Vikram-1 is a four-stage, seven-storey-tall rocket built by the Hyderabad startup Skyroot Aerospace, founded in 2018. It lifted off from Sriharikota at 11:30 am IST on July 18, ThePrint reported. Fifteen minutes later its upper stage reached the planned 450-kilometer low Earth orbit, SpaceNews reports, making Vikram-1 the first privately built Indian rocket to reach orbit. The easy headline writes itself: an Indian startup has joined the short list of companies anywhere that can put something into orbit on a rocket of its own design.

It is worth pausing on that read. Vikram-1's flight is not really an engineering story, or not only one. It is a capital-structure story, and the Union Budget numbers behind it explain India's approach to building a private space industry better than the flight itself does.

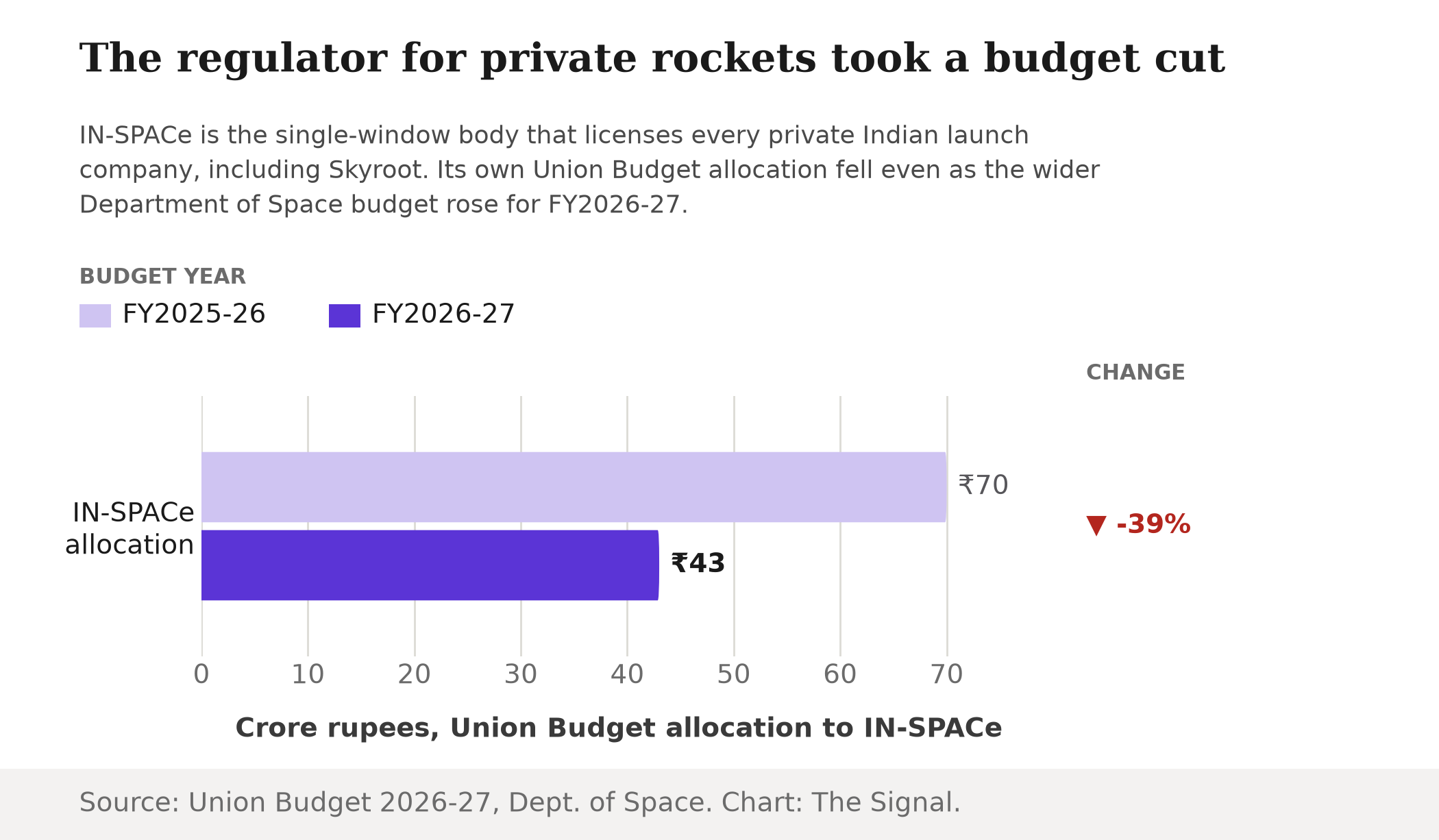

Start with the budget. The Department of Space's total budget rose to Rs 13,705.63 crore for FY2026-27, up from Rs 13,416.20 crore the year before, Union Budget 2026-27 documents show. Over that same year, the allocation for IN-SPACe, the single-window regulator that licenses every private launch company in the country including Skyroot, fell to just Rs 43 crore, down from Rs 70 crore, the same budget documents show.

