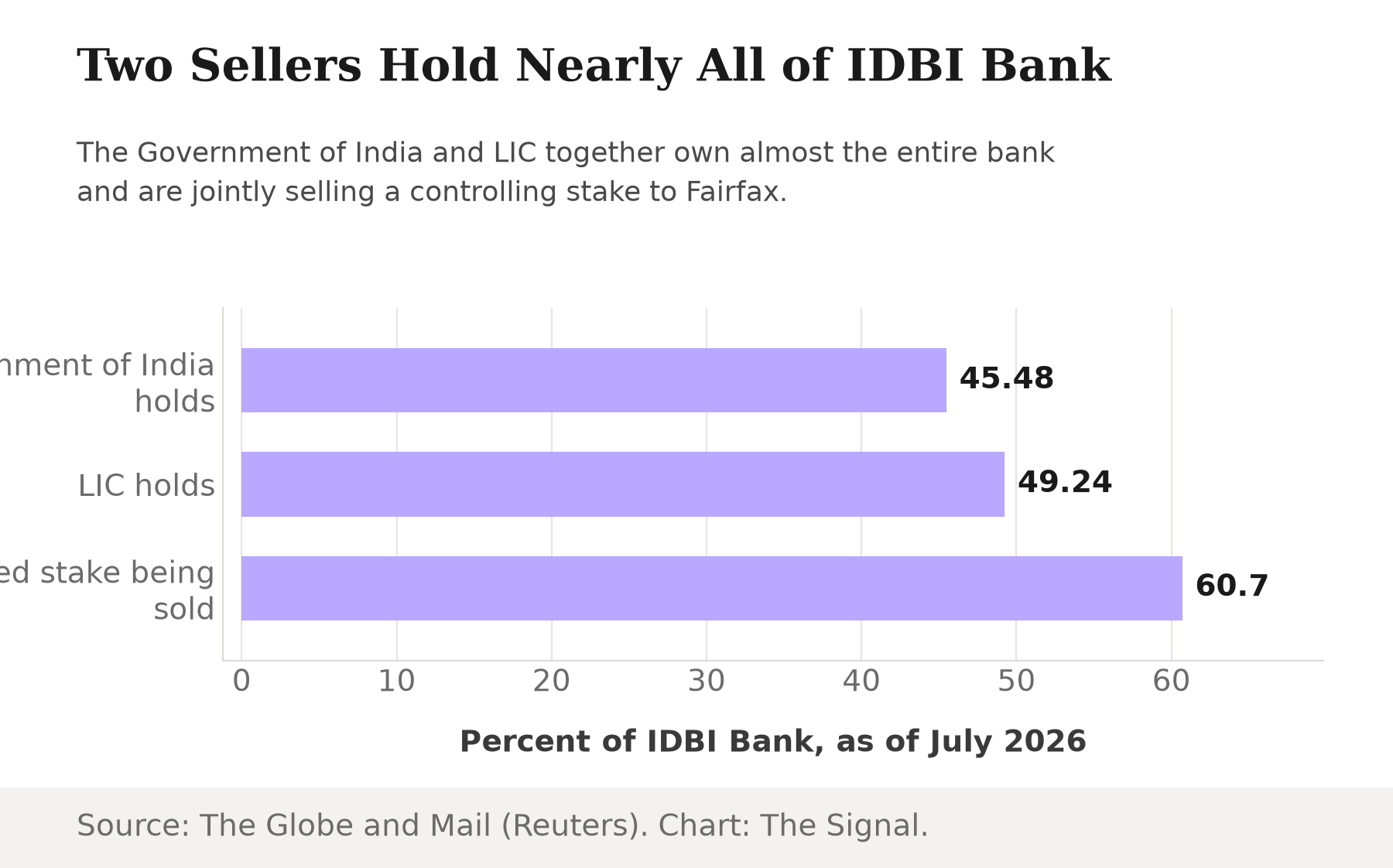

Fairfax Financial has raised its offer for IDBI Bank to ₹81 a share, up from ₹75 in 2025, putting the total deal at around $5.5 billion. The sellers are the Government of India and Life Insurance Corporation, which together are offloading a combined 60.7 percent of the bank: the government holds 45.48 percent, LIC holds 49.24 percent, and both are cashing out a controlling slice. As of July 14, 2026, the revised proposal was reportedly close to being accepted, though final approval from the Union Cabinet and the RBI is still required. Read at that level, this is a straightforward story: a Canadian insurer is paying a record price to take control of a bank still majority-owned by the Indian state and its largest insurer.

