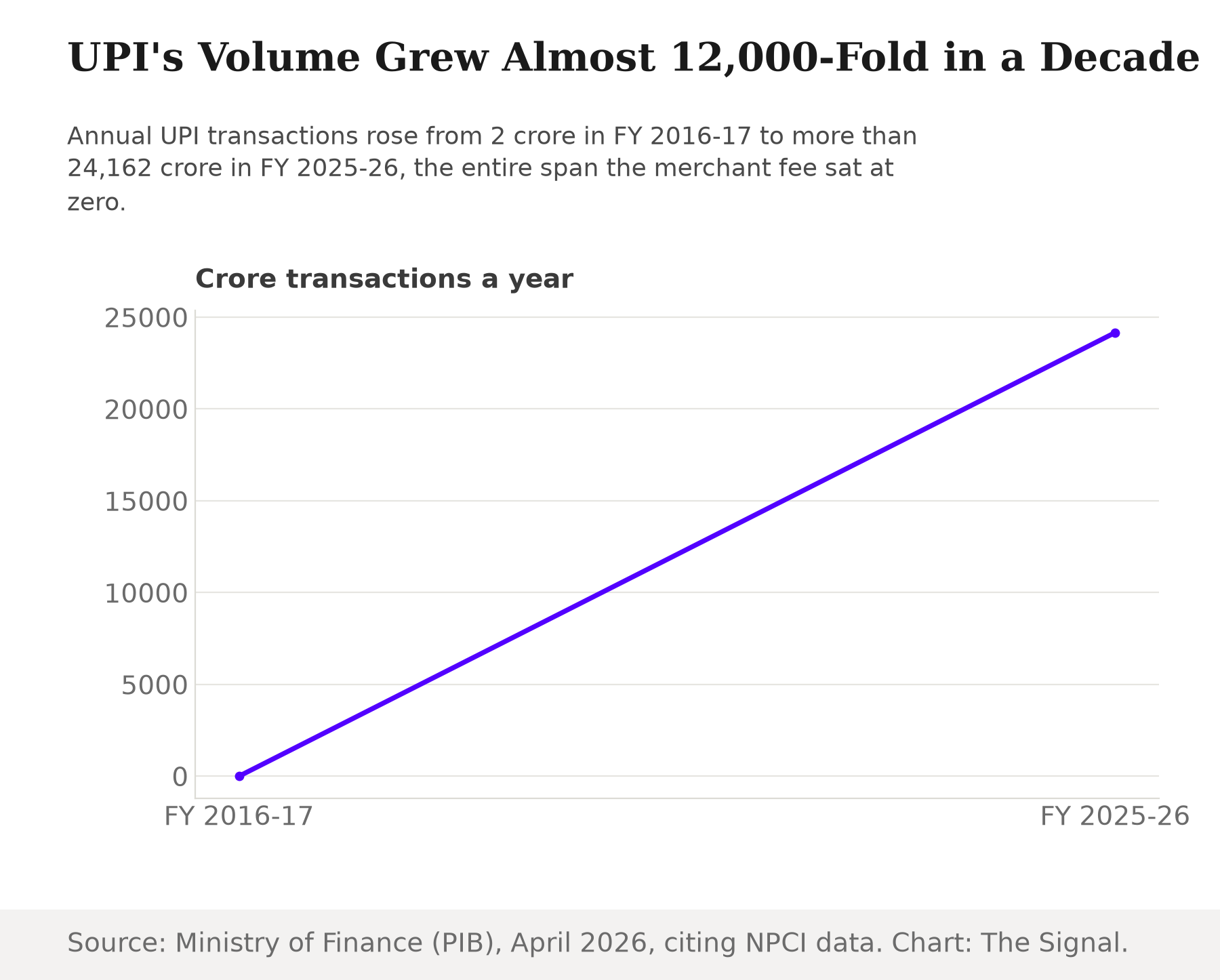

Since 1 January 2020, UPI and RuPay debit card payments in India have carried no merchant discount rate at all. The Ministry of Finance confirms the fee was zeroed out that month, replacing statutory ceilings that had allowed banks to charge up to 0.90 percent on debit cards and up to 0.30 percent on UPI merchant payments, a move made specifically to push transactions off cash and off costlier card rails. It worked. Annual UPI transaction volume crossed 24,162 crore, worth roughly Rs 314 lakh crore, in the financial year that ended in March 2026.

UPI's annual transaction volume has grown almost 12,000-fold since the fee disappeared.