The regulator built to attract private capital took a budget cut as the wider department budget expanded.

That is not a rounding effect buried in a much larger number. It is the line item directly tied to the policy bet Vikram-1 is supposed to be testing, moving the opposite way from the budget that contains it.

The tools built to attract private capital

IN-SPACe was not left to run on goodwill. The Department of Space has separately established a Rs 1,000 crore Venture Capital Fund and a Rs 500 crore Technology Adoption Fund to catalyse private investment and technology commercialisation in the space sector, the Department of Space told Rajya Sabha. Those two funds, not IN-SPACe's own operating budget, are the state's actual capital commitment to the sector, and they sit elsewhere in the government's books.

What IN-SPACe itself does is licensing and oversight, and that workload has only grown. It has issued 112 authorisations to non-government entities to date, 81 of them for space activities specifically, and its cumulative memoranda of understanding reached 72 in FY2025-26, ISRO's Annual Report 2025-26 states. A body clearing a growing docket of private launch and satellite companies is the one whose own funding just fell by roughly 39 percent.

Skyroot's own capital stack

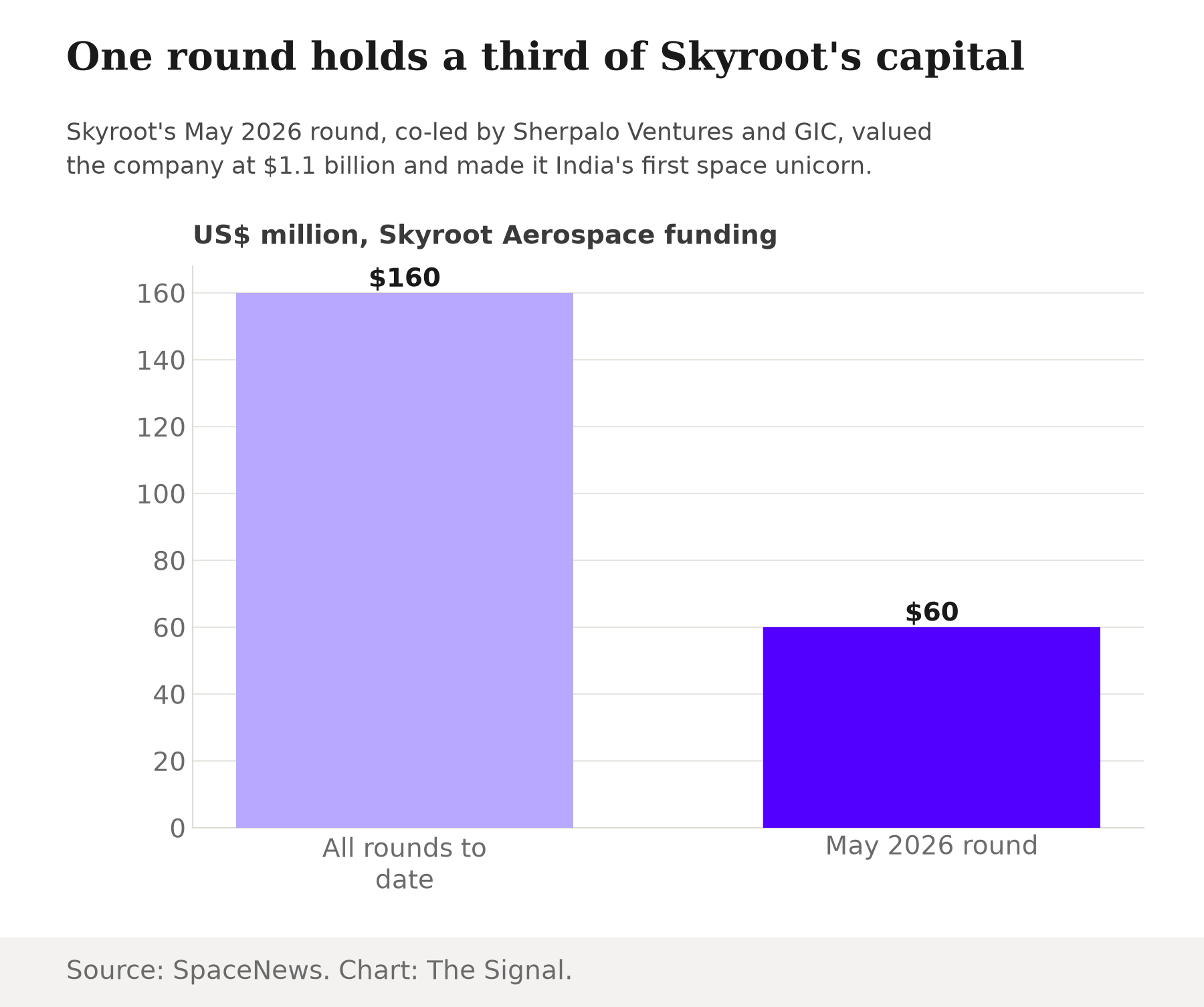

While the regulator's budget was shrinking, Skyroot was raising money on its own terms. The company raised $60 million in May 2026, co-led by Sherpalo Ventures and GIC, at a $1.1 billion valuation, its first "unicorn" round and India's first for a space company, taking its total capital raised to $160 million, SpaceNews reports. A single funding round, the one that closed roughly two months before liftoff, accounts for more than a third of everything the company has ever raised.

The rocket that money built was designed to carry up to 350 kilograms to low Earth orbit, with a launch window that opened July 12 and ran through August 4, SpaceNews reported before liftoff. Today's flight used that window on its first attempt. None of that capital came from IN-SPACe's operating budget. It came from Sherpalo Ventures and GIC, betting on a return the government's own Venture Capital Fund was designed to help crowd in, not replace.