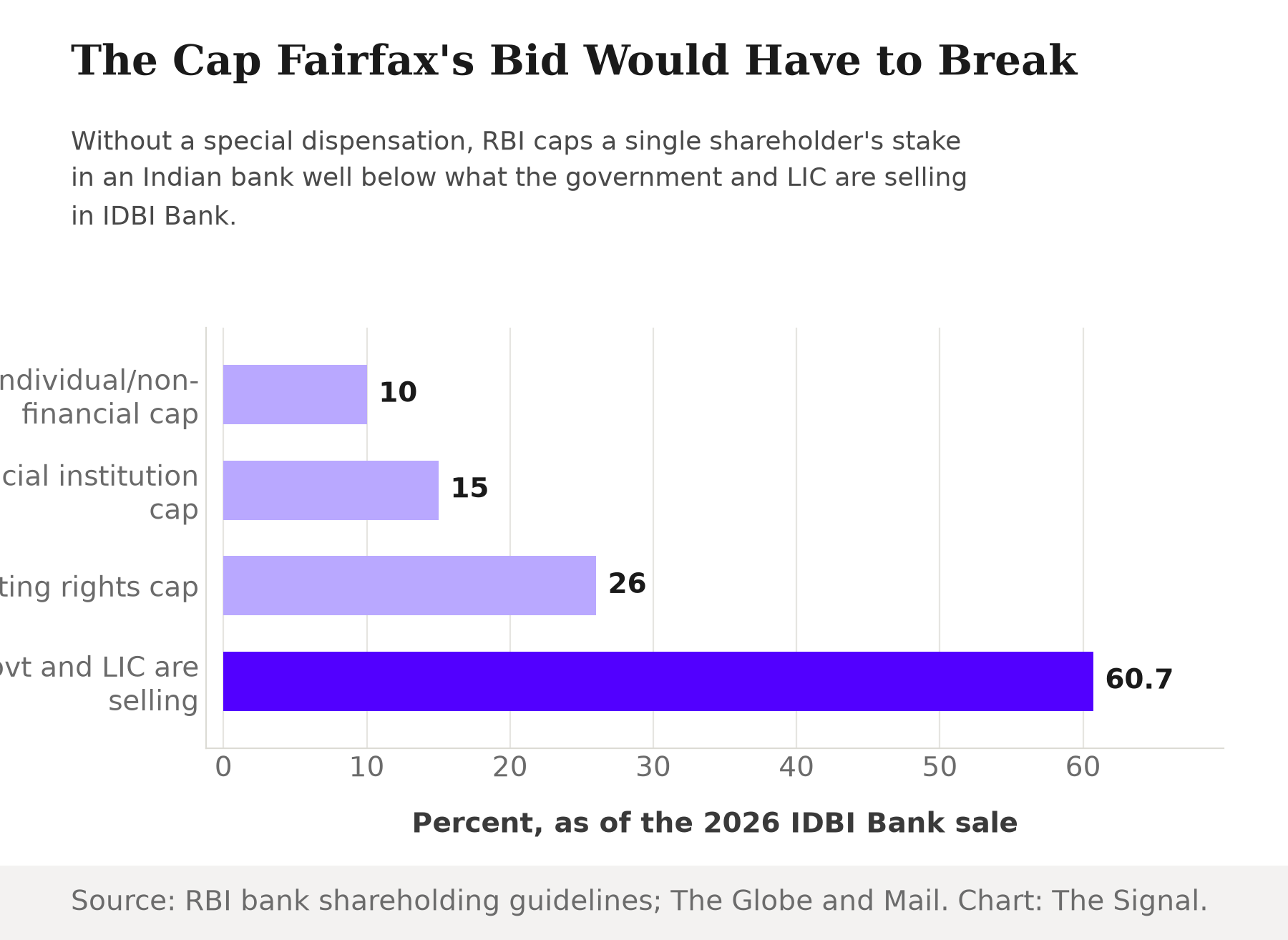

It is worth slowing down on that framing. The headline number is the price. What actually decides the deal is the rule standing in front of it. Any acquisition likely to result in "major shareholding," defined as 5 percent or more of an Indian bank's paid-up capital or voting rights, requires the RBI's prior approval. That approval is not a formality against a blank rulebook. Without a special dispensation, RBI's own guidelines cap a non-promoter shareholder at 10 percent of a bank's capital if it is an individual or non-financial entity, or 15 percent if it is a financial institution, a public sector undertaking or the government. The same guidelines require a promoter to dilute to 26 percent within 15 years, and bar any shareholder, in any category, from exercising voting rights above 26 percent. Whichever bracket a Canadian insurance and investment holding company falls into, none of those ceilings gets anywhere near a majority stake. A 60.7 percent purchase is more than double the hard voting-rights limit and roughly four times the ceiling written for financial institutions.

