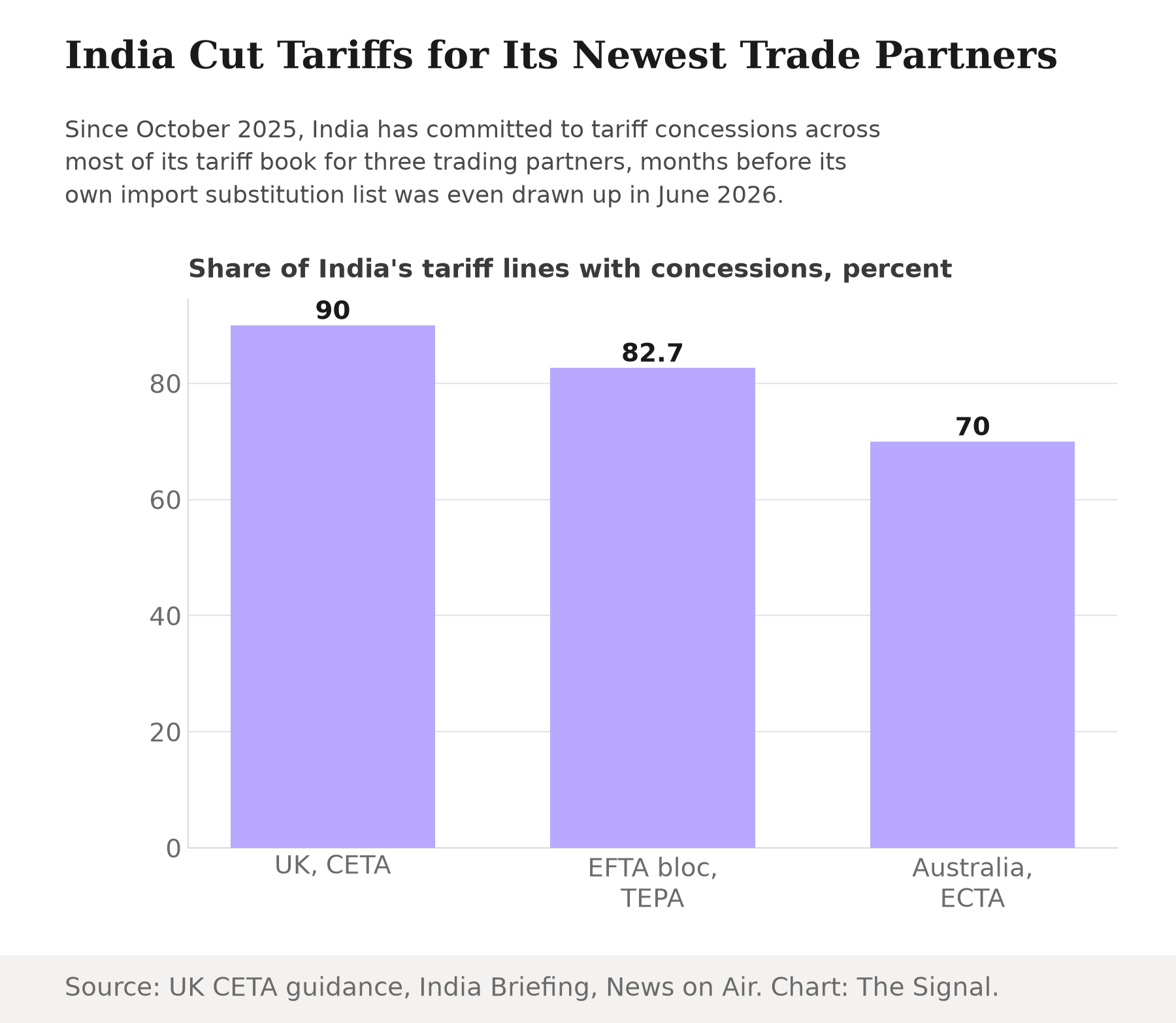

Two days ago, on July 15, 2026, the India-UK trade deal took effect, and the UK government's official CETA guidance states that India will remove or reduce tariffs on 90 percent of its tariff lines with Britain, cutting 64 percent of them immediately and rising to 85 percent after ten years of staged reductions. The clearest single example landed on drinks shelves: India Briefing reports, citing Annex 2A of the treaty's tariff schedule, that the duty on Scotch whisky fell from 150 percent to 75 percent the moment the deal took effect, on its way to 40 percent over the next decade.