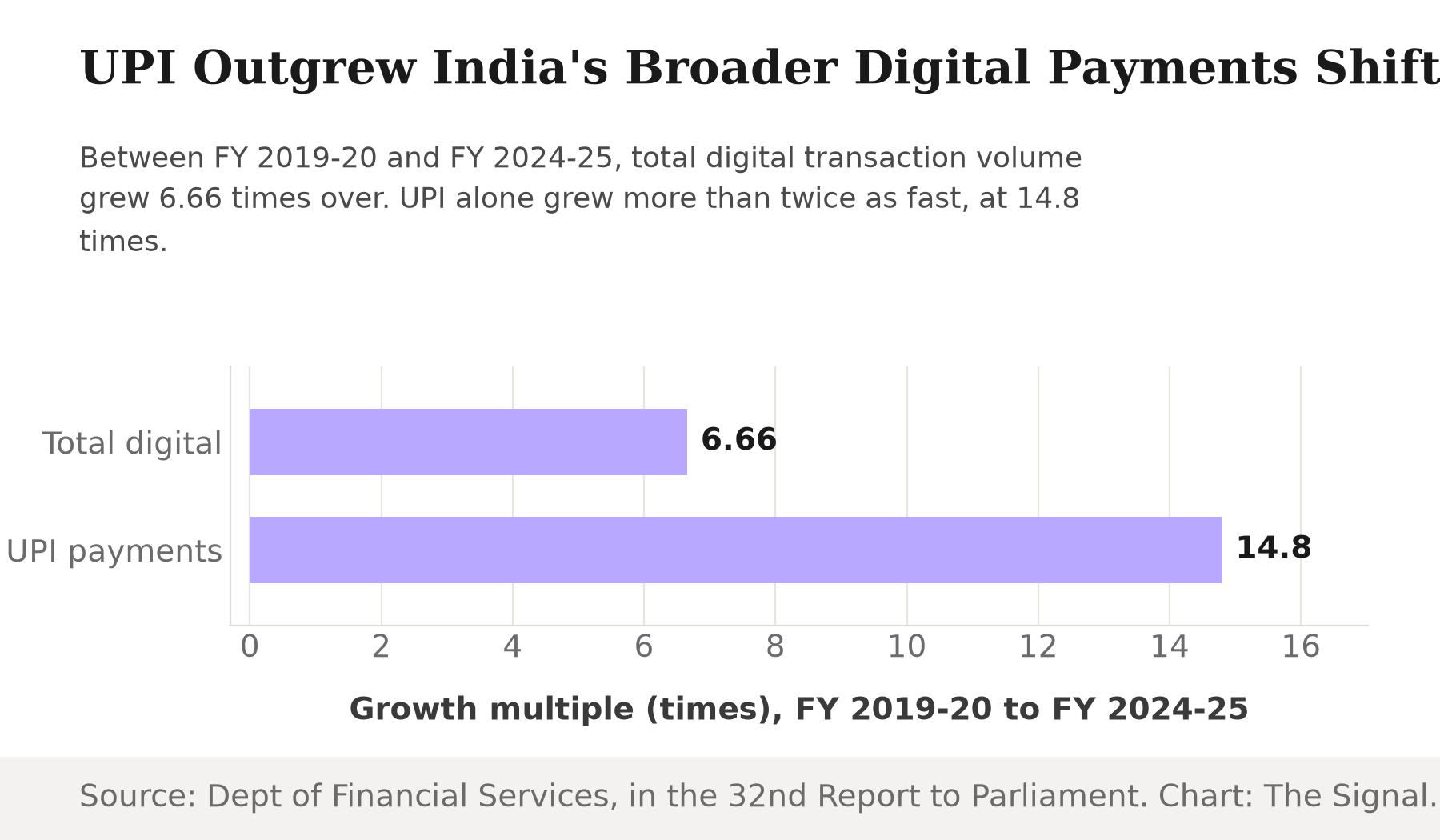

Total digital transaction volume in India grew 6.66 times over between FY 2019-20 and FY 2024-25. UPI alone grew 14.8 times over the same five years, more than double the pace of digital payments generally.

It is worth slowing down on what actually paid for that growth. The zero fee was never free to run. The government replaced the merchant fee with a taxpayer-funded incentive scheme, and the scheme's own design already drew a line it now wants to formalize. Under the Cabinet-approved scheme, large merchants get zero MDR and no government incentive at all on UPI transactions, while only small merchants earn a 0.15 percent incentive, and only on transactions up to Rs 2,000.

Large merchants have never received a rupee of the government's UPI incentive scheme.

| Merchant category | Up to Rs 2,000 | Above Rs 2,000 |

|---|---|---|

| Small merchant | Zero MDR, plus 0.15% government incentive | Zero MDR, no incentive |

| Large merchant | Zero MDR, no incentive | Zero MDR, no incentive |

Source: PIB, on the Cabinet-approved BHIM-UPI incentive scheme.