The market this is supposed to grow

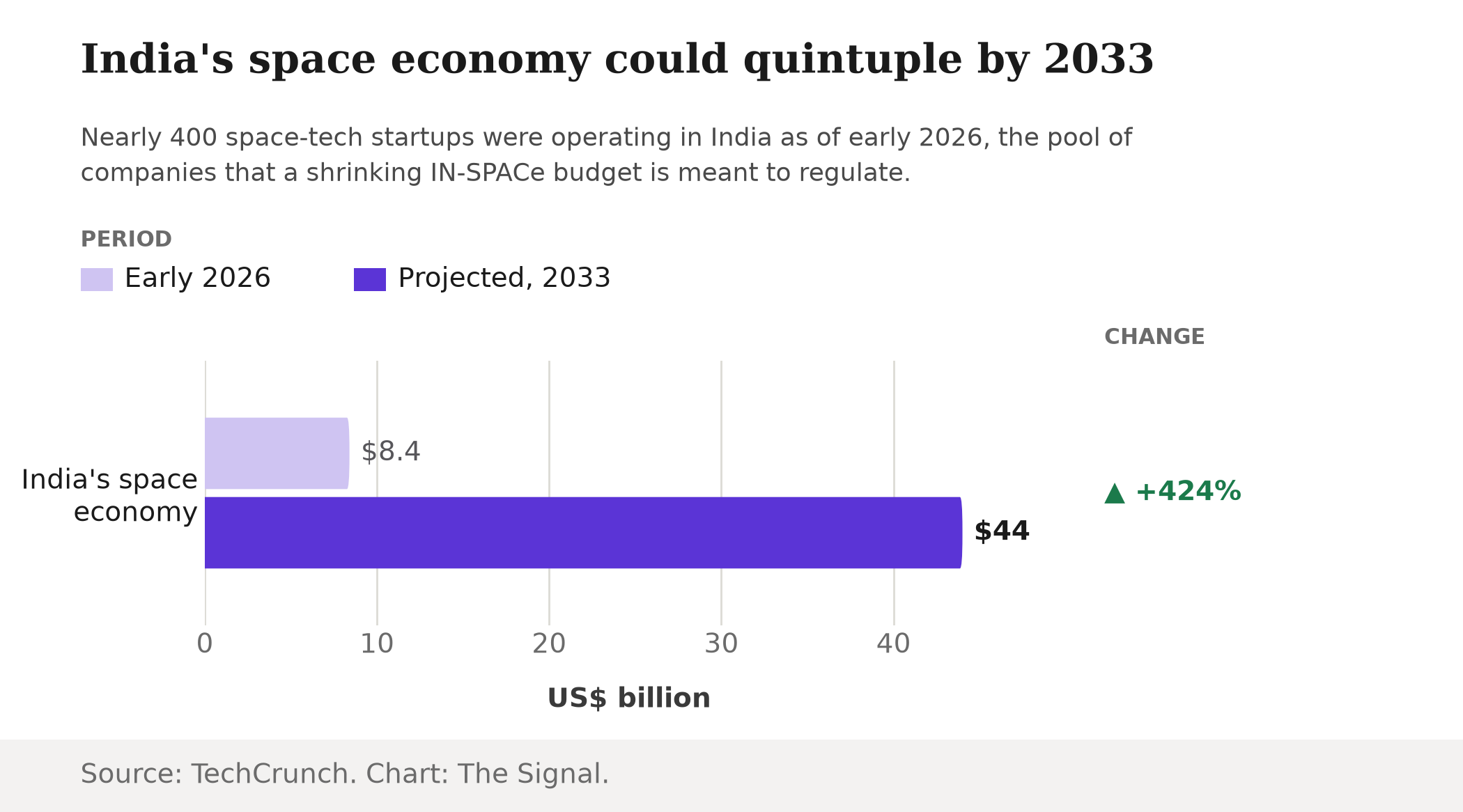

The bet only makes sense at scale. India's space economy is estimated at $8.4 billion and projected to grow to $44 billion by 2033, with the country home to nearly 400 space-tech startups as of early 2026, TechCrunch reports. That is the pool of companies IN-SPACe's shrinking budget is meant to license, monitor and clear for launch. The market is projected to expand roughly fivefold over less than a decade, on a regulatory allocation moving the other way.

The honest objection

The strongest case against reading anything into IN-SPACe's cut is that a licensing body is not a bank. Its job is approvals, inspections and paperwork, not writing checks, so its office budget was never going to track the size of the industry it oversees. On this view, the real state commitment to private space sits in the Rs 1,000 crore Venture Capital Fund and the Rs 500 crore Technology Adoption Fund, both of which sit in the Department of Space's wider budget, and a shrinking line for one regulator's own operations reveals little on its own about the government's appetite for the sector.

That case has real force, and it is why this piece treats the cut as a question rather than a verdict. But it does not fully explain the direction of travel. IN-SPACe's own authorisation count kept rising through FY2025-26, and the market it is meant to police is projected to reach nearly five times its current size by 2033. Even the venture fund held up as the state's real commitment has been slow to move: approved in October 2024, its first Rs 150 crore tranche for FY2025-26 went entirely unspent, and investments are expected to begin only from April 2027. A regulator whose caseload is expanding, and whose sector is not yet mature enough to police itself, is an odd place to look for savings, even a small one. That is especially true in the same year Skyroot needed a single venture round worth more than 13 times IN-SPACe's entire annual budget at prevailing exchange rates to get a rocket to the pad.

The Signal

