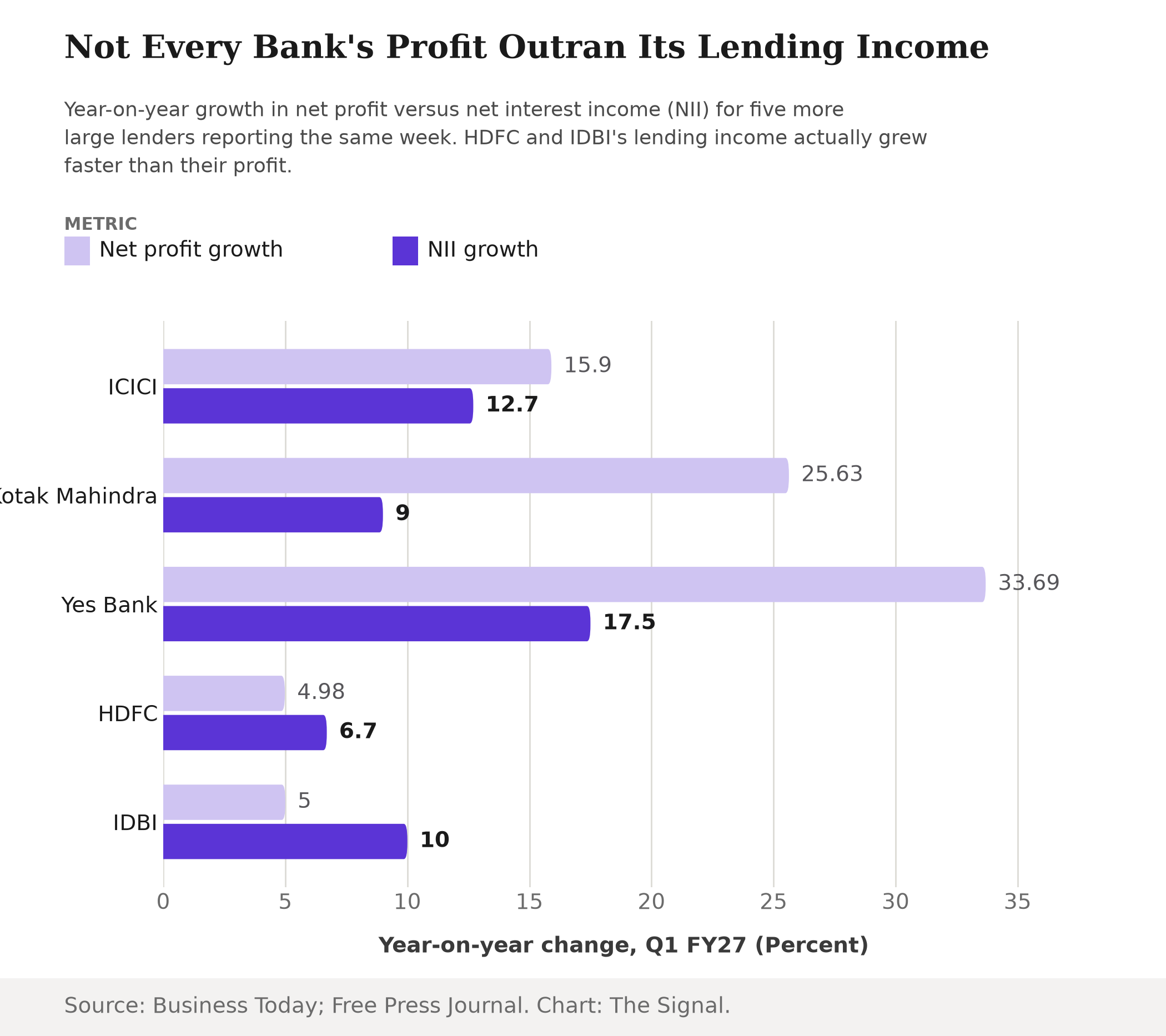

PNB was not filing alone. Five other large Indian lenders reported June quarter results in the same window, and the profit-to-lending gap shows up to very different degrees across them.

Every one of the six banks reporting this week posted profit growth, but only three show profit meaningfully outrunning lending income.

| Bank | Net profit growth (YoY) | NII growth (YoY) |

|---|---|---|

| Punjab National Bank | +213.6% | +2.1% |

| Yes Bank | +33.69% | +17.5% |

| Kotak Mahindra Bank | +25.63% | +9% |

| ICICI Bank | +15.9% | +12.7% |

| HDFC Bank | +4.98% | +6.7% |

| IDBI Bank | +5% | +10% |

Source: Business Today; Free Press Journal; The Print. Figures are standalone, year-on-year, for the quarter ended June 2026.