Five weeks earlier, in June 2026, the commerce ministry had assembled a different kind of machinery entirely. KNN India reports that six sector-specific working groups, chaired by the DPIIT Secretary, were formed to shortlist up to 100 products for an import-substitution push, with a mandate to report back to the Cabinet Secretariat within three weeks. Read together, the plan writes itself: raise the tariff, make the import expensive, let the domestic factory fill the gap.

It is worth slowing down on that. For any product line that also happens to sit inside the UK deal, or inside India's other two recent trade agreements, that instrument is not in the toolbox anymore. It has already been signed away.

Three deals, one squeezed lever

All India Radio's News on Air reported that the India-EFTA Trade and Economic Partnership Agreement, which took effect on October 1, 2025, carries a binding commitment from the four-nation European Free Trade Association bloc to invest $100 billion in India over 15 years and generate one million jobs; in return, India Briefing reports that India offered concessions on 82.7 percent of its own tariff lines to EFTA, covering 95.3 percent of the bloc's exports to India. And News on Air reported that under the Australia-India ECTA, effective January 1, 2026, India offers preferential tariff access on more than 70 percent of its tariff lines to Australia, chiefly coal, mineral ores and wine, while every Indian tariff line gained duty-free entry into the Australian market on the same date.

Stack the three deals together and the pattern is not a handful of carve-outs. It covers the bulk of India's tariff book, conceded to three separate partners, before the substitution list was even drawn up.

Source: UK government CETA guidance; India Briefing, on the EFTA TEPA; News on Air, on the Australia ECTA. Chart: The Signal.

