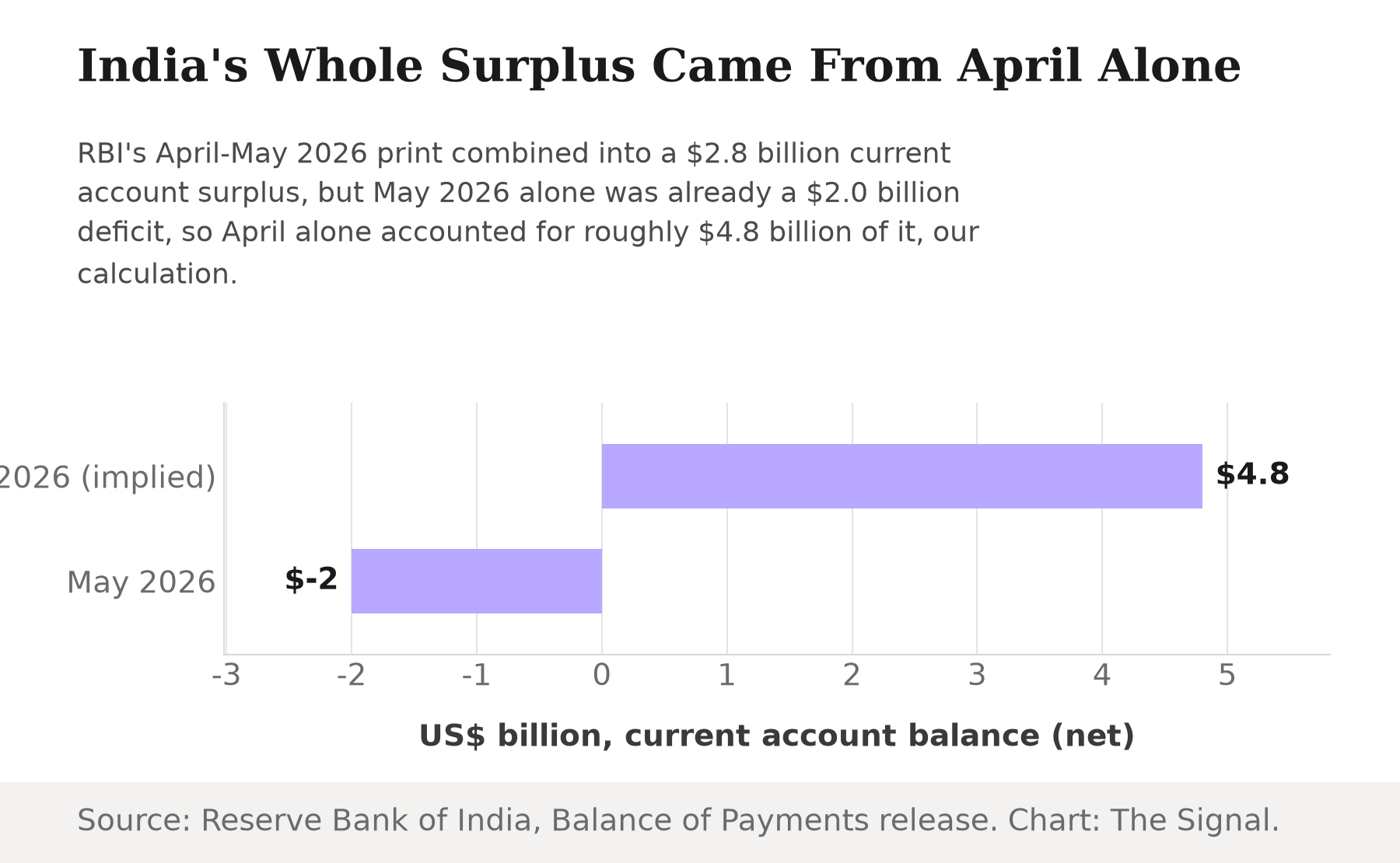

India's balance of payments looked, on the surface, like it turned a corner this spring. The Reserve Bank of India's preliminary data for April and May 2026 show the current account swinging to a $2.8 billion surplus, a reversal from a $4.1 billion deficit in the same two months of 2025. That happened even as the merchandise trade deficit widened, to $55.9 billion from $49.7 billion a year earlier. Read only the two-month total and the story writes itself: the external accounts look healthier than last year, a wider trade gap notwithstanding.

