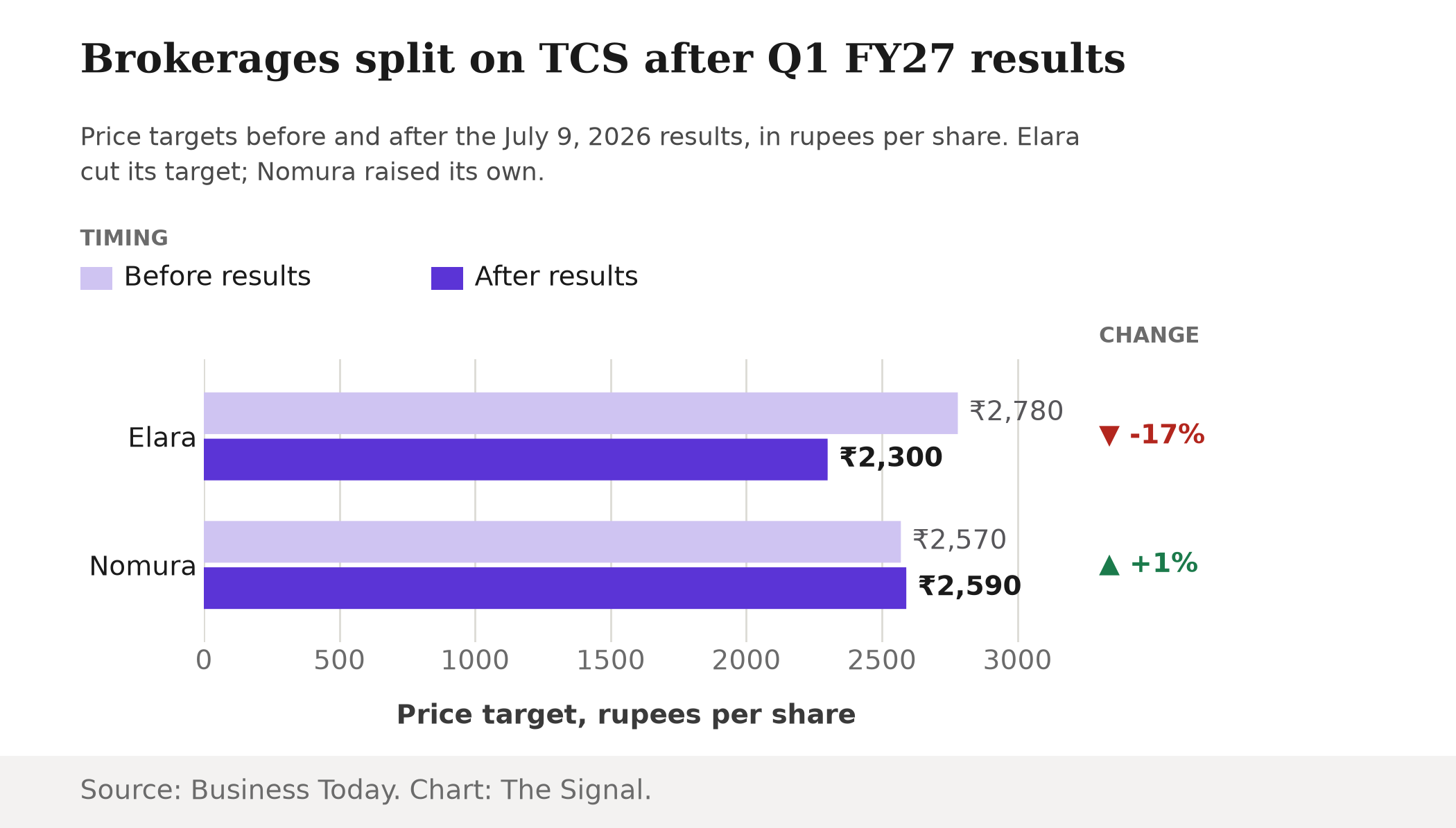

Tata Consultancy Services reported its first-quarter results for fiscal year 2027 on July 9, 2026, and the market delivered a verdict fast. Shares climbed nearly 4 percent the next trading day, adding ₹26,720 crore to TCS's market capitalisation, even as the brokerage notes that followed split hard on where the stock goes from here. Elara Securities cut its price target 17 percent, to ₹2,300 from ₹2,780, while Nomura India raised its own target to ₹2,590 from ₹2,570, on the same set of numbers. Read only the target-price fight and TCS looks like a stock nobody can agree on.