Fairfax is bidding for a stake more than twice the RBI's voting-rights ceiling for any single shareholder.

IDBI Bank has already tested this rule once

This would not be the first time IDBI Bank's ownership has run past the standard ceiling. The RBI categorised IDBI Bank as a "Private Sector Bank" for regulatory purposes with effect from January 21, 2019, after LIC had acquired 51 percent of its paid-up equity. LIC's 51 percent stake was, on its own, already far beyond the 26 percent ceiling that otherwise applies to any single shareholder's voting rights. That earlier restructuring is the precedent the current sale sits on top of: IDBI Bank has already been the vehicle for one ownership arrangement well outside the normal cap, engineered specifically to bring in a controlling shareholder. Fairfax's bid asks the RBI for a second exception on the same bank, at a larger scale, not an entirely new kind of one.

The condition already attached to the exception

The clearest evidence that this is a negotiated exception, not a waiver, is what Fairfax has already agreed to give up. Fairfax holds around 40 percent of CSB Bank and has committed to fully divest that stake if it wins IDBI Bank, because RBI norms do not permit a single promoter to hold two banking licences. That commitment is the shape of things to come for whatever dispensation the RBI ultimately signs off on: permission to exceed the ownership cap in one bank, paired with a hard requirement to exit any position in another. The price of admission to majority control at IDBI Bank is giving up control anywhere else in Indian banking.

