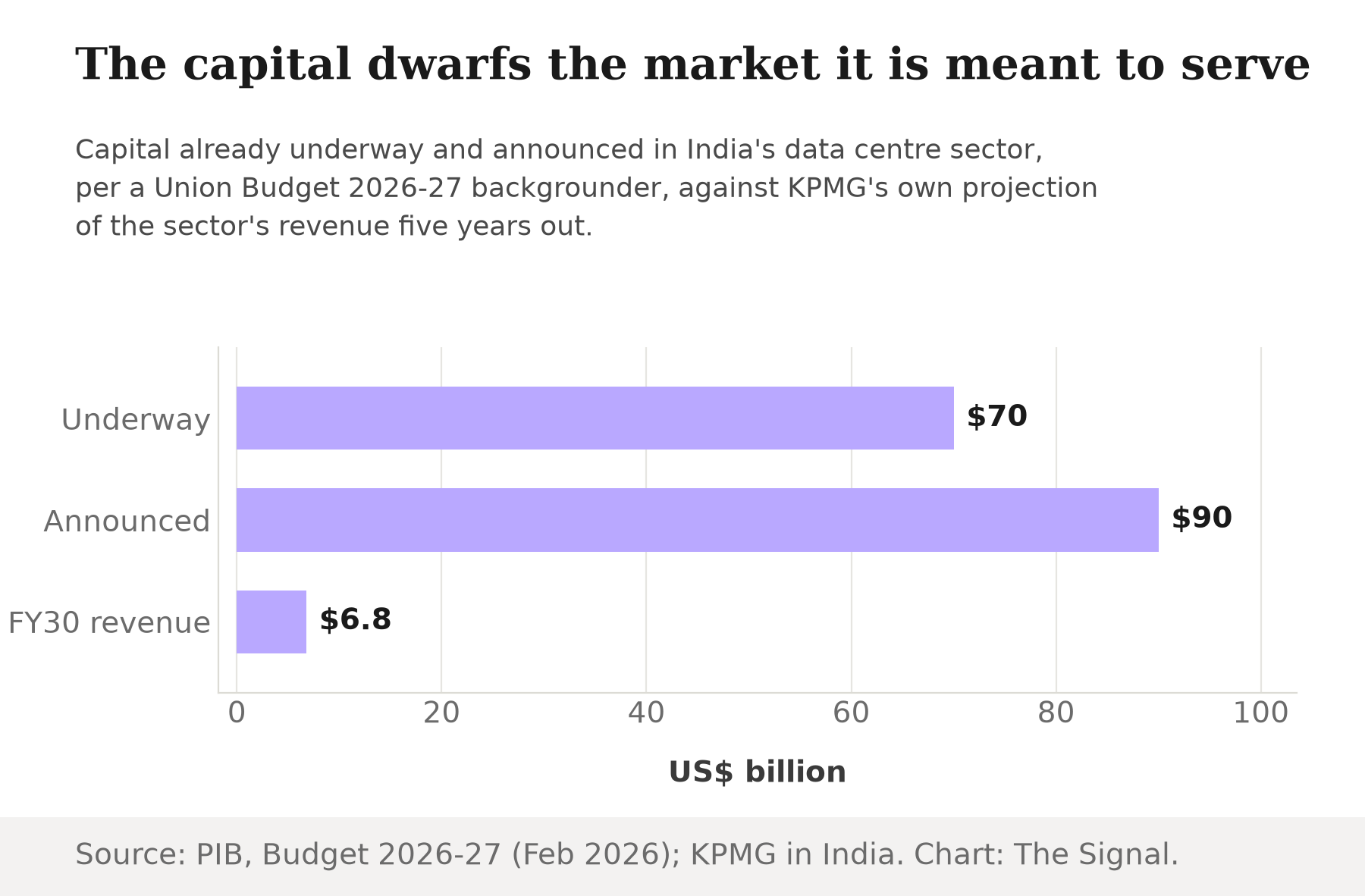

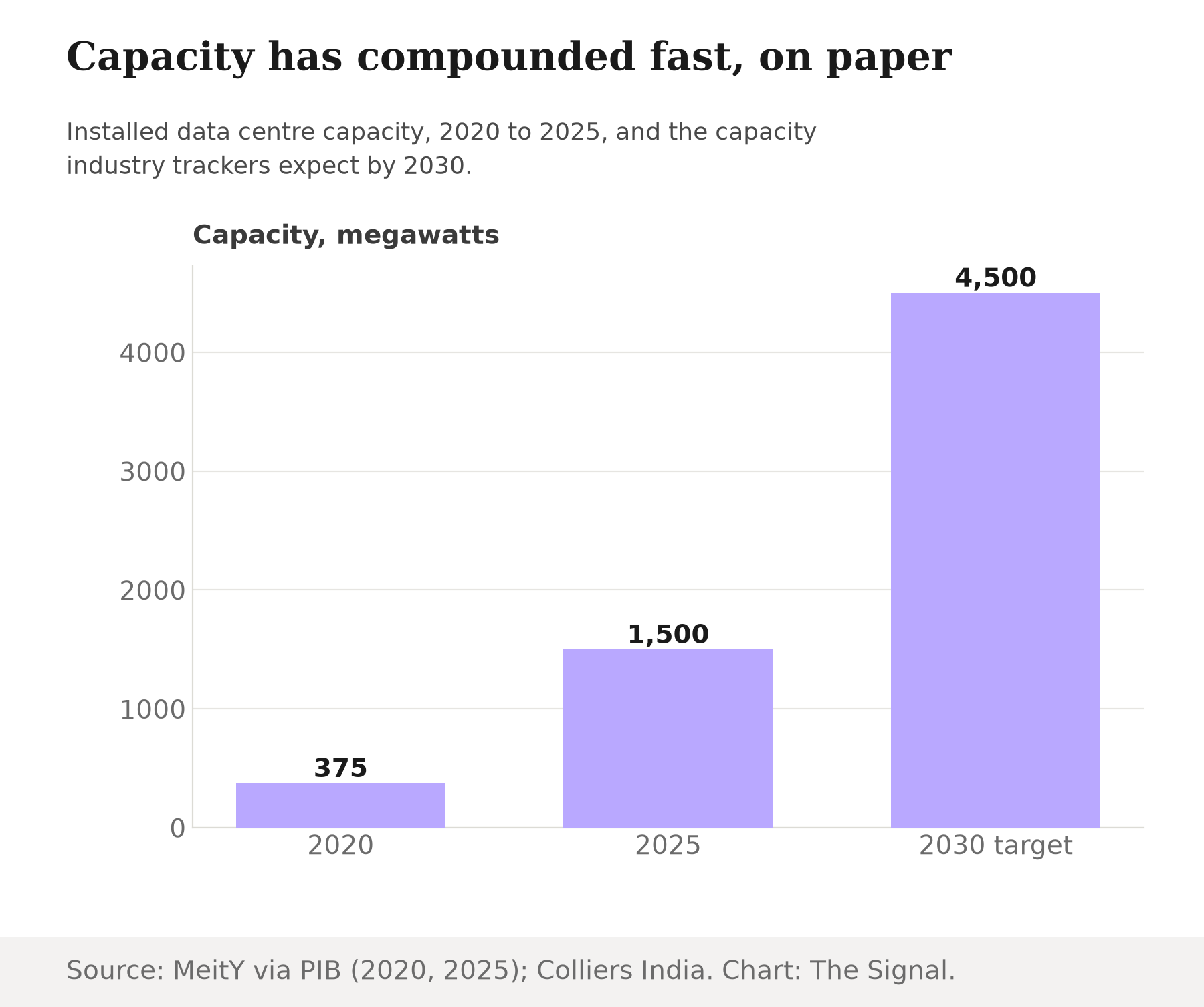

In its backgrounder for Budget 2026-27, the Press Information Bureau states that nearly USD 70 billion of investment is already underway in India's data centre sector, with an additional USD 90 billion in announced projects. The capacity data backs up the scale of that number: the Ministry of Electronics and Information Technology reports, via PIB, that data centre capacity grew from 375 MW in 2020 to more than 1,500 MW by 2025, a fourfold rise in five years. Global capital keeps arriving to match it: CNBC reports that Amazon has added a fresh USD 13 billion pledge for AI and cloud infrastructure in India, taking its cumulative commitment to USD 48 billion, up from what was already about USD 35 billion. That is one hyperscaler's running tab, added to in a single announcement in June 2026, layered on top of the national totals above.

