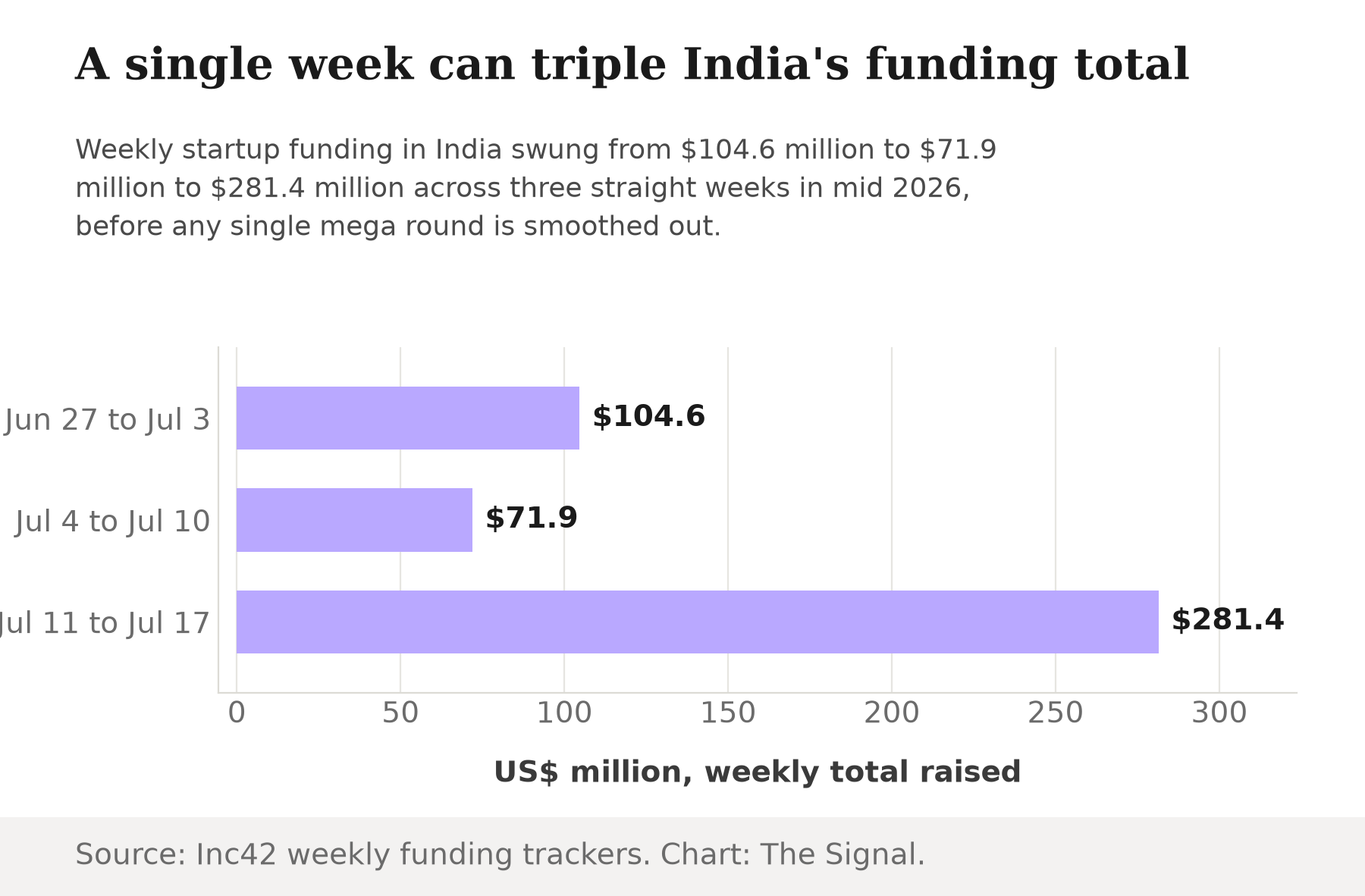

In the week of July 11 to 17, 2026, Indian startups raised $281.4 million across 24 deals, over three times the $71.9 million raised by 17 startups the previous week; AI companies alone took $172.4 million of that across just seven deals, nearly 60 percent of the week's total. It followed a quieter stretch: between July 4 and July 10, Indian startups had raised just $71.9 million across 17 deals, itself a 31 percent decline from the $104.6 million raised by 21 startups the week before that. A separate tracker counted the middle of that stretch differently: Entrackr found 18 Indian startups raising nearly $70.4 million between July 6 and July 11, split between just 3 growth-stage deals and 15 early-stage ones. Read any one of those weeks and the story writes itself: Indian startup funding is back, and AI is pulling it.