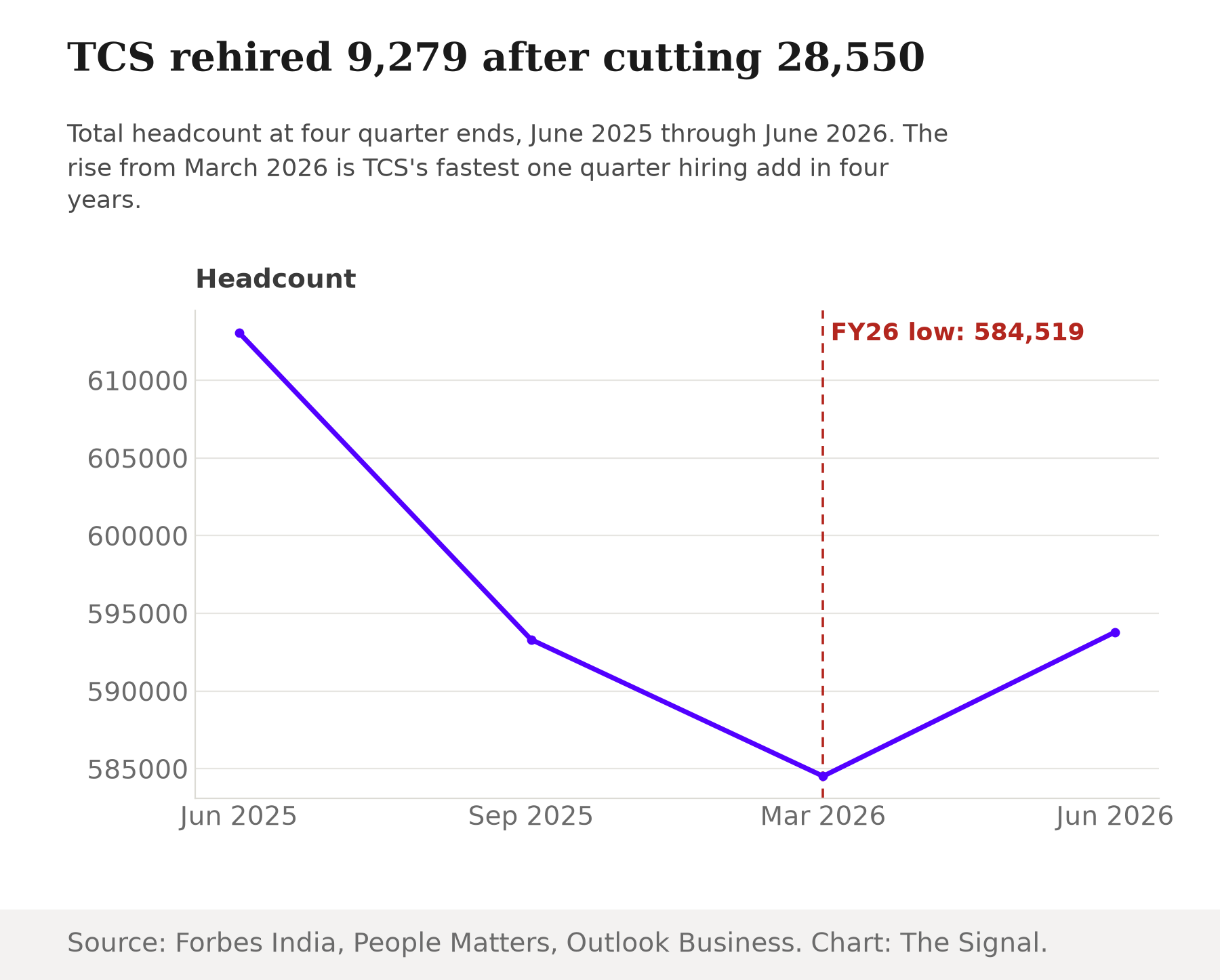

It is worth slowing down on that disagreement, because it buries the more telling number in the same results. TCS added a net 9,279 employees in the quarter, taking its total headcount to 593,798, and The People's Board reports that this is the company's strongest quarterly headcount addition in four years. On the same earnings call, TCS CEO K Krithivasan said the company does not believe there will be a drastic change in headcount from AI, expecting workers to shift into roles like prompt engineering instead. A brokerage target is a forecast, revised on a quarterly cycle. A headcount number is a decision the company has already made and has to live with.

TCS shed 28,550 jobs before it hired any back

The shape of the reversal only reads clearly across four quarters.

TCS's headcount fell to a 14-quarter low of 593,314 in the quarter ended September 2025, a sequential decline of nearly 20,000 from 613,069 the quarter before. The slide did not stop there. TCS closed the full fiscal year 2026 (the year to March 2026) with 584,519 employees, down 23,460 from a year earlier, a trough the company has called the end of its restructuring exercise. From that low point in March 2026, the addition of 9,279 workers in the very next quarter is not a modest uptick. It is TCS's sharpest one-quarter swing since the cuts began.

Hiring is the harder signal to fake

A brokerage price target costs almost nothing to change: revise the slide deck, publish a new note, and the only thing at stake next quarter is the analyst's own credibility. Payroll is a heavier kind of commitment. Salaries, benefits, training, and severance if the bet is wrong all land on TCS's books long after any forecast has moved on. Viewed as revealed preference rather than a stated opinion, TCS's hiring line is the harder signal to fake. A company that genuinely expected AI to shrink its workforce over the near term would not be running its fastest headcount addition in four years the same month one of its own brokers cut its price target 17 percent. What the company does with its payroll is a sharper read on how it actually expects AI to hit Indian IT jobs than what any single analyst writes about its stock.