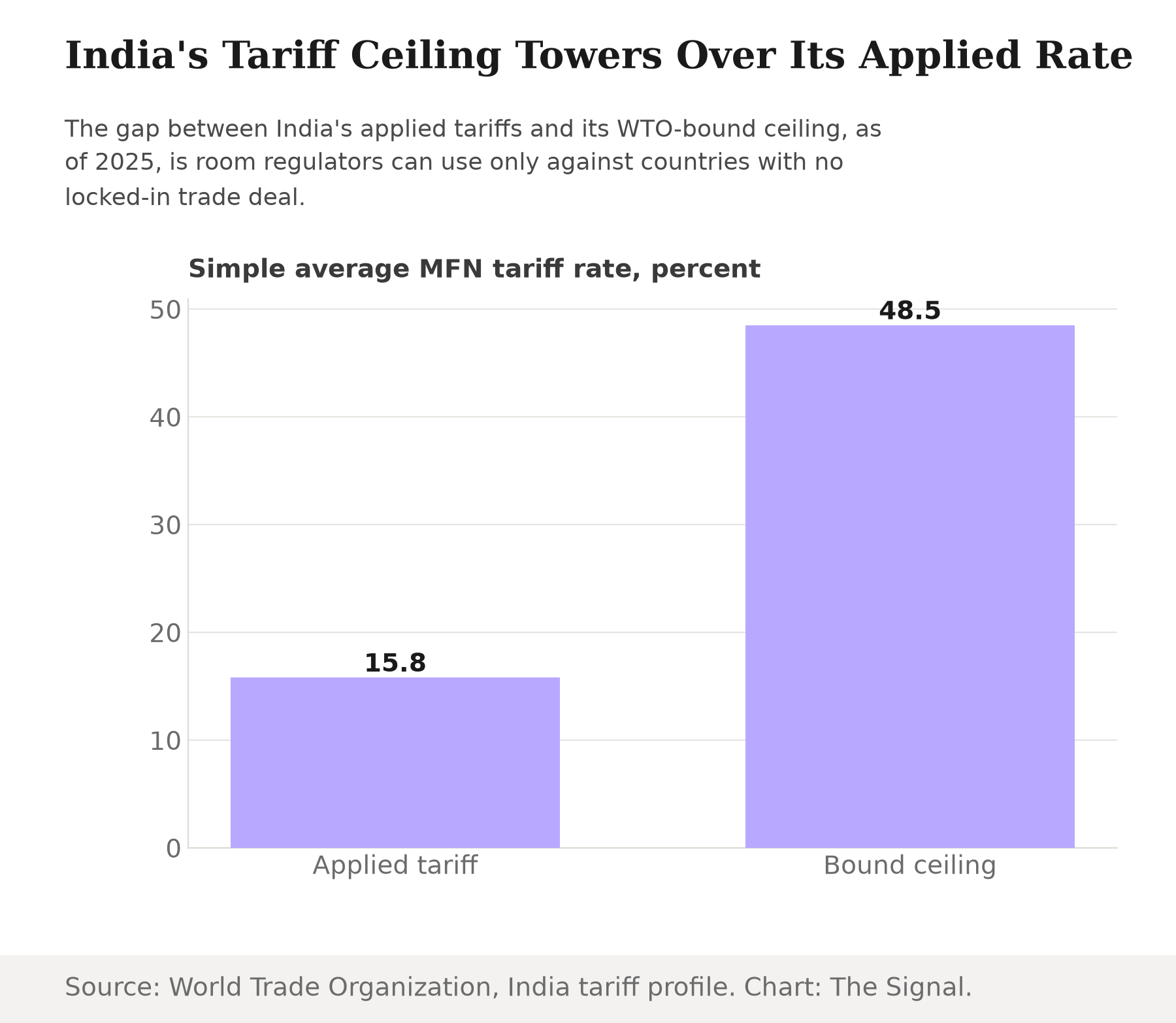

The headroom that does not reach everywhere

India still has real room to raise tariffs, in principle. The WTO's tariff profile for India shows a simple average MFN applied tariff of 15.8 percent against a simple average bound tariff of 48.5 percent, with 74.4 percent of tariff lines legally bound, as of 2025. That 33-point gap is the ceiling the WTO allows India to raise applied tariffs to, for any product and any partner, without breaching a commitment.

Source: WTO Tariff Profile: India. Chart: The Signal.

The gap is real, but it is not available everywhere at once: for any tariff line covered by the UK, EFTA or Australia deals, that headroom is fenced off by treaty, in some cases for a decade. Raising the rate on Scotch whisky, or any category now moving toward zero duty for those partners, would not be a policy choice under WTO rules. It would be breaking a bilateral commitment signed months, not decades, ago.