It is worth slowing down on that total. The same RBI release breaks the two months apart, and May 2026 alone was already back in deficit: $2.0 billion, against a $0.7 billion surplus in May 2025. Subtract May from the combined figure and April 2026 alone accounted for roughly $4.8 billion of the $2.8 billion two-month surplus, our calculation from the RBI release. The headline number was never a steady state. It was one very good month sitting next to one month that had already turned negative again.

What flipped between the two months

The obvious suspect is the trade gap, and over a longer horizon it is real, but it does not explain May specifically. RBI's own figures put the merchandise deficit at $27.9 billion in May 2026, barely different from the $28.0 billion implied for April, our calculation from the same RBI release. The goods gap was already wide in April. It did not spike in May. Something else in the current account did the work of flipping the total from a $4.8 billion implied surplus to a $2.0 billion deficit: the services surplus, investment income, or transfers, none of which RBI's headline release breaks out by month. The trade gap is why India needs a large services and remittance surplus in the first place, but it is not the reason that cushion came up roughly $6.8 billion short between April and May.

A trade gap that is real, just not the May story

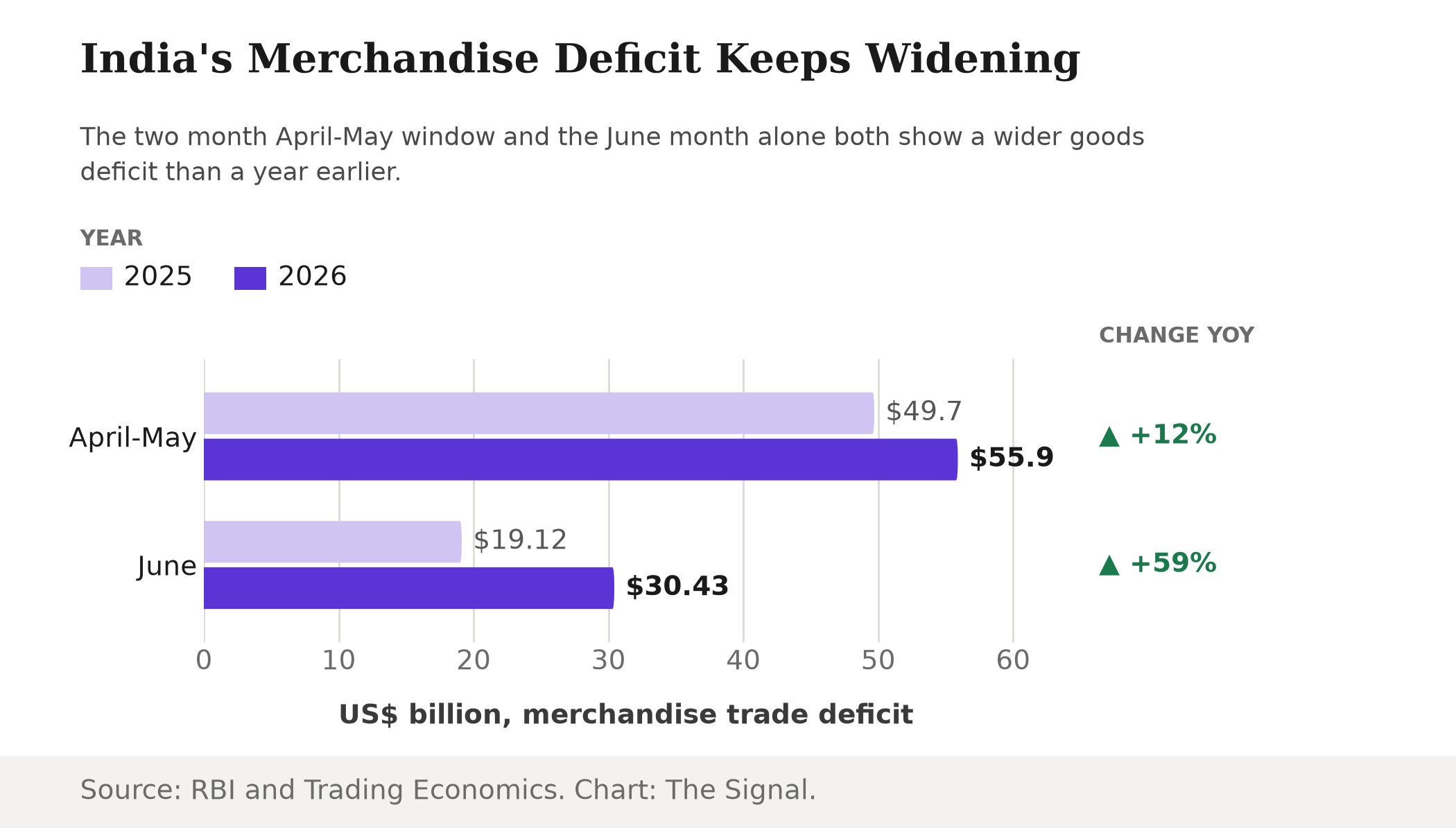

None of that means the trade gap is beside the point, only that its damage shows up on a longer clock than one month. The April-May 2026 merchandise deficit of $55.9 billion was $6.2 billion wider than the same two months of 2025. The quarter immediately before it, January-March 2026, the fourth quarter of fiscal year 2025-26, widened by even more: Trading Economics reports, citing RBI data, that the goods deficit reached $83.4 billion that quarter, up from $59.3 billion a year earlier, as the current account surplus itself narrowed to $7.1 billion from $13.7 billion. And the first full month with data released after May, June 2026, kept the pattern going: Trading Economics reports, citing Ministry of Commerce trade data, that the merchandise deficit hit $30.43 billion, the largest for that month on record, up from $19.12 billion in June 2025, as imports surged 31 percent to a record $70.84 billion while exports rose a softer 15.5 percent. Every period measured since April 2026, the two-month window, the quarter before it, and the month after it, points the same way: wider, not narrower.