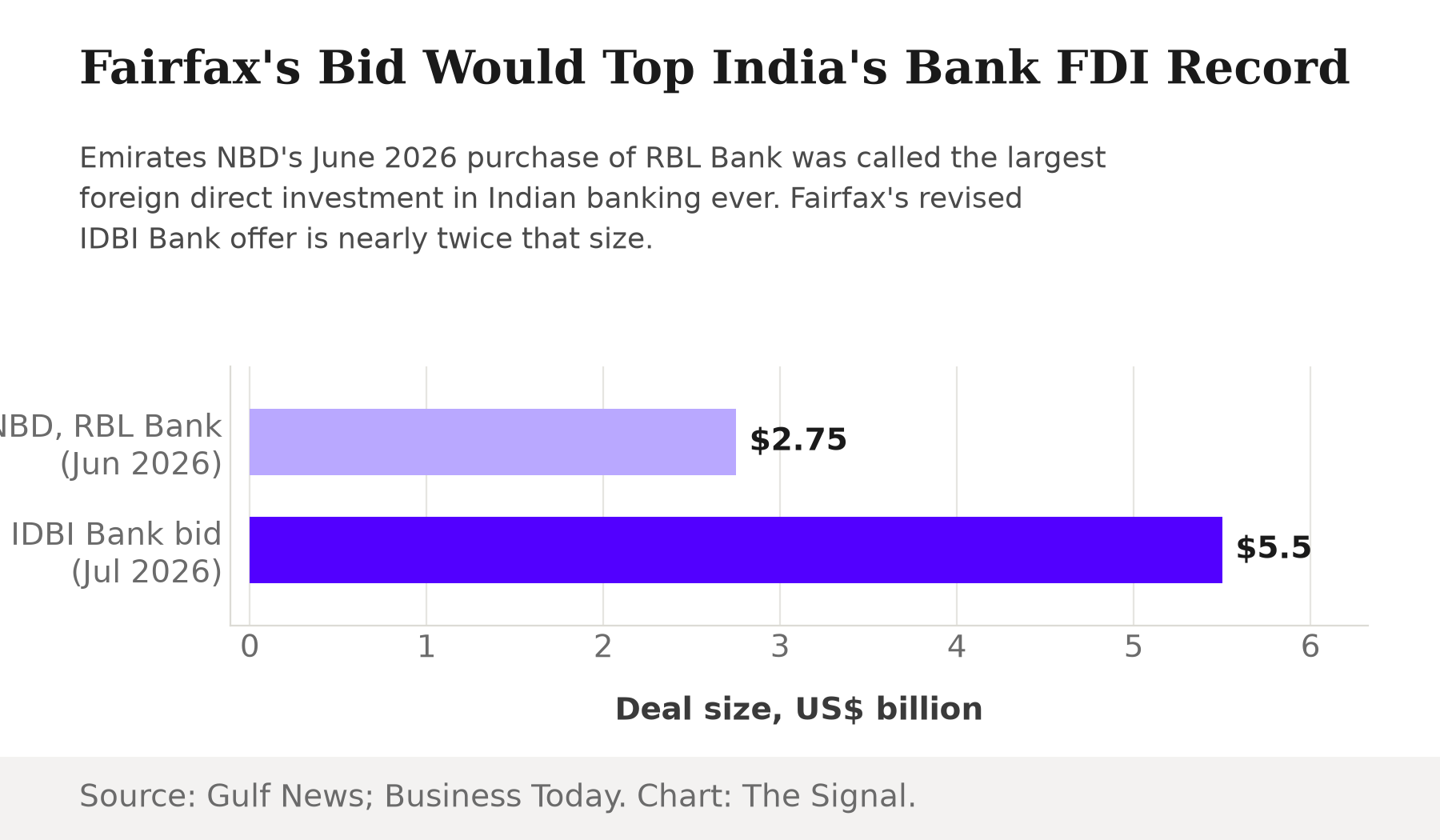

The size is real, even if the record framing is premature

Set against India's other recent foreign banking deal, Fairfax's bid is genuinely large. Emirates NBD completed a $2.75 billion acquisition of a 60 percent stake in RBL Bank on June 18, 2026, which it called the largest foreign direct investment in the Indian banking sector to date. Fairfax's $5.5 billion bid is nearly double that figure. But that comparison should be read carefully: Emirates NBD's deal has closed, while Fairfax's is still one Cabinet meeting and one RBI approval away from being final. The size of the number is not in question. Whether it becomes the new record is a decision two regulators have not yet made.

The honest objection

The strongest case for treating this as routine is that the RBI's approval requirement was built precisely for cases like this one. The rule is not a ban, it is a gate: any acquisition of major shareholding needs prior approval, which means the regulator retains full discretion to grant one on terms it sets, case by case. IDBI Bank's own history under LIC shows the RBI is willing to approve concentrated ownership in a bank it judges fit for it, and a divestment condition like the one Fairfax has already accepted on CSB Bank shows the RBI is not simply waving deals through. On this view, there is no rule being broken at all, only a process working as designed.

That case holds up to a point, but it understates what is actually being asked. A gate that requires case-by-case approval for anything above 5 percent is one thing. A request to hold the 60.7 percent stake on the table, more than double the voting-rights ceiling that applies even with approval, is a different kind of decision: not "may this shareholder cross the ordinary line," but "should the ordinary line apply to this shareholder at all." The RBI has answered that question once before, for this exact bank. It has not yet answered it for a foreign financial holding company with no other Indian government stake to fall back on.

The Signal

Forget the price tag on this deal. Watch whatever conditions the RBI attaches when, and if, it signs off: how long Fairfax is given to exit CSB Bank, what voting or board restrictions come with the stake, and whether the approval is written narrowly enough that it cannot be cited as precedent by the next foreign bidder eyeing a public-sector bank. Every other PSU lender still on the government's list is a smaller, less scrutinised version of the same negotiation. Whoever comes next will read the fine print of this deal before they read the price.

Reporting basis: the RBI's ownership-cap framework and IDBI Bank's 2019 reclassification are drawn directly from Reserve Bank of India primary documents, its Master Direction on bank-share acquisitions, its shareholding guidelines, and its 2019 press release. The current bid price and deal size are per Business Today's reporting; the government and LIC shareholding figures are per The Globe and Mail's reporting of Reuters wire copy; the pending Cabinet and RBI approval status is per Outlook Business; the CSB Bank divestment commitment is per Business Today; and the Emirates NBD-RBL Bank comparison is per Gulf News. The comparison between the RBI's ownership ceilings and the stake on the table in IDBI Bank is The Signal's own reading of those RBI figures against the reported deal terms.