The industry case for why the money is rushing in rests on a real gap. A KPMG in India sector analysis notes that although India produces about one fifth of global data, it hosts only about 2-3 per cent of global data centre capacity. Read that way, the capital is closing an obvious shortfall, not chasing a mirage.

It is worth slowing down on that framing. The same KPMG analysis does not model this gap closing into a large market soon: it puts India's data centre sector revenue at about USD 1.7 billion in FY26, rising to about USD 6.8 billion by FY30, with India's share of global capacity moving only from 2-3 per cent to about 5 per cent over that span. Against a market that size, the capital already logged is not a modest overweight: the USD 70 billion already underway alone runs to more than ten times KPMG's FY30 revenue figure, and the combined USD 160 billion of underway and announced investment runs to nearly twenty-four times it (our calculation, from the two KPMG figures and the PIB total).

Source: Press Information Bureau; KPMG in India. Chart: The Signal.

The capital already committed runs to ten to twenty-four times the market it is meant to serve.

That gap is the story. It is not that India lacks a case for more data centres. It is that the money now committed is sized for a demand curve that has not yet shown up in the sector's own revenue projections.

Capacity is compounding fast, on paper

Colliers India separately finds that capacity had grown more than fourfold in six to seven years to reach 1,263 MW as of April 2025, and projects capacity across the top seven cities will cross 4,500 MW by 2030 on USD 20-25 billion of fresh investment, a further threefold jump from today's base. That 1,263 MW figure, for April 2025, sits below MeitY's own count of more than 1,500 MW for 2025 as a whole, a gap of at least a couple hundred megawatts between two credible counts taken only months apart.

Source: Ministry of Electronics and Information Technology, via PIB; Colliers India. Chart: The Signal.