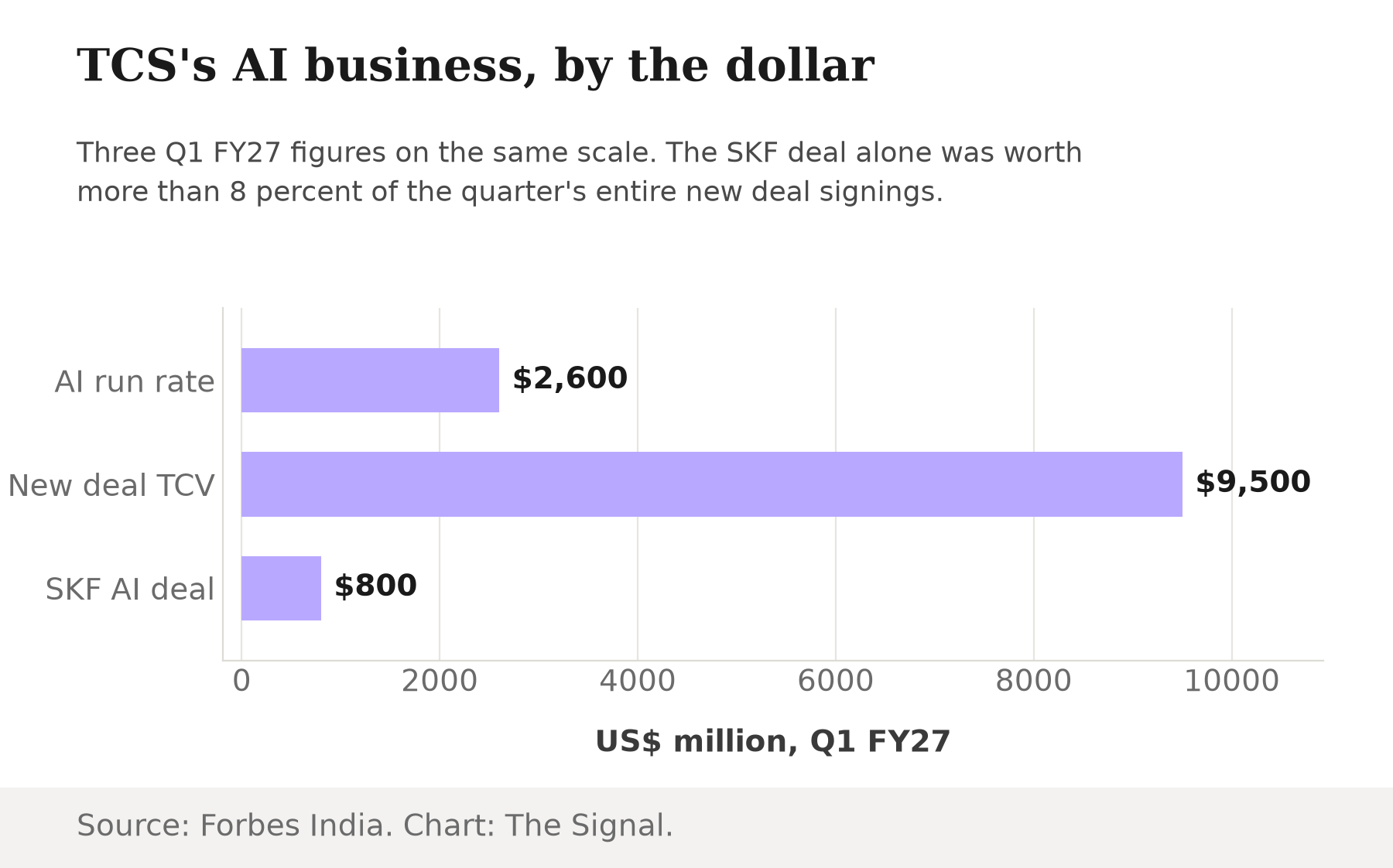

The AI money is scaling too, not instead

TCS is not hiring because it has stepped back from AI. The company's AI business reached a $2.6 billion annualised revenue run rate in the quarter, on $9.5 billion of new deal bookings (total contract value), including an $800 million AI-led transformation deal with the bearings maker SKF.

That single SKF contract was worth more than 8 percent of the quarter's entire new-deal haul on its own. The growth is not costless, either: revenue rose 13.9 percent year on year in rupee terms, 2.7 percent in dollar terms, to $7,624 million, while operating margin compressed 130 basis points to 24.0 percent, a decline management attributed to the annual salary increases it had just paid out. TCS scaled its AI bookings and added headcount and paid more per employee, in the same quarter. That combination is hard to square with a company quietly using AI to shed people.

Two national studies frame TCS's hiring bet against a much bigger, more contested picture.

| Signal | Figure | Source |

|---|---|---|

| India's software services exports, FY2024-25 | US$204.7 billion, up 7.3% year on year | Reserve Bank of India |

| Potential new AI-enabled tech-sector jobs, five-year horizon, with a coordinated national approach | Up to 4 million | NITI Aayog, October 2025 |

| IT business units reporting AI productivity gains vs. declines | 3.5 to 1 | ICRIER-OpenAI survey, fielded Nov 2025 to Jan 2026 |

| IT firms reporting rising demand for hybrid domain-plus-AI skills | 63% | ICRIER-OpenAI survey, fielded Nov 2025 to Jan 2026 |

Source: Reserve Bank of India; NITI Aayog's Roadmap for Job Creation in the AI Economy, via DD News; ICRIER-OpenAI study, via The Bridge Chronicle.

TCS anchors an industry the Reserve Bank of India put at $204.7 billion in software services exports in FY2024-25, up 7.3 percent on the year before. The same NITI Aayog roadmap that projects up to 4 million new AI-enabled jobs also flags the risk of job displacement by 2031 if the transition is not managed well: the upside is conditional, not guaranteed. And the sector-wide survey data cuts both ways too. An ICRIER-OpenAI survey of more than 650 Indian IT firms found business units reporting AI productivity gains outnumbering those reporting declines by 3.5 to 1. The same survey found 63 percent of firms reporting rising demand for workers who combine domain expertise with AI skills, even as entry-level hiring moderates. TCS's quarter is consistent with that picture. It is not proof the picture is settled.