Where the tariff wall still stands

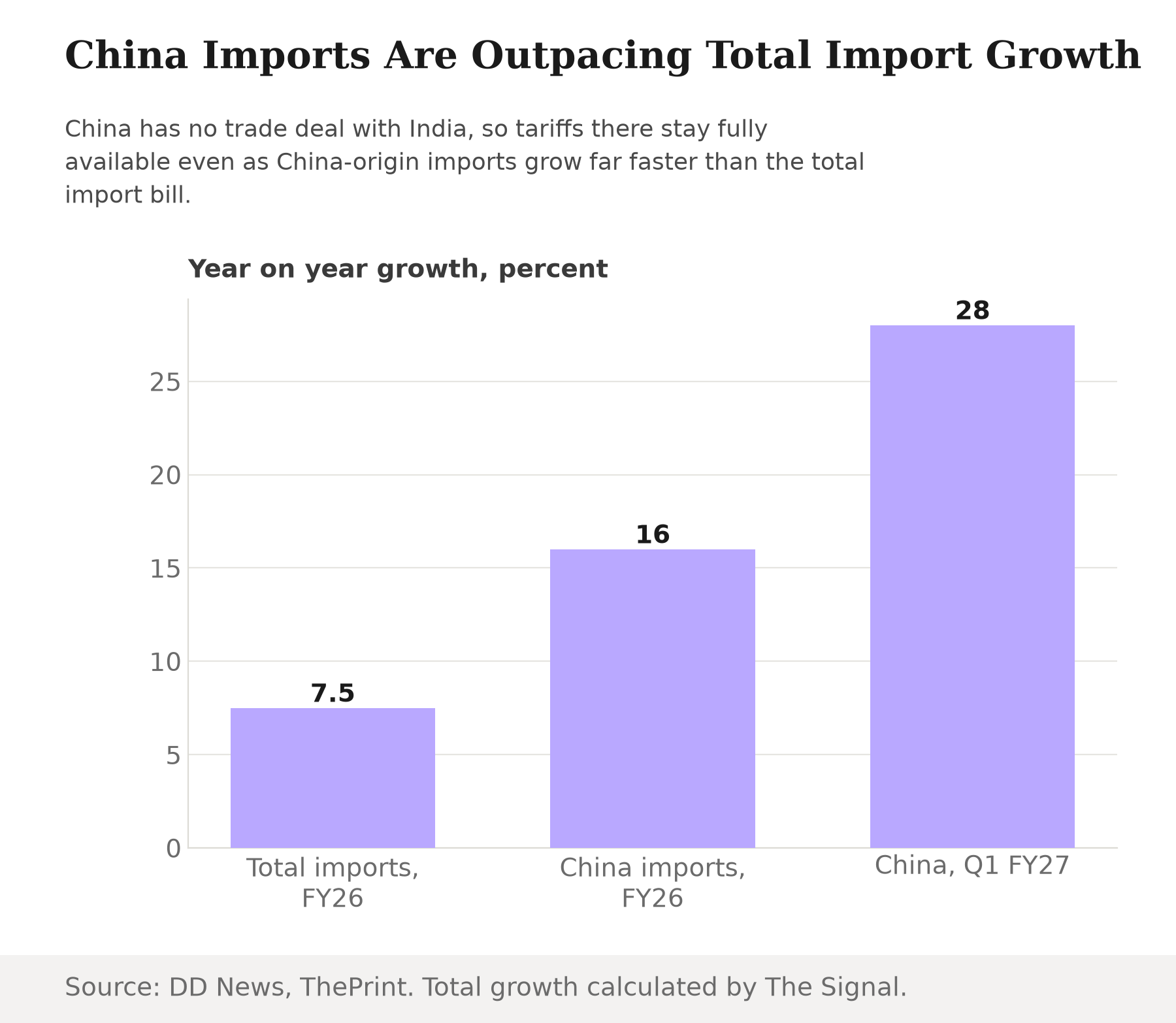

Not every import falls under one of the three deals. China has no free-trade agreement with India, so the tariff constraint does not apply there. ThePrint reports, citing Ministry of Commerce and Industry data, that India's imports from China rose 16 percent to $131.6 billion in FY2025-26, then a further 28 percent in the first quarter of FY2026-27, April to June 2026, to about $38.04 billion. Whatever ends up on the list, if those products are sourced mainly from China or another partner with no FTA, the WTO's full 33-point gap stays open for use.

Source: DD News, citing Commerce Secretary Rajesh Agrawal; ThePrint, citing Ministry of Commerce and Industry data. Total-import growth rate is The Signal's calculation. Chart: The Signal.

Put in dollar terms, the trade sitting inside the three treaty-constrained lanes is small next to that. BusinessToday reports, citing the Commerce Ministry, that India's total merchandise imports from the UK were $11.68 billion in FY2025-26, and DGCI&S data show India imported $15.77 billion from Australia and $25.17 billion from Switzerland, the largest EFTA economy, in calendar year 2024. Add all three together and it is still less than half of the $131.6 billion China alone supplied in FY2025-26. The percentage-of-tariff-lines conceded is large, but the trade value it constrains is the smaller pool next to the lane that stays fully open.