Source: Inc42; Inc42. Chart: The Signal.

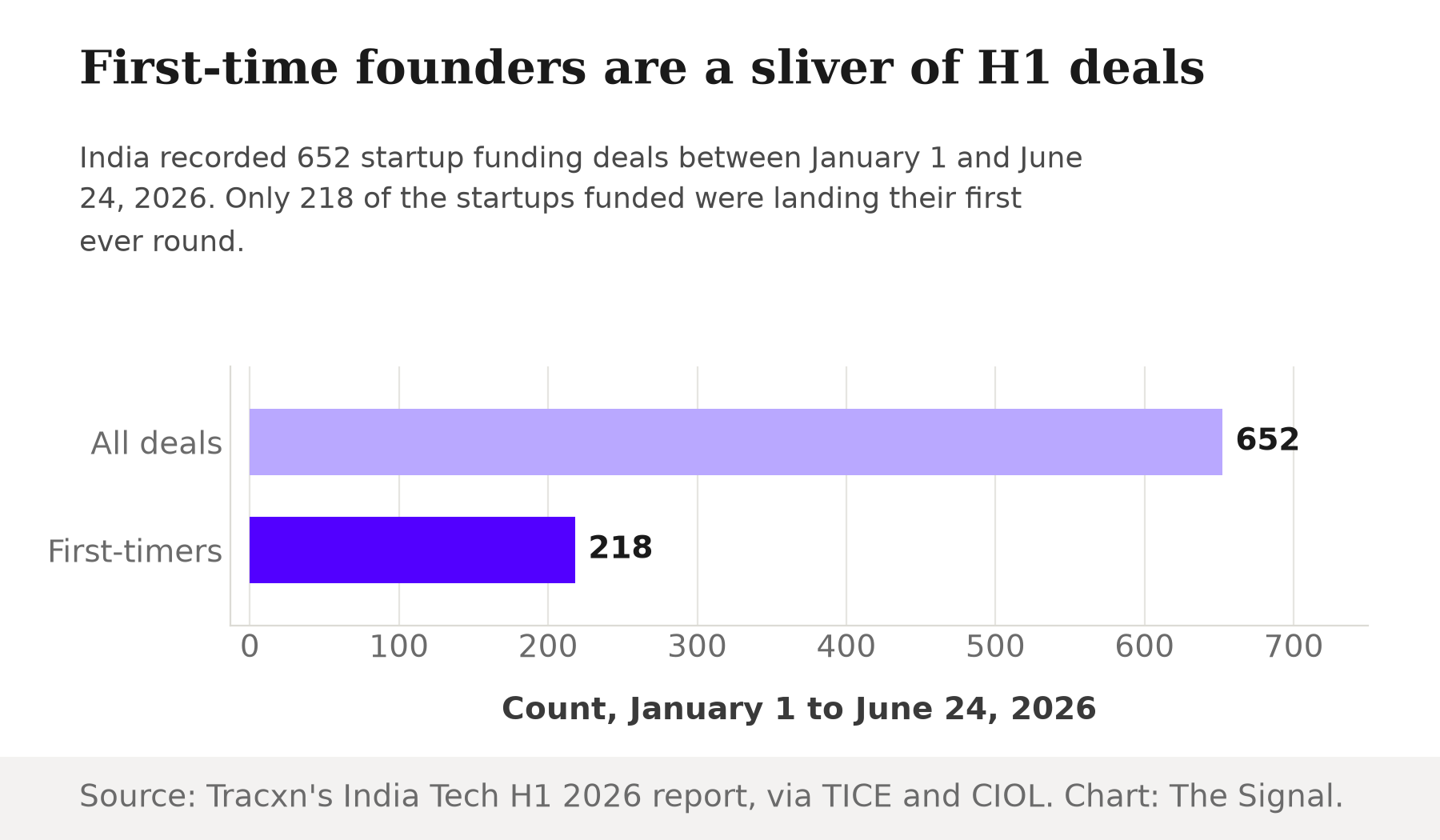

It is worth slowing down on that. A single mega-round can triple a weekly total, which is exactly why weekly trackers are noisy and half-yearly ones are not. Zoom out to the first half of 2026: Indian tech startups raised $7.2 billion across 652 deals between January 1 and June 24, 2026, a 12 percent increase over the same period last year, even as the number of funding transactions fell 43 percent year on year. Money is up. The number of companies splitting it is down by nearly half.

Funding rose 12 percent while the number of deals fell 43 percent, in the same six months.

