On July 13, 2026, Aditya Birla Renewables Limited, a subsidiary of Grasim Industries, signed a Share Purchase Agreement to acquire Solenergi Power Private Limited from Shell Overseas Investment B.V., a wholly owned subsidiary of Shell plc. Solenergi is the Mauritius-based holding company for Sprng Energy, and Aditya Birla is buying 100 percent of it, as ANI reported, citing the companies' stock exchange filing. The transaction is valued at an enterprise value of Rs 17,200 crore, around $1.8 billion, Business Today reports. Sprng Energy's portfolio runs to 5.0 gigawatts-peak, comprising 3.3 GWp of operating assets and 1.7 GWp under contract, RTTNews reports. Shell says the sale fits its strategy to recycle capital into an asset-backed trading approach while targeting improved returns through 2030, citing Shell's statement.

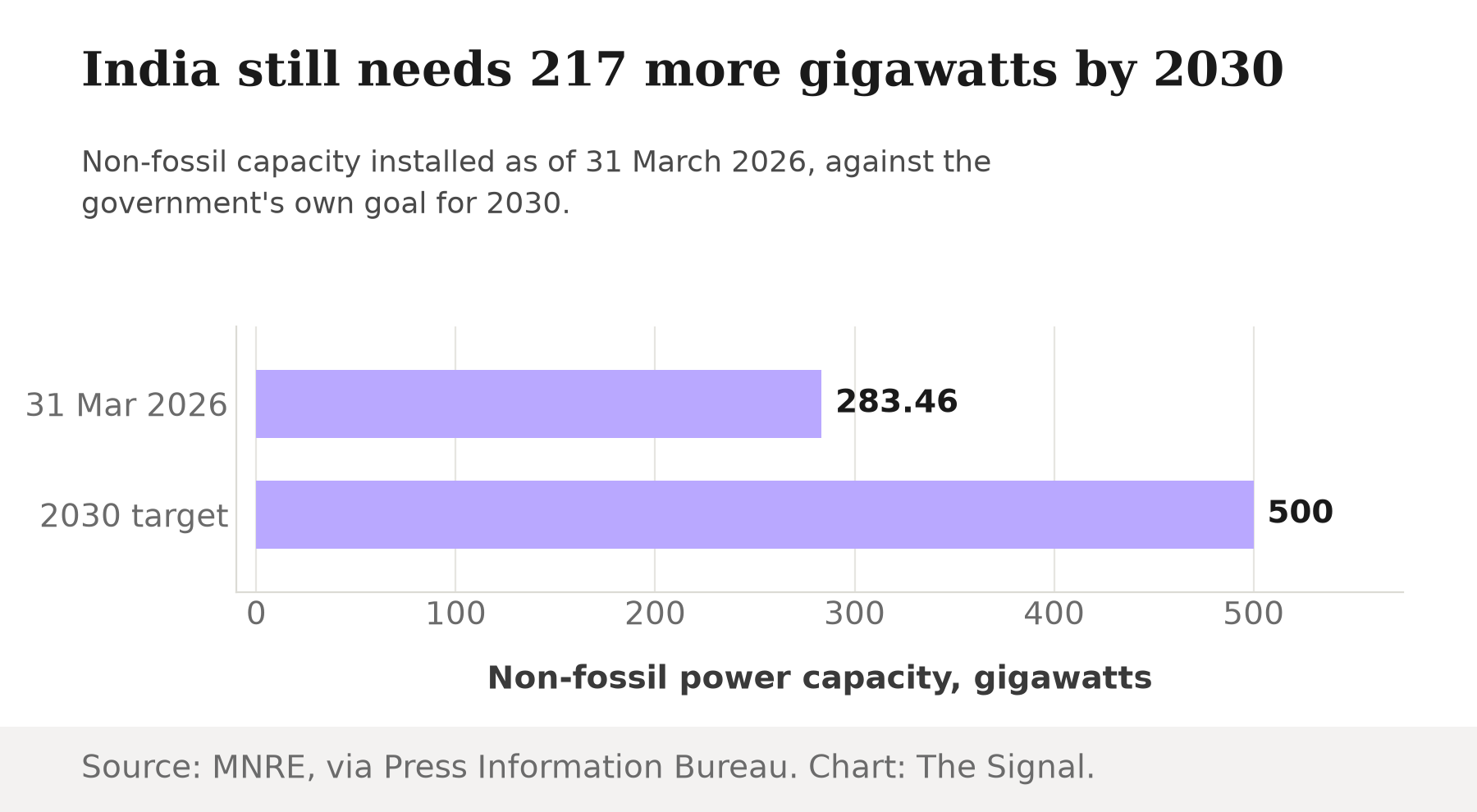

Read plainly, this looks like more fuel for a fire that is already burning. India's cumulative installed renewable capacity had reached 288,589 megawatts, about 288.6 gigawatts, as on June 30, 2026, the Ministry of New and Renewable Energy's own data show. Non-fossil capacity stood at 283.46 gigawatts as on March 31, 2026, against a government target of 500 gigawatts of non-fossil capacity by 2030, per a Press Information Bureau release. A large asset changing hands reads, at first glance, like one more sign that capital keeps arriving to build the grid out.

