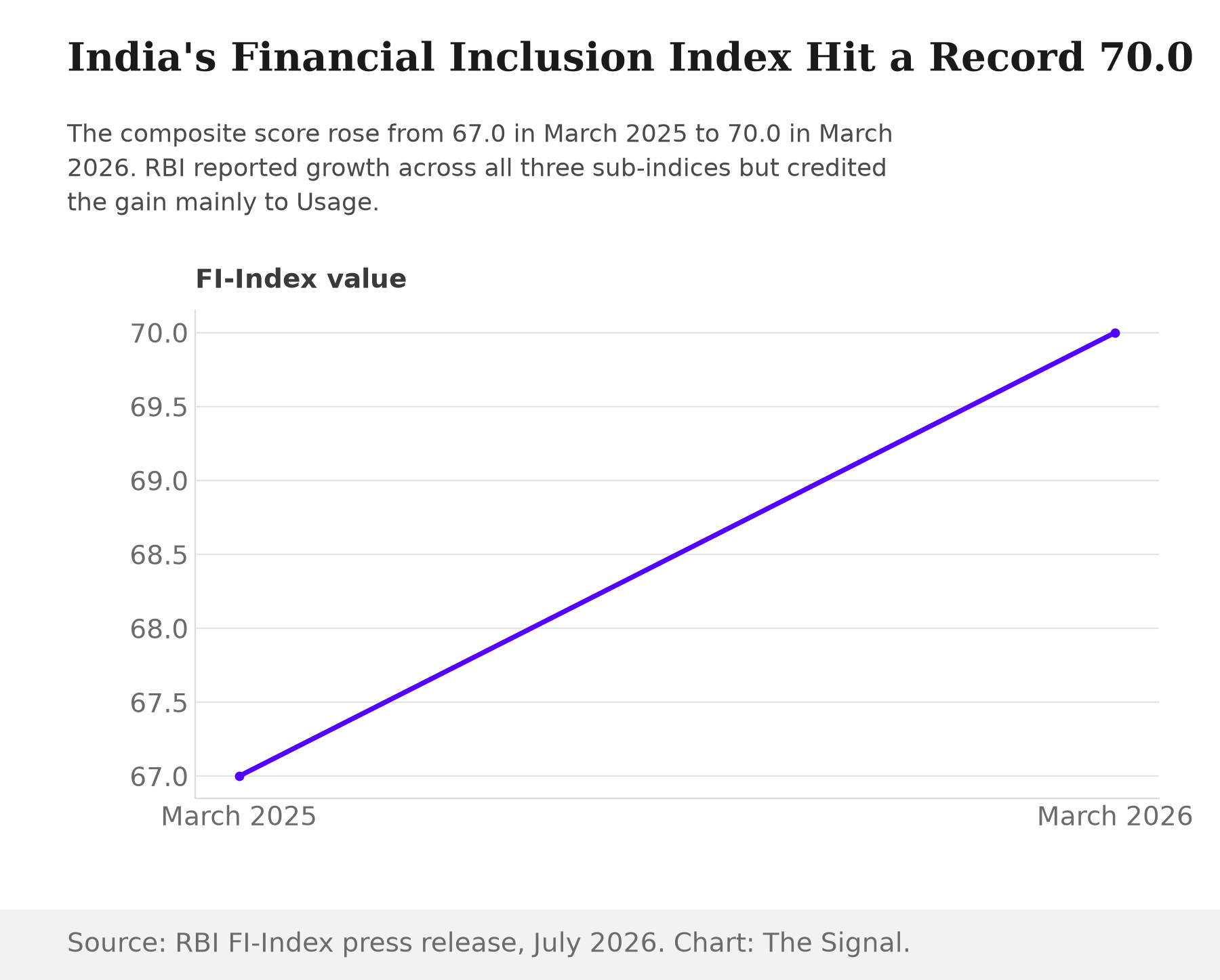

The Reserve Bank of India's Financial Inclusion Index closed the year to March 2026 at 70.0, and RBI's press release states that the value stands at 70.0 against 67.0 in March 2025, with growth witnessed across all sub-indices. Read only the headline number and the story looks straightforward: India's long push to get every adult a bank account, a working payment habit and a fair deal from the financial system is gaining ground on every front at once.

It is worth slowing down on that "every front" reading. RBI's own statement on this year's print says the improvement is mainly on account of an uptick in the Usage parameter, not a broad move across Access, Usage and Quality alike. That is a narrower sentence than the one RBI used to describe the previous year's rise.