The cushion that is supposed to absorb it

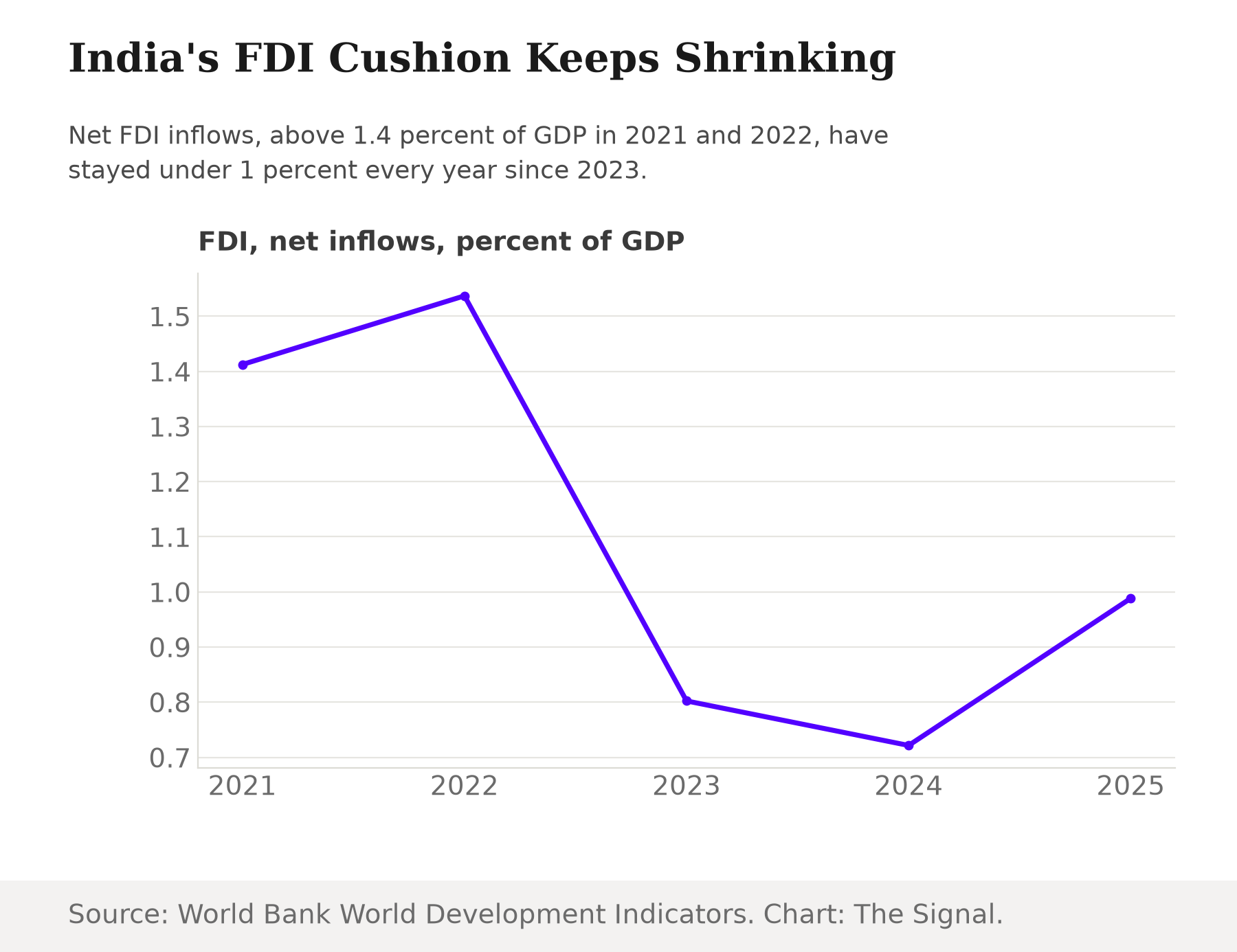

A current account that swings between small surpluses and small deficits from month to month is normal for an economy running a persistent goods deficit. What keeps the overall account close to balance is everything else, chiefly remittances from Indians working abroad, net services exports, and capital inflows that help finance whatever gap remains. World Bank data show personal remittances into India rose to $150.7 billion in 2025 from $137.7 billion in 2024, still the country's largest non-trade inflow. The Economic Survey 2025-26 puts India's standing among remittance-receiving countries in explicit terms: it remained the world's largest recipient, with inflows of $135.4 billion in FY2024-25. But the capital side of that cushion has been thinning for longer. Net foreign direct investment, the financing India has traditionally relied on to fund any residual current account gap, fell to 0.99 percent of GDP in 2025, down from 1.54 percent in 2022 and 1.41 percent in 2021, and has stayed under 1 percent of GDP in every year since 2023. Remittances are still growing. The FDI leg of the cushion is not.

The annual data has not caught up

None of this shows up yet in the number that gets the most attention: the full-year current account deficit as a share of GDP. World Bank data put India's current account deficit at just 0.42 percent of GDP in calendar 2025, down from 0.85 percent in 2024 and a peak of 2.43 percent in 2022, a genuine multi-year narrowing. But that figure is for calendar year 2025, a full year that closed before the April-May 2026 print existed, let alone June's record goods gap. It cannot show a reversal that began in May 2026. The annual trend and the monthly trend are not contradicting each other. They are describing different clocks, and the faster one just changed direction.

The honest objection

The strongest case against reading anything into one month is that RBI's own numbers invite caution. The May 2026 current account figure is marked preliminary, and the year-ago comparison it sits against is marked partially revised, meaning even the baseline has already moved once and May's number could move again. A single deficit month inside an otherwise-surplus two-month window, in an economy whose annual current account gap has narrowed for three straight years running, is thin evidence of a structural turn. Monthly balance-of-payments data is noisy for reasons that have nothing to do with trade: a large one-off dividend repatriation or bond redemption can move a month's figure without saying anything about the trend beneath it.