Source: Business Today (ICICI, Kotak Mahindra, Yes Bank, IDBI); Free Press Journal (HDFC). Chart: The Signal.

HDFC Bank and IDBI Bank actually show the pattern reversed: HDFC's net interest income grew 6.7 percent against 4.98 percent profit growth, and IDBI's grew 10 percent against 5 percent profit growth. That matters, because it means this is not a uniform, sector-wide story where every large bank is quietly manufacturing profit growth its loan book cannot support. It is a story with a genuine outlier in PNB, a moderate version of the same gap at Kotak and Yes Bank, and two banks, ICICI and HDFC, where profit and lending income moved in something close to lockstep.

One bank explains its gap. PNB does not

Kotak Mahindra Bank's results come with a stated mechanism for its own version of the gap. The bank said its profit gain was aided by provisions falling 45 percent year-on-year to Rs 668 crore, even as those provisions rose from the March quarter. Lower provisioning is a normal, checkable reason for profit to outrun lending income: set aside less for bad loans this quarter than last year, and more of the lending income drops straight to the bottom line.

That channel does not work for PNB. Its provisions did not fall, they doubled, to Rs 792 crore from Rs 396 crore. The line that does move in PNB's favour is tax, not lending or provisioning. PNB's income-tax provision fell 66.1 percent year-on-year to Rs 1,725 crore, from Rs 5,083 crore a year earlier, a swing of roughly Rs 3,360 crore that alone accounts for most of the Rs 3,600 crore rise in net profit. That is not this quarter's tax rate falling; it is last year's comparison being unusually high. PNB's tax charge in the year-ago quarter had more than doubled to Rs 5,083 crore because the bank switched to the new income-tax regime that quarter, a one-time-elevated base, and management said the switch would save the bank roughly Rs 700 crore a quarter going forward. So PNB's "tripled profit" is largely a base-effect story: a lending business that grew income 2.1 percent, measured against a year-ago quarter whose profit was itself depressed by a one-off tax transition, not a business generating three times the earnings power it had a year ago.