That split matters because the pressure behind the working groups is real, not manufactured. DD News reported, citing Commerce Secretary Rajesh Agrawal, that India's merchandise imports rose to $774.98 billion in FY2025-26 from $721.20 billion the year before, about a 7.5 percent increase, while the combined merchandise-and-services trade deficit widened to $119.30 billion from $94.66 billion. The urgency is not invented. What has narrowed is which lever answers it, and for which countries.

The tools that still work

Where the tariff option is gone, the government already has an alternative built. The Bureau of Indian Standards lists 29 Quality Control Orders notified and due for implementation between July 2026 and June 2027, as of July 1, 2026. A QCO sets a mandatory technical or safety standard and can block a substandard shipment without touching a customs schedule, so no FTA's tariff-line commitments cover it. It works on British, Swiss or Australian imports exactly as it does on Chinese ones.

India's Production Linked Incentive scheme is the other working lever: it pays domestic manufacturers to build capacity, rather than taxing the import that competes with it.

| Metric | Figure | As of |

|---|---|---|

| Sectors covered | 14 | Dec 31, 2025 |

| Investment drawn | Over Rs 2.16 lakh crore | Dec 31, 2025 |

| Jobs created | More than 14.39 lakh, direct and indirect | Dec 31, 2025 |

| Incentives disbursed by government | Rs 28,748 crore | Dec 31, 2025 |

Source: DD News, citing a Ministry of Commerce and Industry statement.

Neither instrument needs an open tariff line or breaches a trade commitment, which is why they are the tools left standing wherever the tariff option has been signed away.

The honest objection

The strongest case against this reading is that the working groups' shortlist may have little to do with the UK, EFTA or Australia at all. China alone supplies a large share of the import categories that worry Indian officials, and China sits outside every one of these three deals. If the substitution push is really aimed at Beijing, the FTA constraint is a footnote, and the WTO's full tariff gap remains available for whatever the working groups choose.

That case would be stronger if China itself sat outside every one of India's tools, but it doesn't. The same QCOs and PLI incentives described above apply to Chinese-origin goods exactly as they apply to British, Swiss or Australian ones. Whichever country ends up supplying the working groups' 100 products, a standard or a subsidy is the likelier instrument, not a customs rate, because officials are already leaning on both regardless of a product's origin.

The Signal

The working groups' shortlist is not public yet. When it is, the country mix behind it, not the headline count of 100 products, will determine the substitution push's real bite. Goods China already dominates keep the tariff option live, and a fresh MFN hike remains a real possibility no treaty blocks. For goods now flowing through freshly zeroed British, Swiss or Australian tariff lines, that line is spoken for into the next decade, so what is left is a QCO, a PLI subsidy, or nothing. Watch which agency issues the next order: the finance ministry with a new duty, or the Bureau of Indian Standards with a new quality mark. That choice, not the length of the product list, is the real substitution policy.

Reporting basis: the CETA tariff commitments are from the UK government's own published guidance, and the Scotch whisky duty schedule is per India Briefing's reporting of the treaty's Annex 2A. The EFTA TEPA's investment pledge is per News on Air, and its tariff-line concessions are per India Briefing. The Australia ECTA's tariff terms are per News on Air. The working-group formation is per KNN India. India's FY2025-26 merchandise trade and trade-deficit figures, and the Production Linked Incentive scheme's investment, jobs and disbursement figures, are both from Ministry of Commerce and Industry statements as reported by DD News. The Bureau of Indian Standards' Quality Control Order count is from the bureau's own published list. India's China-import growth figures are per ThePrint, citing Ministry of Commerce and Industry data. India's applied and bound tariff averages are from the WTO's own tariff profile for India. India's UK import figure is per BusinessToday, citing the Commerce Ministry; the Australia and Switzerland import figures are from DGCI&S's own published trade data. The FY2025-26 total-import growth rate, and the combined UK, Australia and Switzerland import total and its comparison against China's import figure, are The Signal's calculations from those cited figures.