Vikram-1's flight answers an engineering question: yes, a private Indian company can build a rocket that reaches orbit. It does not answer the policy question the launch was supposed to settle, which is whether India's decision to lean on private capital instead of a second ISRO can actually scale. That test runs through IN-SPACe, not the rocket, because IN-SPACe is the body that has to keep licensing and clearing every company like Skyroot as that list gets longer. Its budget just moved in the wrong direction to be reassuring. Watch next year's Union Budget for the same line item. If IN-SPACe's allocation recovers as the sector's authorisation count keeps climbing, the state is backing its own policy. If it keeps falling, venture capital is not supplementing the government's bet on private space. It is carrying it alone.

Reporting basis: the Venture Capital Fund and Technology Adoption Fund figures are from the Department of Space's reply to Rajya Sabha, via a Press Information Bureau release. IN-SPACe's authorisation and memoranda-of-understanding counts are from ISRO's Annual Report 2025-26. The Department of Space's total budget and IN-SPACe's own allocation, for both FY2025-26 and FY2026-27, are from the Union Budget 2026-27 documents. Skyroot's May 2026 funding round, its valuation, its total capital raised, Vikram-1's design specifications and launch window, and confirmation that the rocket reached orbit are all as SpaceNews reported. India's space economy's current size, its projected 2033 size and the national space-tech startup count are per TechCrunch. Vikram-1's physical description, Skyroot's founding year and the launch's local time are per ThePrint. The rupee-dollar exchange rate used to compare IN-SPACe's budget with Skyroot's funding round is the US Federal Reserve's H.10 release for the week of July 6-10, 2026. The Venture Capital Fund's disbursement delay is per WION, relaying Union Minister Dr. Jitendra Singh's written reply in the Lok Sabha. The percentage changes in the Department of Space's and IN-SPACe's budgets, and the share of Skyroot's total funding raised in its May 2026 round, are The Signal's calculations from those figures.