It is worth slowing down on that. Shell is not simply monetizing a winning bet. Its own numbers say it is retreating, and they said so before the Sprng announcement did.

The math behind the exit

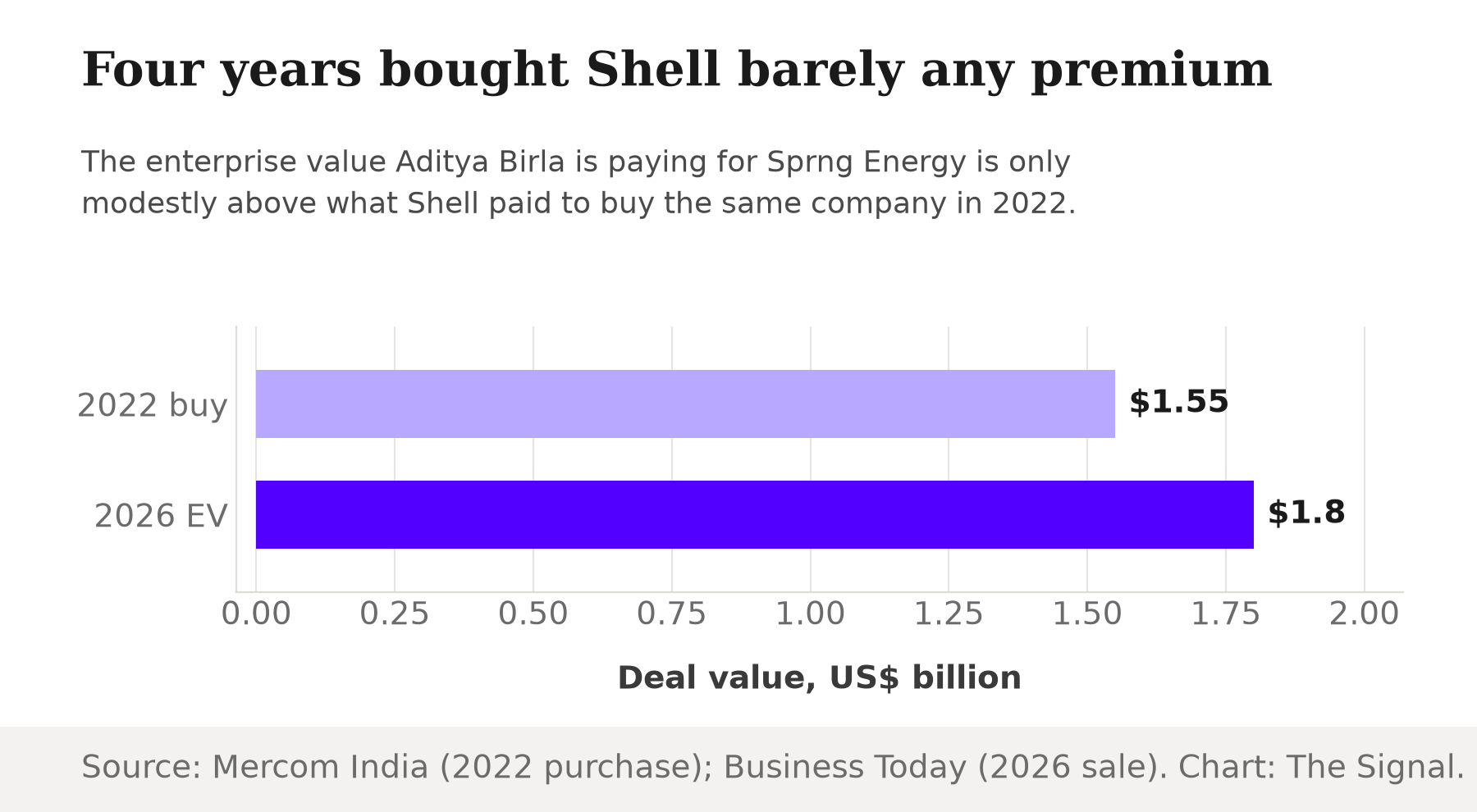

Shell bought the same company, then called Solenergi Power, from Actis Solenergi Limited for $1.55 billion in April 2022, Mercom India reported. Four years and three months later, it is selling that same holding company for an enterprise value of about $1.8 billion, per Business Today's report of the current deal. Our calculation: that is a nominal gain of roughly 16 percent. The comparison does not account for whatever capital Shell put in or took out along the way, and it comes on a business whose operating and contracted portfolio grew over the same period. These are not identical measures, a 2022 purchase price against a 2026 enterprise value, but they are the closest public comparison available, and the gap between them is thin for a four-year hold.