That case would carry more weight if the trade evidence pointed the other way. It does not. June 2026's merchandise deficit was not just wider than a year earlier, it was the largest June on record, arriving after a quarter that had already produced the sharpest widening in the data available. The countervailing evidence has kept building in the two months since May's current account print, not receding. Noise explains one bad month. It does not explain three periods in a row moving in the same direction.

The Signal

The two-month total was never wrong, exactly. It was carrying an April that had already stopped repeating itself by the time it was published. The real test is not the number already printed. It is the one that has not printed yet: whether India's current account for June and July, sitting behind a goods deficit already running at a record pace, comes back to surplus or extends May's reversal. If it extends, the story stops being a wide but stable trade gap and becomes a shrinking cushion meeting a widening hole at the same time, with the FDI leg of that cushion thinner than it has been in years. A two-month average can hide a one-month reversal for exactly as long as nobody checks the second month.

Reporting basis: the April-May 2026 and May 2026 current account and merchandise trade figures are from the Reserve Bank of India's preliminary Balance of Payments press release. The January-March 2026 quarterly current account and goods-deficit figures are from Trading Economics, compiling Reserve Bank of India Balance of Payments data. The June 2026 merchandise trade deficit is from Trading Economics, compiling Ministry of Commerce trade data. The calendar-year current account deficit as a share of GDP is from the World Bank's World Development Indicators, personal remittances from the same World Bank series, and net foreign direct investment inflows from the World Bank's FDI series. The implied April 2026 current account balance and merchandise deficit, and the April-to-May change described in this piece, are The Signal's calculations from the Reserve Bank of India's release.