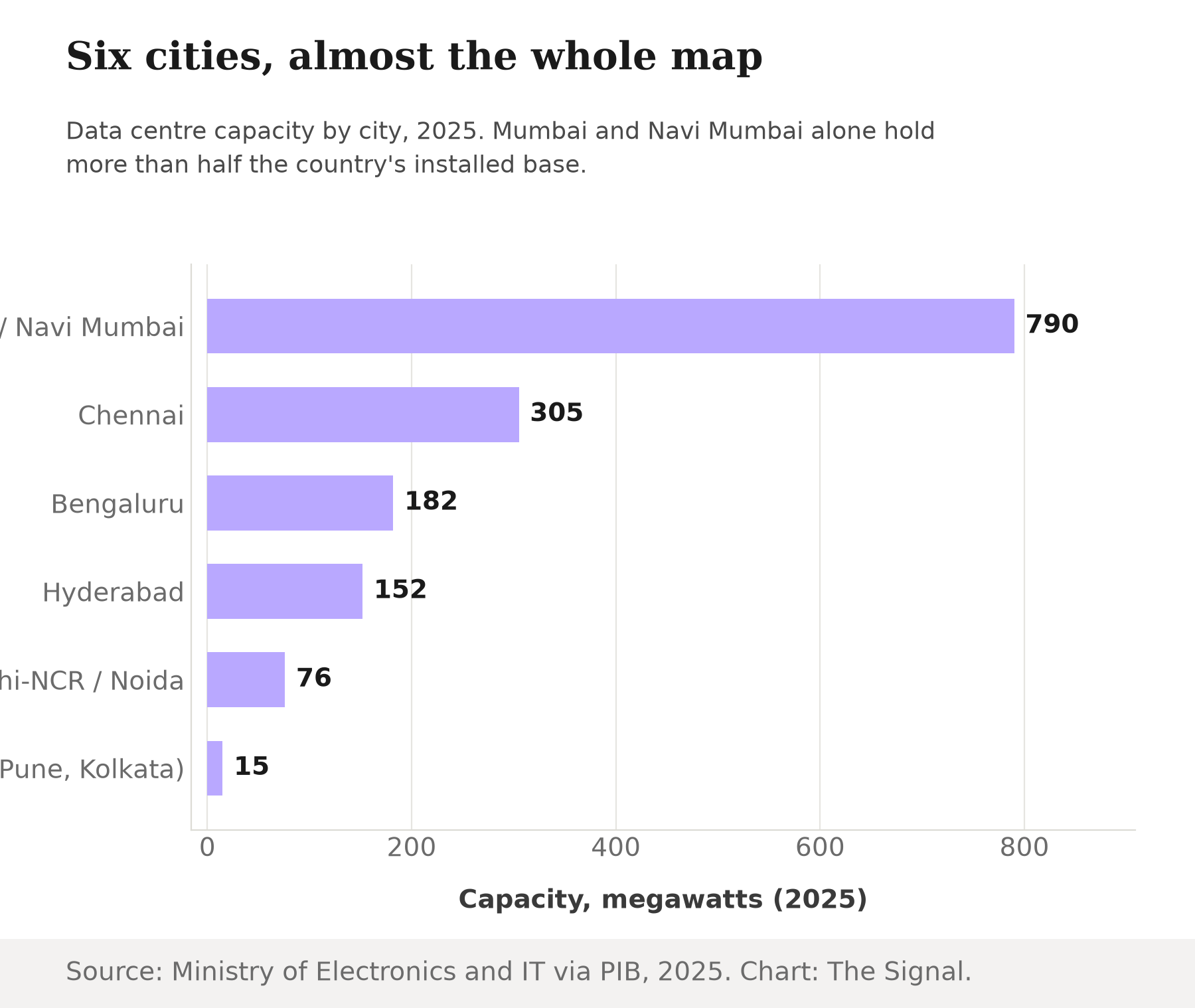

That expansion is not spread evenly. MeitY's own city breakdown puts Mumbai and Navi Mumbai at 790 MW, against 305 MW for Chennai, 182 MW for Bengaluru, 152 MW for Hyderabad, 76 MW for Delhi-NCR and Noida, and 15 MW for the rest. Mumbai and Navi Mumbai alone hold more than half the country's installed base.

Source: Ministry of Electronics and Information Technology, via PIB. Chart: The Signal.

What is actually running on it today

The confirmed-demand side of the ledger is thinner. A Council on Energy, Environment and Water white paper finds that in 2024, data centres accounted for around 0.5 per cent of India's national electricity consumption and roughly 150 billion litres of water use, with both shares projected to more than double by 2030, meaning even the doubled electricity figure stays close to one per cent of the grid. And the government's own dedicated AI compute programme is modest next to the capital totals above: a Press Information Bureau release states the IndiaAI Mission, approved by the Cabinet in March 2024, carries a Rs 10,371.92 crore budget over five years and had, as of December 2025, onboarded over 38,000 subsidised GPUs, up from an initial target of 10,000, available to users at a subsidised Rs 65 an hour.

Those are real numbers and they are moving in the right direction for the bull case: GPU onboarding has nearly quadrupled its own original target. But a national electricity footprint still under one per cent by 2030 and a sector revenue base still under USD 7 billion by the same year are not what a demand-led buildout of this size would usually show at this stage.