The honest objection

The strongest case for treating TCS's hiring number skeptically does not need any AI-phobia to work. TCS's own operating margin compressed 130 basis points to 24.0 percent in the same quarter, a decline management pinned on the wage increases it had just paid out, so the cost line funding the hiring rebound is the same cost line brokers like Elara are pricing as a margin risk. And the caution is not confined to TCS's stock: the ICRIER-OpenAI survey found entry-level hiring moderating across the sector even as productivity gains outnumber declines 3.5 to 1. That fits a wider industry still cautious on graduate intake, even as a handful of large players absorb workers back at the margin. On this reading, TCS's quarter is encouraging, not decisive: one company's rebound, funded by margin pain, inside a sector still cooling on entry-level hiring.

That case is real, and margins matter. But it argues for caution about the industry, not about TCS's own number. TCS's human-resources chief has said the company's restructuring exercise is complete and that it still expects to hire roughly 40,000 freshers a year, a run-rate the company was already committed to even through the year it cut headcount by tens of thousands on net. TCS's CHRO said the company gave offers to more than 14,000 freshers in the quarter alone, more than the entire 9,279 net addition. That gap means attrition and changes among experienced staff quietly offset a chunk of that intake even as the total climbed. A quarter that still came in as TCS's strongest net headcount addition in four years is not explained by routine freshers intake alone. The margin hit funded that hiring. It did not prevent it.

Whether that hiring is a TCS story or an industry story is also still an open question. Infosys, the peer closest to TCS in scale, cut headcount by 8,440 in the March 2026 quarter, its first decline after six straight quarters of growth. Infosys, Wipro and HCLTech had not yet reported their own April-June 2026 results as of this writing, so there is no same-quarter comparison yet to say whether TCS's rebound is company-specific or the start of a sector-wide pattern.

The Signal

Brokerage notes get revised every quarter with no consequence for the analyst beyond a changed number on a slide. TCS's payroll does not work that way. The company added more people in one quarter than in any quarter in four years, scaled its AI bookings to $9.5 billion at the same time, and paid for both with a margin hit it chose to absorb rather than avoid. That is a company betting its own money that AI augments its workforce faster than it replaces it, at least for now. Watch two things next: whether the hiring pace holds through the next quarterly print, and whether the AI revenue run rate keeps climbing without headcount reversing again. If both keep rising together, TCS's own ledger will have said more about AI and Indian IT jobs than any brokerage note ever could. If hiring rolls over while AI revenue keeps climbing, that reversal will say more than this quarter's target-price argument ever could.

Reporting basis: TCS's Q1 FY27 net headcount addition and total headcount are per Outlook Business's reporting of the company's disclosures; the four-year hiring superlative and the CEO's headcount comments are per The People's Board's report of the same earnings call. The AI business run rate, new deal bookings and the SKF deal are per Forbes India's report of the earnings call. The September 2025 14-quarter-low headcount figure is per a separate Forbes India report; the FY26 year-end headcount and the CHRO's freshers guidance are per People Matters. Revenue, margin and the wage-increase attribution are per Investing.com's report of TCS's results slides. The share-price move, market-capitalisation gain and both brokerages' price targets are per Business Today. India's software services export figure is from the Reserve Bank of India. The AI jobs roadmap is NITI Aayog's, as reported by DD News. The productivity and hiring-demand survey findings are from the ICRIER-OpenAI study, as reported by The Bridge Chronicle. The freshers-offers figure is per Upstox's report of the CHRO's earnings-call remarks. Infosys's March 2026 headcount decline is per Outlook Business. The 28,550 headcount decline from June 2025 to March 2026 and the SKF deal's 8 percent share of new bookings are The Signal's calculations from those figures.