Three rounds explain a large share of why the dollar total held up at all: CRED's $900 million, Nxtra's $710 million and Neysa's $600 million together made up almost 31 percent of all startup capital deployed in India in the first half of 2026. Fewer deals, bigger ones, concentrated at the top.

The funnel for new entrants is closing

The deal count is not the only thing shrinking. In that same window, the number of Indian startups landing a first-ever funding round fell 31 percent to just 218, and the count of active institutional investors dropped to 488, down sharply from prior highs. Of the 652 deals struck in the first half of the year, only a third went to a company raising money for the first time in its existence.

Source: TICE; CIOL, both reporting Tracxn's India Tech H1 2026 data. Chart: The Signal.

The investor pool is shrinking faster than the checks

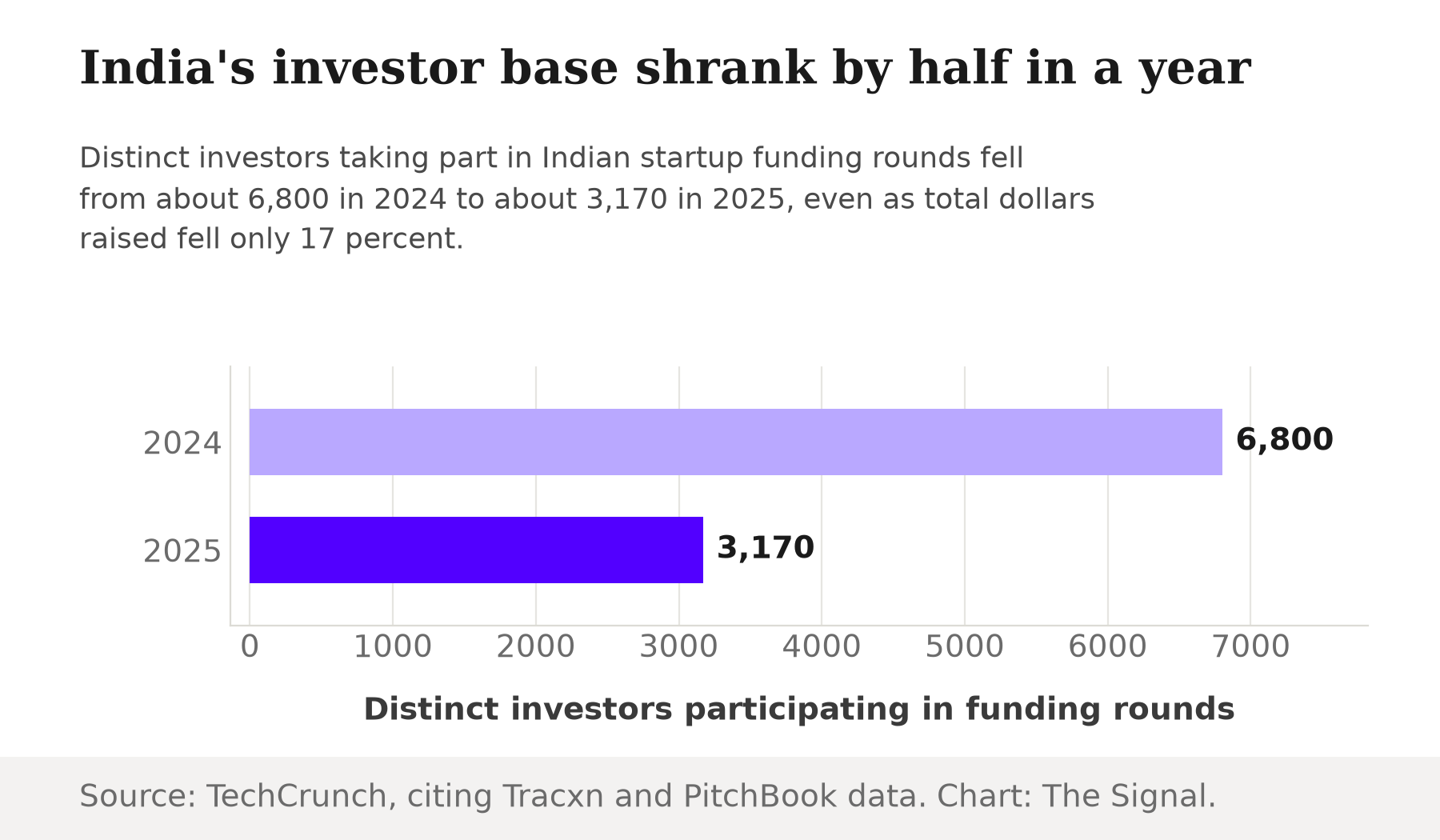

This is not a one-off blip. Over the full year 2025, India startup funding totaled $10.5 billion, down just over 17 percent from 2024; seed-stage funding fell even harder, down 30 percent to $1.1 billion, and the number of distinct investors participating in Indian rounds fell 53 percent to about 3,170, from roughly 6,800 in 2024. Total dollars fell by a sixth. The number of investors willing to write any check at all fell by more than half.