That thin margin fits the reason Shell itself gave: recycling capital into an asset-backed trading approach, chasing improved returns through 2030, rather than continuing to hold and operate generation assets in India.

Shell was already leaving, everywhere

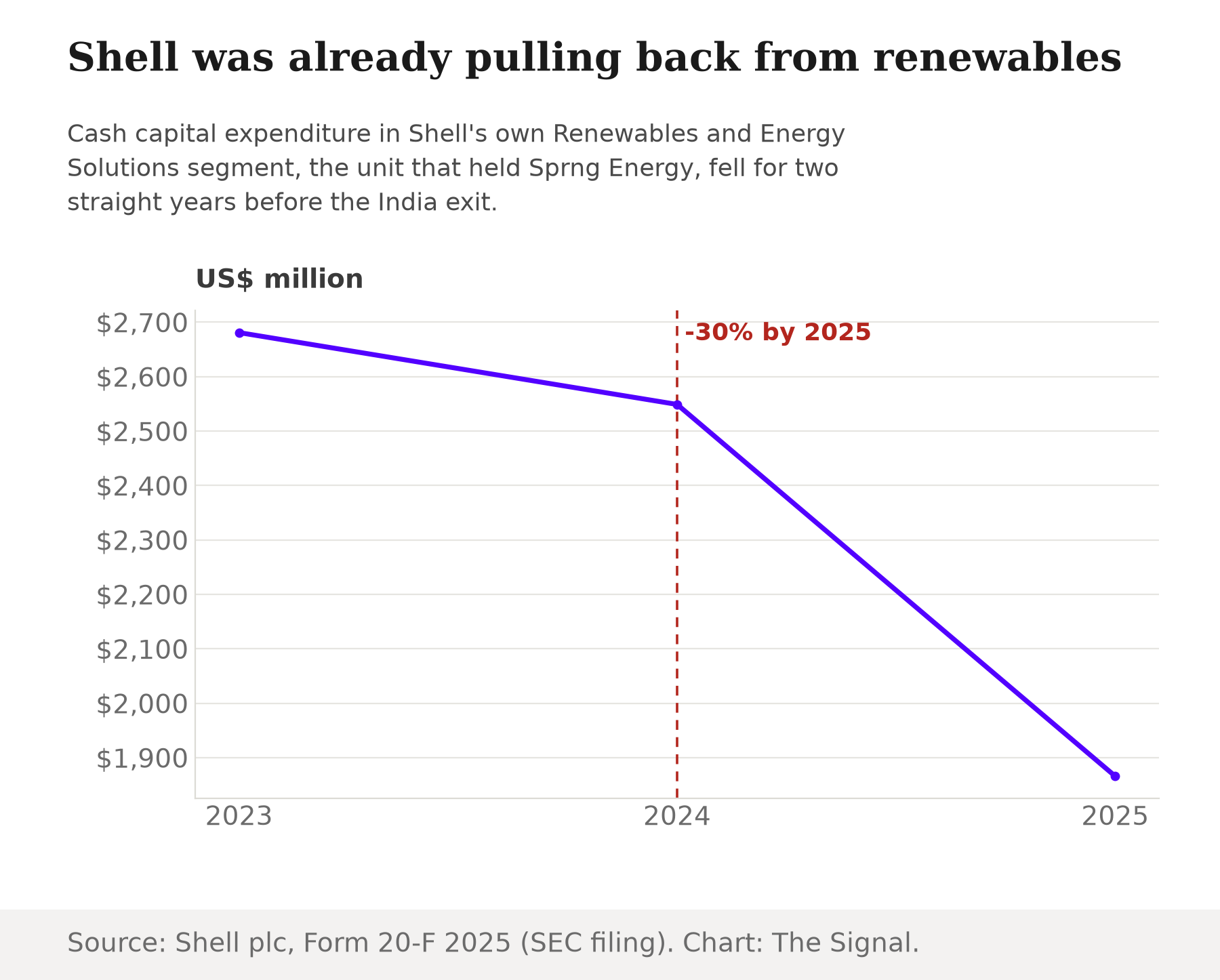

The India sale is not an isolated retreat. Shell's Renewables and Energy Solutions segment, the global unit that housed Sprng Energy, cut its own cash capital expenditure from $2,681 million in 2023 to $2,549 million in 2024 to $1,866 million in 2025, a two-year decline of roughly 30 percent, Shell's Form 20-F annual report filed with the U.S. Securities and Exchange Commission shows.

A segment spending 30 percent less on renewables worldwide was never going to keep bankrolling a 5-gigawatt Indian platform indefinitely. The Sprng sale reads less like an opportunistic cash-out and more like the India installment of a retreat Shell had already logged on its own balance sheet.