RBI credited two legs for last year's gain. This year it credits one. Describing the year ended March 2025, when the index rose from 64.2 to 67.0, RBI said the increase was mainly driven by the Usage and Quality dimensions together. This year's statement drops Quality from that sentence and credits Usage on its own. Whatever combination of forces lifted Quality's slice for the year to March 2025, RBI's own description of the year to March 2026 does not repeat it.

What the index actually weighs

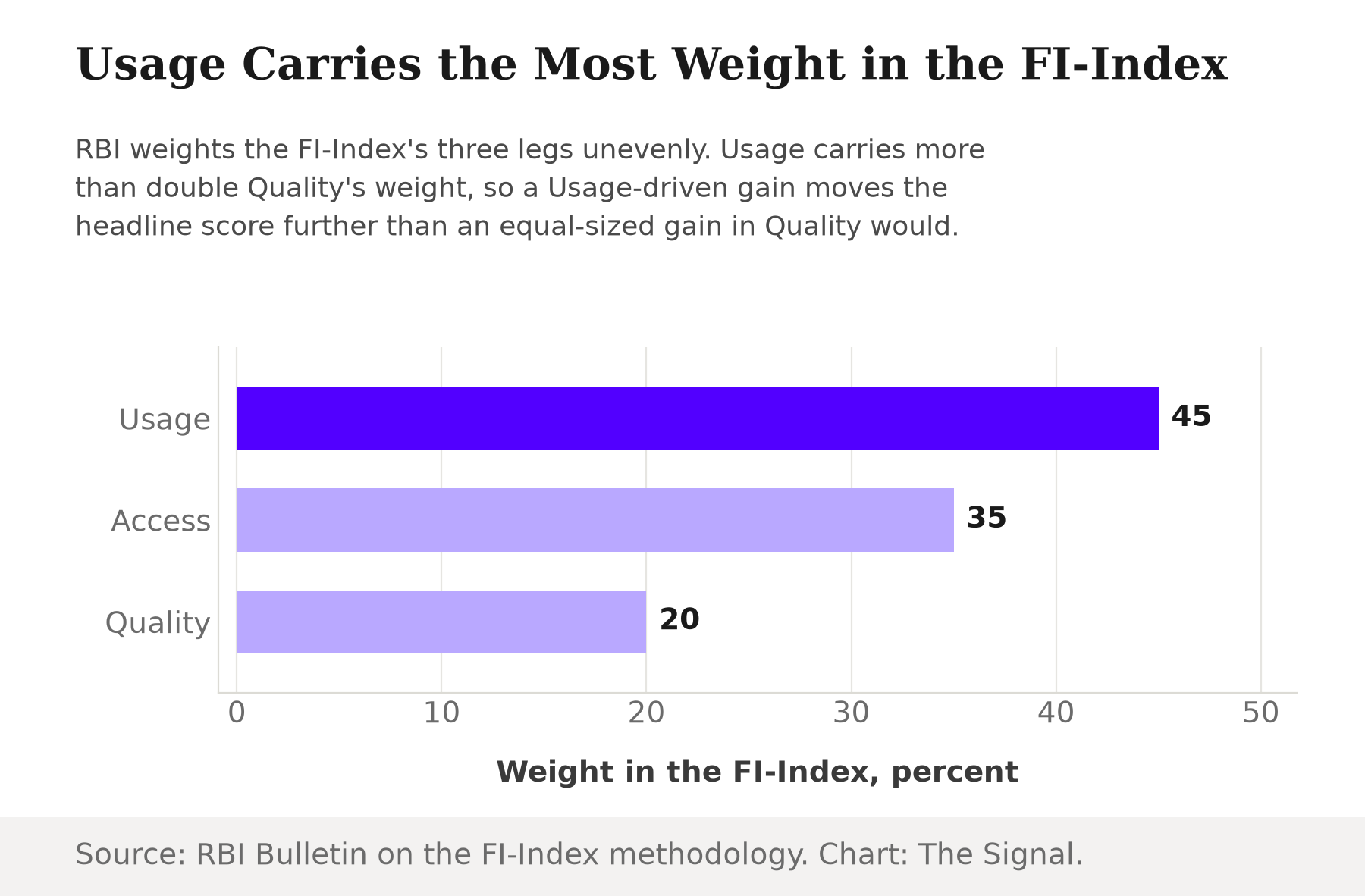

The FI-Index is not a single measurement. It is a weighted average of three sub-indices, and the weights are not equal. An RBI Bulletin article on the index's construction, published in 2021, sets Access at 35 percent, Usage at 45 percent and Quality at 20 percent of the total score. Usage carries more than double Quality's weight, so an improvement concentrated in Usage moves the headline number further than an identically sized improvement in Quality ever could. That is a mechanical fact about how the index is built, not a comment on this year's print specifically. But it does mean a record headline number driven mainly by Usage gets a structural boost that a Quality-led gain of the same size simply cannot match.