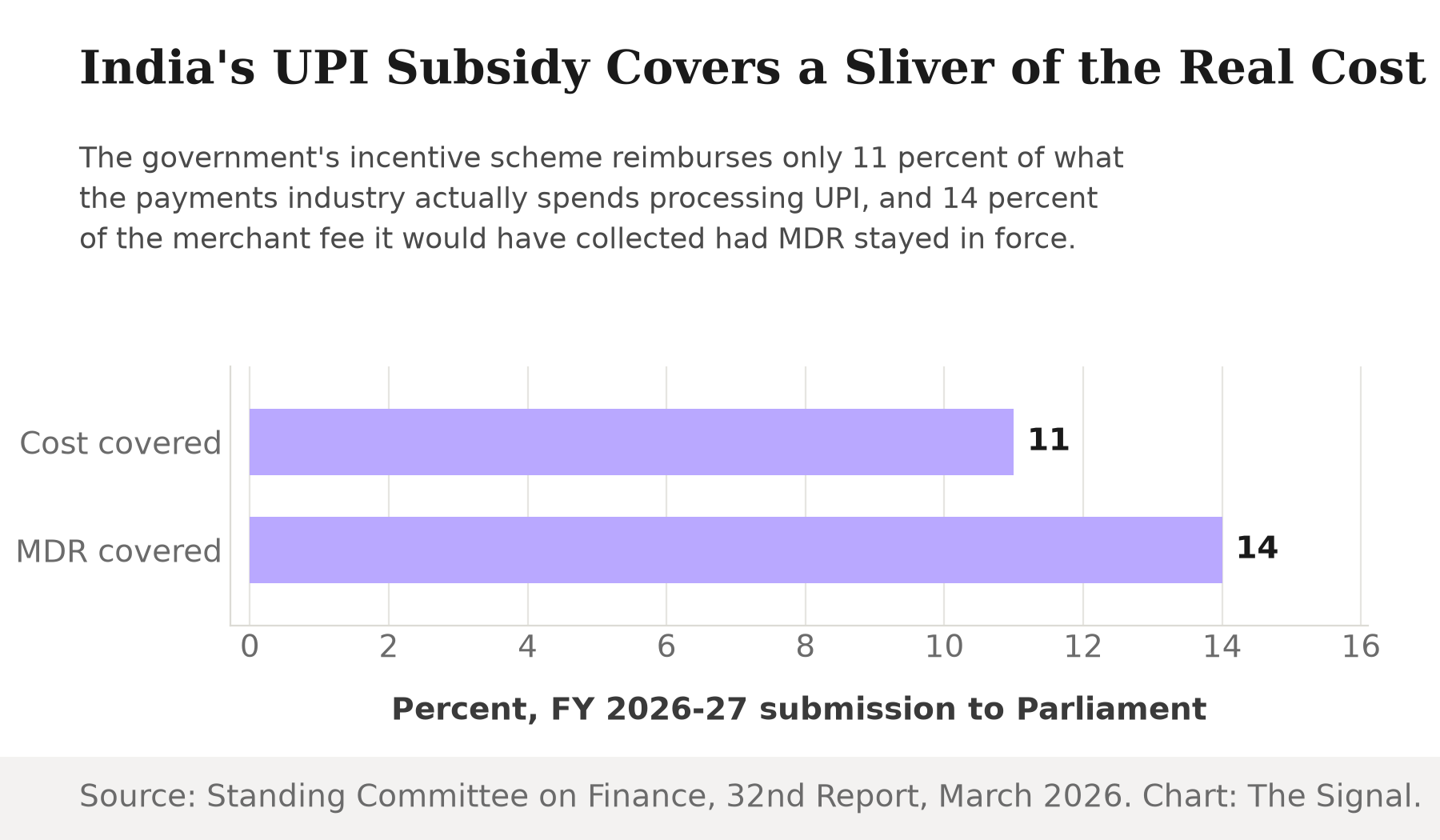

That gap is not a rounding error. Transactions above Rs 2,000 already make up 67 percent of total UPI transaction value, and that is exactly the ticket size the incentive scheme excludes. Banks and payment companies have already been absorbing the cost of processing most of UPI's value with no government support, for as long as the zero-fee rule has existed. Zoomed out, the incentive scheme covers only 11 percent of what the payments industry actually spends running UPI, and just 14 percent of the MDR revenue it would have collected had the fee never gone to zero.