Whose numbers do you believe

No two trackers agree on the total, though all point the same direction.

| Tracker | Investment figure | Capacity figure | As of |

|---|---|---|---|

| Government of India, via PIB | USD 70bn underway + USD 90bn announced | More than 1,500 MW | Feb 2026 / Dec 2025 |

| Colliers India | USD 20-25bn fresh, next 5-6 years | 1,263 MW, target 4,500 MW by 2030 | Apr 2025 |

| CBRE India | USD 94bn in commitments, 2019 to 9M2025 | About 1,530 MW operational | Sep 2025 |

Sources as linked in the table above.

CBRE India's own count puts commitments since 2019 at nearly USD 94 billion, with operational stock at about 1,530 MW, translating to roughly 23 million square feet of built space, a different tally, a different window, and a different total from the government's. That gap between three professional counts of the same buildout, tens of billions apart, is itself a signal: this is a sector being measured after the fact, not one with an agreed baseline that new capital is being underwritten against.

The honest objection

The strongest case against calling this a mismatch is that infrastructure is supposed to run ahead of revenue. Power plants, telecom towers and toll roads all take years to fill, and a service that needs land, power connections and cooling secured well before a tenant signs cannot wait for confirmed demand before breaking ground. On this view, IndiaAI's GPU onboarding beating its own target and CEEW's own doubling of the power share by 2030 are exactly the ramp a capital-intensive build should show, just early in the curve.

The steelman has one more data point in its favour: built capacity itself is not sitting idle. A JLL India report finds the sector's vacancy rate had compressed to just 4.3 per cent by the first half of 2025, a supply-constrained market where what exists today is close to fully leased. That is a real signal that current demand has absorbed current supply.

That case is real, but it does not explain the size of the gap or the disagreement about the very numbers meant to justify it. A capital-intensive build usually has one tracker's estimate of the base it is scaling from; India's has three, ranging from roughly 1,263 MW to more than 1,500 MW in capacity and from USD 94 billion to USD 160 billion in investment, within months of each other. And a sector revenue base projected at under USD 7 billion by FY30, against USD 70 billion already logged as underway, is a wider gap than "early in the ramp" alone accounts for. A market can be fully let at 1,500 MW and still be badly oversized for what gets built at 4,500 MW: full occupancy of today's stock says demand caught up with today's build, not that it will catch up with a build three times the size. The money looks less like it is financing confirmed tenants and more like it is securing scarce land and power connections now, on a bet that the demand catches up later.

The Signal

The India data centre story is not really about whether the capacity gets built. On present trackers it almost certainly will. It is about who is holding the risk while the market underneath it stays small: land and power are being locked in years before the revenue that is supposed to justify them, and three separate professional trackers cannot even agree on how much has been spent so far. Most of that risk sits abroad: Houlihan Lokey finds foreign institutional investors contributed about 86 per cent of the USD 14.7 billion in data centre investment India attracted between 2020 and April 2025, so the bet that demand catches up later is mostly a foreign bet. Watch two numbers over the next two years, not the announcement totals. If data centres' share of the national grid and KPMG's revenue line move up together with the capacity being switched on, the capital was early, not wrong. If capacity keeps compounding while those two lines stay flat, the money was never chasing demand. It was chasing land.

Reporting basis: the investment and capacity totals for India's data centre sector are drawn from three separate trackers who do not agree with one another: a Press Information Bureau backgrounder on Budget 2026-27 and a separate PIB release citing the Ministry of Electronics and Information Technology, both government sources; Colliers India's own research note; and a CBRE India report. The IndiaAI Mission's budget and GPU count are from a Press Information Bureau release on that programme. The data centre sector's electricity share and its trajectory to 2030 are from a Council on Energy, Environment and Water white paper. The market size and India-versus-global capacity share figures, including the FY30 revenue projection that anchors this piece's central comparison, are from a KPMG in India sector analysis and are not independently corroborated by another tracker. Amazon's cumulative India investment figure is as reported by CNBC. The foreign-investor share of committed capital is from a Houlihan Lokey real estate sector report, and the vacancy rate on existing capacity is from a JLL India market dynamics report. The ratios of total committed investment to KPMG's projected FY30 revenue are The Signal's calculations from those figures.