The Quality leg was already thin

Quality is built from just 19 indicators spanning financial literacy, consumer protection and inequality, and a 2025 Press Information Bureau explainer frames it explicitly around effective grievance-redressal mechanisms. It is the smallest of the three legs and, by RBI's own description, the most procedural: it measures whether people who already have accounts and use them also know their rights and can get a complaint resolved, not simply whether they show up to transact.

In December 2025, RBI's National Strategy for Financial Inclusion 2025-30 named strengthening the quality and reliability of customer protection and grievance redressal measures as one of only five strategic objectives for the next five years. An index leg the central bank itself just flagged as needing a dedicated five-year strategy is not one that should be assumed to be doing much of this year's lifting.

That mechanism is also under growing strain. RBI's own Reserve Bank Integrated Ombudsman Scheme received 1,334,244 complaints in the year to March 2025, up 13 percent from 1,175,075 the year before. A grievance-redressal system fielding a fast-rising complaint load is not obvious evidence of a Quality leg that is quietly catching up to Usage.

Access is close to done

World Bank data show account ownership among Indian adults at 89.0 percent in 2024, within striking distance of saturation. When nearly nine in ten adults already hold an account, the Access leg has less room left to move the score. The remaining growth increasingly has to come from Usage, the frequency and volume of transactions, or from Quality, the depth and fairness of the service once someone is inside the system. This year, by RBI's own account, it came from Usage.

Where the FY26 gain differs from FY25, in RBI's own words

| Fiscal year end | FI-Index value | Sub-indices RBI credited for the rise |

|---|---|---|

| March 2025 | 67.0 | Usage and Quality together |

| March 2026 | 70.0 | Usage alone |

Source: RBI statements, as reported by ThePrint for FY25 and ANI for FY26.

The honest objection

The strongest case against reading much into this is that RBI's own headline sentence for this year still says growth was witnessed across all sub-indices, meaning Quality did not fall, it simply grew less than Usage did. On that reading, singling out one phrase in a press release is overreading routine variation in language, not uncovering anything real about the underlying data.

That case has some force, but it does not explain why RBI's own comparative framing changed between the two years it is describing. A year earlier, RBI credited the rise to Usage and Quality together; this year, the equivalent statement credits Usage alone. Both statements are RBI comparing its own index to its own prior year, and the central bank chose to drop Quality from the explanation this time. Nor is the December strategy document a hedge against a hypothetical problem: RBI does not typically spend a five-year strategic objective on a leg of its own index that is already moving as fast as it needs to.

The Signal

A composite score gives a reader exactly one number to react to, and 70.0 against 67.0 will read, correctly, as progress. That single figure can hide which part is doing the work, though, and this year RBI told you which one, in its own words: Usage. The leg that is structurally the heaviest, at 45 percent of the total, is also the one the central bank says drove the gain, while the leg it just spent December naming a five-year strategic priority sits at the lowest weight of the three, 20 percent, and drew no such credit this time. Financial inclusion was never meant to be only about getting people to transact. Watch the next print for whether RBI's language widens back out to include Quality, or whether "mainly on account of Usage" becomes the standing explanation for a number that keeps climbing regardless.

Reporting basis: the FY26 FI-Index value and its "growth across all sub-indices" framing are from RBI's own press release. The specific attribution to the Usage parameter is per ANI's report of RBI's statement, and the comparable Usage-and-Quality attribution for the year to March 2025 is per ThePrint's report of RBI's FY25 statement; both are RBI's own words as relayed by a single wire report each. The index's 35/45/20 weighting comes from an RBI Bulletin article on the index's construction, published in 2021 and not revisited here. The composition and grievance-redressal framing of the Quality sub-index is per a 2025 Press Information Bureau explainer, and the naming of customer protection and grievance redressal as a five-year strategic objective is from RBI's own press release announcing the National Strategy for Financial Inclusion 2025-30. The Ombudsman Scheme complaint volumes are from RBI's Annual Report of the Ombudsman Scheme 2024-25, as reported by ThePrint's Hindi edition. Account ownership among Indian adults is World Bank Global Findex data, via the World Bank's Open Data API. The comparison of Usage's and Quality's relative weight is The Signal's calculation from the RBI Bulletin's own figures.