The proposal on the table

That is the backdrop to the proposal now under discussion. The government is weighing a merchant discount rate below 0.5 percent on UPI transactions above Rs 2,000, for large merchants only, with no charge passed to shoppers, and a decision was expected within two weeks of mid-July 2026. Officials were direct about what the change is and is not: "the MDR is not about charging consumers for UPI transactions," the Free Press Journal reported them saying, framing it instead as "merchant-side economics and sustainability of the payments ecosystem."

Read against the incentive scheme's design, the proposal is narrower than "reviving a fee" sounds. It targets the slice of UPI, large-merchant transactions above Rs 2,000, that the incentive scheme never subsidized to begin with. The zero-MDR rule stays intact everywhere it was ever backed by taxpayer money.

Why the math stopped adding up

The pressure behind the proposal is a growth trajectory the current funding was never built for. UPI is projected to add another 600 million users and scale to 100 to 150 billion transactions a month over the next five to seven years, a path the Standing Committee on Finance itself flagged as running into a structural funding gap. The Department of Financial Services has asked Parliament for a Rs 2,000 crore budgetary grant in FY 2026-27, specifically for the small-ticket incentive scheme, a bill that grows every year alongside volumes, while covering a shrinking share of a fast-expanding system.

The committee's own response was blunt. It directly asked the Department of Financial Services whether it could adopt a tiered model, charging banks and larger entities while keeping BHIM-UPI free for street vendors and small businesses. The large-merchant MDR now under discussion reads like a direct answer to that question, not a reversal of the policy that made UPI ubiquitous.

Nor is the pressure coming only from the government side. The Payments Council of India, the industry body for payment companies, has itself written to the Prime Minister's Office demanding a 0.30 percent MDR on UPI transactions at large merchants, arguing that only about 50 lakh of India's 6 crore merchants would be affected. The businesses that carry UPI's processing costs today are among those asking to formalize a fee for it.

The honest objection

The strongest case against touching the fee at all, even at the edges, is that UPI's growth has compounded precisely because it stayed free at the point of sale for six straight years, and any fee anywhere in the chain risks the flywheel that produced the volumes above. Once a size-based distinction exists between merchants, banks and payment apps gain a standing reason to lobby for wider fees over time, and today's promise of "no charge to the consumer" is only as durable as the government that made it. That worry has a precedent worth weighing: in August 2022, days after an RBI discussion paper floated charging UPI transactions, the Finance Ministry publicly shut the idea down, saying UPI is a "digital public good" and that there were "no intentions within the government to charge for UPI services". The zero-fee promise has already survived one serious challenge.

That case has real force, but it runs into two specifics of this proposal. First, officials framing the change were explicit that it targets merchant-side economics, not consumer charges, and only transactions above Rs 2,000. Second, the segment being asked to pay is the one segment that was already carrying its own processing costs commercially, since the incentive scheme never covered large merchants or transactions above Rs 2,000 to begin with. Nothing is being taken from small shopkeepers. The parliamentary recommendation driving this proposal explicitly protects street vendors and small businesses from any new fee.

The Signal

The headline read as "India brings back the UPI fee it killed" invites a reversal narrative the mechanics do not fully support. The government is not undoing the 2020 policy. It is drawing a line around the part of that policy it never actually funded, and asking the segment that already pays its own way, quietly, through bank and payment-company margins, to pay through a visible fee instead. Watch the small-merchant side of the incentive scheme once the FY 2026-27 budget is finalized. If that funding stays in place alongside a large-merchant MDR, the tiered model the committee asked for is taking shape as designed. Trim the small-merchant incentive once large merchants start paying, though, and the promise made in mid-July 2026 that consumers will not be charged will not have held for long. A subsidy that covers a sliver of the real cost was never going to survive the scale UPI is now built for.

Reporting basis: the January 2020 zero-MDR policy and the FY 2025-26 UPI transaction volumes are from Ministry of Finance releases via the Press Information Bureau, drawing on RBI and NPCI data. The Cabinet-approved incentive scheme's merchant-category terms are also from a Press Information Bureau release. The incentive scheme's cost coverage, the value share above Rs 2,000, the digital and UPI growth multiples, the FY 2026-27 budgetary request, the growth projections, and the committee's tiered-charging question are all from the Standing Committee on Finance's 32nd Report to the 18th Lok Sabha, as hosted by MediaNama. The pending large-merchant MDR proposal and the officials' framing of it are as reported by the Free Press Journal. The Payments Council of India's own push for a large-merchant MDR is as reported by Inc42. The 2022 episode, in which the RBI floated UPI charges and the Finance Ministry rejected the idea, is as reported by India Infoline. The almost 12,000-fold volume increase and the pace comparison between UPI and total digital growth are The Signal's calculations from those figures.