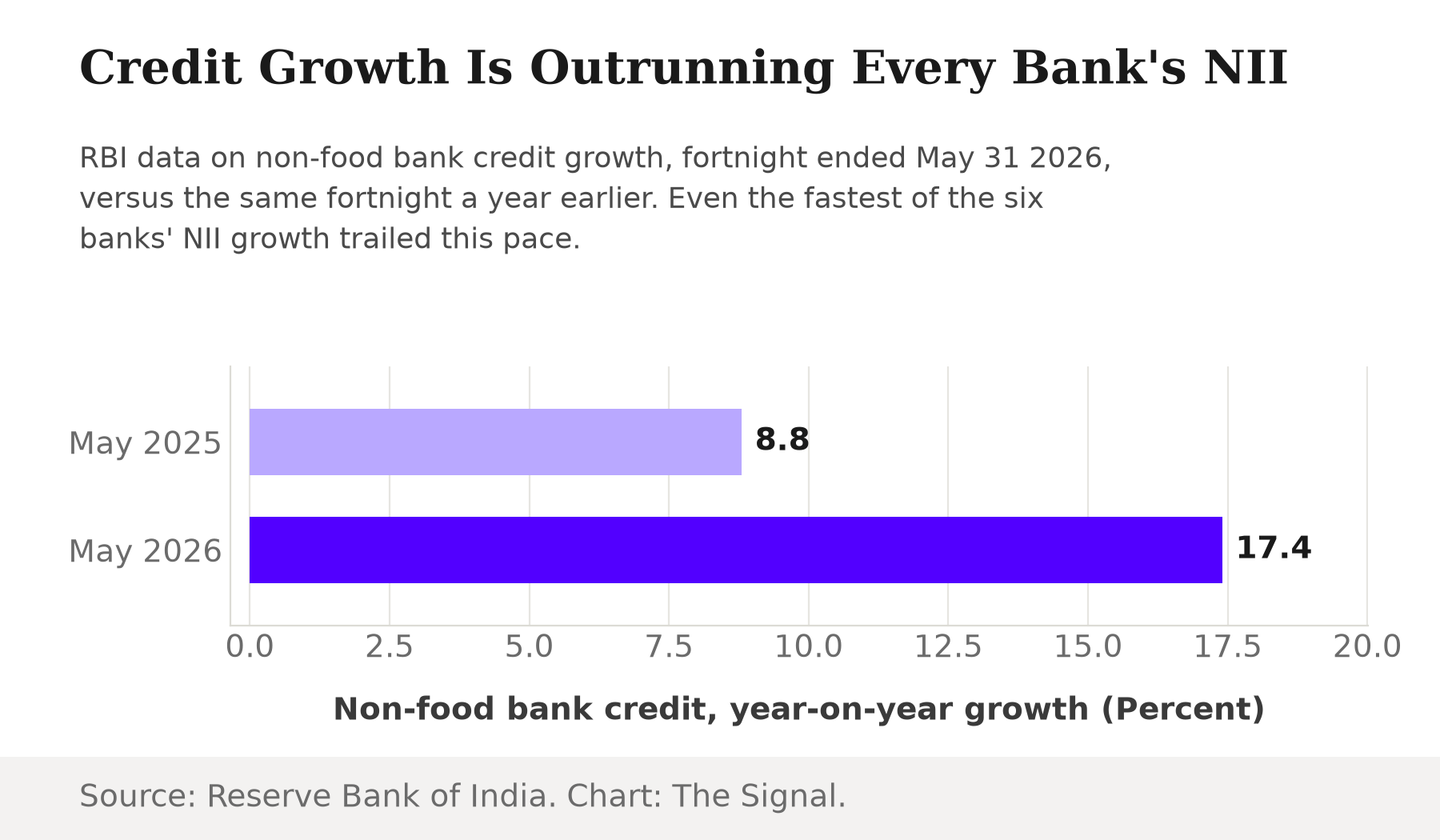

The credit boom does not close the gap either

The other place to look for an explanation is the lending side of the whole banking system, not just six banks. The Reserve Bank of India's non-food bank credit grew 17.4 percent year-on-year in the fortnight ended May 31, 2026, more than double the 8.8 percent growth in the same fortnight a year earlier. If credit demand across the system is accelerating that sharply, a reasonable expectation is that individual banks' core lending income should be accelerating too.

Source: Reserve Bank of India. Chart: The Signal.

None of the six banks got there. ICICI's 12.7 percent NII growth was the fastest of the group, still nearly 5 points behind the system-wide credit pace. A bank's lending book can grow in volume while its net interest income grows more slowly if the interest margin on new and existing loans is being squeezed, from competition for borrowers, a shift toward lower-yielding loan categories, or deposit costs rising faster than lending rates. The RBI's Monetary Policy Committee held the policy repo rate unchanged at 5.25 percent at its June 3-5, 2026 meeting, so the rate anchor itself did not move during the quarter, which makes a margin squeeze, rather than a policy shock, the more likely reason credit is growing faster than any single bank's lending income.

The honest objection

The strongest case against reading anything sinister into this is that quarterly bank profit is a noisy number for reasons that have nothing to do with lending. A one-off tax adjustment, a treasury gain on bond holdings, a low base from a genuinely bad year-ago quarter, or a recovery on a single large written-off account can all swing reported profit by double digits without saying anything about the health of the core business. PNB itself was recovering from a weak comparative base: its year-ago profit was Rs 1,675 crore, itself a depressed figure. Banks with cleaner, more stable year-ago comparisons, ICICI and HDFC, show profit and lending income moving together, which is exactly what a normally functioning quarter looks like.

That case is real, and the tax base-effect traced above is exactly this kind of noise, not evidence of anything improper. But it does not make the underlying question go away. PNB's 213.6 percent profit jump is mostly a comparison against an unusually tax-heavy year-ago quarter, and it arrived in a quarter when the bank's own bad-loan provisioning doubled, the signal analysts usually read as risk rising, not falling. A base-effect gain that big, sitting on top of a rising provisioning charge and lending income growing barely faster than inflation, is precisely the kind of profit that does not repeat next quarter.

The Signal

Six large Indian banks filed Q1 FY27 results in the same week, and system-wide non-food credit growth reached 17.4 percent in the fortnight to May 31, 2026, more than double the year-earlier pace. Yet the bank that posted the most dramatic profit growth of the six is the one whose own lending income and provisioning both moved the way analysts usually read as a warning, not a celebration. The gap does not prove PNB's profit is fake. It proves the profit and the lending business are, this quarter, telling two different stories, and only one of them is repeatable. The number to watch next quarter is not the profit growth rate. It is whether PNB's NII growth catches up to the 17.4 percent pace the rest of the credit system is already running at, or whether its provisions keep climbing while the lending income stays flat.

Reporting basis: Punjab National Bank's profit and net interest income figures are per Business Today's reporting of the results; its provisioning figure is per The Print's reporting of the same results; its income-tax provision figure is per NewsDrum's reporting of the same results; its year-ago tax-regime transition is per PSU Watch's reporting of PNB's Q1 FY26 results. ICICI Bank's, Kotak Mahindra Bank's and Yes Bank's results are per Business Today. HDFC Bank's results are per Free Press Journal. IDBI Bank's results are per Business Today. The system-wide credit growth figures and the repo rate decision are from the Reserve Bank of India's own releases. The point gap between system credit growth and each bank's NII growth, and the tax-provision swing's share of PNB's profit rise, are The Signal's calculations from those figures.