Source: TechCrunch, citing Tracxn and PitchBook data. Chart: The Signal.

Fewer investors are underwriting a funding total that barely moved.

That is the mechanism behind the weekly headlines. When a smaller pool of investors concentrates its checks into fewer, larger, more proven bets, a single mega-round from that pool is enough to triple a weekly total on its own, exactly what happened in the week of July 11 to 17. The volatility is not noise sitting on top of a stable market. It is what a thinning market looks like from week to week.

The capital pipe keeps getting fatter

None of this is a shortage of capital. It is a shortage of capital reaching new entrants. The formal venture fund industry that sits above all these deals kept growing through the same period the funnel was narrowing.

The funding funnel, at different altitudes.

| Metric | Figure | As of | Source |

|---|---|---|---|

| DPIIT-recognised startups (the total base) | 1,97,692 | 31 Oct 2025 | DPIIT, via PIB |

| SEBI Category I VC fund commitments | Rs 64,134 crore | 31 Mar 2026 | SEBI |

| SEBI Category I VC funds actually raised | Rs 38,899 crore | 31 Mar 2026 | SEBI |

| SEBI Category I VC funds actually invested | Rs 34,125 crore | 31 Mar 2026 | SEBI |

| Startups landing a first-ever funding round, H1 2026 | 218 | Jan 1 to Jun 24, 2026 | Tracxn, via CIOL |

Source: DPIIT via PIB, SEBI, and Tracxn via CIOL, as linked per row. Table: The Signal.

SEBI-registered Category I Venture Capital Funds held cumulative commitments of Rs 64,134 crore as of March 31, 2026, of which Rs 38,899 crore had actually been raised and Rs 34,125 crore invested. That committed pool of formal VC capital keeps growing even as the base it could theoretically reach is enormous: the Department for Promotion of Industry and Internal Trade had recognised 1,97,692 entities as startups under the Startup India initiative as of October 31, 2025. Against a registered base approaching two lakh, 218 first-time fundraises in six months is a rounding error. The money is not the constraint. Who it reaches is.

The honest objection

The strongest case against calling this concentration is that it could simply be the market maturing. After a funding winter, investors often circle back to proven teams and follow-on rounds before opening checkbooks to new names again; fewer, bigger, better-vetted bets can be a sign of capital discipline, not capital flight. The gap between two independent weekly trackers is also a reminder that these are noisy, overlapping counts, not a single clean series: Entrackr counted 18 startups raising nearly $70.4 million in a week that Inc42 counted differently.

That case holds for the deal-count decline alone. It does not explain why the number of distinct investors participating fell 53 percent in a single year, from about 6,800 in 2024 to about 3,170 in 2025, a contraction in who is writing checks, not just how many deals get done. Nor does it explain why first-time founders specifically fell to just 218 funded in six months while the formal VC-fund vehicle industry kept adding to its Rs 64,134 crore in commitments. A maturing market rotates capital toward quality. It does not simultaneously shrink its own investor base and lock out new entrants while the money on the sidelines keeps growing.

The Signal

The headline number every week is the dollar total, because it is the easiest thing to compare to last week. The number that actually describes the market is how many distinct companies, and how many distinct investors, touched that money at all: both fell through 2025 and the first half of 2026 even as the dollar total rose. Watch the second half of 2026: if Tracxn's next report shows first-time-funded startups recovering off the 218 count, this is a temporary flight to quality. If that count keeps falling while committed VC capital keeps climbing, India's funding market is not growing. It is just concentrating.

Reporting basis: the weekly funding figures for July 2026 are per Inc42's weekly funding trackers, with an independent count for the same window from Entrackr. The first-half 2026 totals, deal count, top-three-deal concentration, first-time-founder count and investor count are per Tracxn's India Tech H1 2026 report, as reported by TICE and by CIOL respectively. The full-year 2025 funding, seed-stage and investor-count figures are per TechCrunch, citing Tracxn and PitchBook data. The SEBI Alternative Investment Fund figures are from SEBI's own published statistics. The DPIIT startup count is from a Press Information Bureau release citing DPIIT data. The observation that 218 is roughly a third of 652, and that the registered startup base of nearly two lakh dwarfs the first-time-funded count, are The Signal's calculations from those figures.