Who is actually building the grid

The buyer matters as much as the seller's math. The deal hands Aditya Birla Renewables, a Grasim Industries subsidiary, 100 percent of Solenergi Power directly from a Shell subsidiary, no other bidder or intermediate owner involved. It joins a short list of Indian conglomerates that already dominate utility-scale renewable ownership. Adani Green Energy calls itself India's largest pure-play renewable energy company. It closed the 2025-26 financial year on March 31, 2026 with 19.3 gigawatts of total operational capacity, having added just over 5 gigawatts in fiscal 2025-26 alone, the company's own newsroom release states.

A single Shell divestment barely dents India's renewable map, but it does shift whose balance sheet carries it.

| Entity | Capacity | Metric | As of |

|---|---|---|---|

| Sprng Energy (sold to Aditya Birla) | 5.0 | GWp: 3.3 GWp operating, 1.7 GWp under contract | 13 Jul 2026 |

| Adani Green Energy | 19.3 | GW, total operational | 31 Mar 2026 |

| India, cumulative installed renewable capacity | 288.6 | GW | 30 Jun 2026 |

Source: RTTNews, citing Shell's statement; Adani Green Energy newsroom; Ministry of New and Renewable Energy.

Sprng's 5.0 gigawatts-peak is a small slice, about 1.7 percent, of India's 288.6 gigawatts of cumulative installed renewable capacity as on June 30, 2026. But scale was never the point. What matters is who takes over: the slice moves from a global energy major with decades of operating experience to a domestic conglomerate entering a business Adani Green already runs at nearly four times Sprng's size. Each time a foreign operator exits an Indian renewable platform, the replacement keeps coming from the same short list of Indian industrial houses rather than a wider pool of global capital taking direct operating stakes.

The gap that still needs filling

None of this is happening in a vacuum. India's own target is 500 gigawatts of non-fossil capacity by 2030; as on March 31, 2026 it had installed 283.46 gigawatts, leaving 217 gigawatts still to build in under four years, per the Press Information Bureau's figures.

Filling that gap needs continuous capital and continuous operating expertise. The operators exiting are global majors retreating for reasons that reach beyond any one country, and the operators entering are the same two or three Indian conglomerates. That means the balance sheets carrying the execution risk are shrinking as the 2030 deadline approaches, the opposite of what a maturing market would normally produce.

The honest objection

The strongest case against reading this as a problem is that Indian conglomerates may simply be better placed to hit the 2030 target than a foreign major ever was. Aditya Birla and Adani Green know India's land acquisition process, transmission queues, and state electricity distribution companies from the inside, in a way an overseas-headquartered Shell subsidiary never could. Consolidation into domestic hands could mean faster execution, not slower, and foreign capital can still fund the build through debt, green bonds, or portfolio stakes without needing to be the operator of record. That case is real, and it may well be right on financing.

That case addresses cost, not resilience. Shell's own capital numbers show a specialized global renewables operator pulling back for reasons that have nothing to do with India specifically, and the immediate replacement narrows the field of operators rather than widening it. A grid that depends on two or three domestic balance sheets to add 217 more gigawatts of non-fossil capacity by 2030 carries a different risk profile than one built by a dozen competing operators, foreign and domestic alike, even if the near-term construction pace looks identical either way.

The Signal

Aditya Birla's purchase reads, on its face, like proof that India's clean-power story is strong enough to keep pulling in big capital. Look instead at what Shell actually got for four years of ownership, and at what its own global spending did in the meantime, and the more accurate read is that one kind of owner is leaving and only one kind of owner is arriving to replace it. Watch where the next large foreign renewable divestment in India lands. If it goes anywhere other than an existing Indian conglomerate's balance sheet, the ownership base is genuinely diversifying. If it does not, India will reach its 2030 target with a shorter list of hands actually running the grid.

Reporting basis: the deal value and Shell's stated rationale for the sale are per Business Today's and RTTNews' reporting of the transaction announcement, the latter citing Shell's own statement; the deal structure is per ANI's report of the companies' stock exchange filing. Shell's 2022 acquisition price is per Mercom India's report of the original agreement with Actis Solenergi. Adani Green Energy's operational capacity is from the company's own newsroom release, a corporate disclosure rather than independent verification of that figure. India's cumulative renewable and non-fossil capacity figures are from the Ministry of New and Renewable Energy's Physical Progress data and a Press Information Bureau release, respectively. Shell's segment capital expenditure is from its Form 20-F annual report filed with the U.S. Securities and Exchange Commission. The nominal gain on the 2022-to-2026 sale, Sprng's share of India's total installed renewable capacity, the multiple by which Adani Green's operational capacity exceeds Sprng's, and the gigawatts still needed to reach the 2030 target are The Signal's own calculations from those figures.