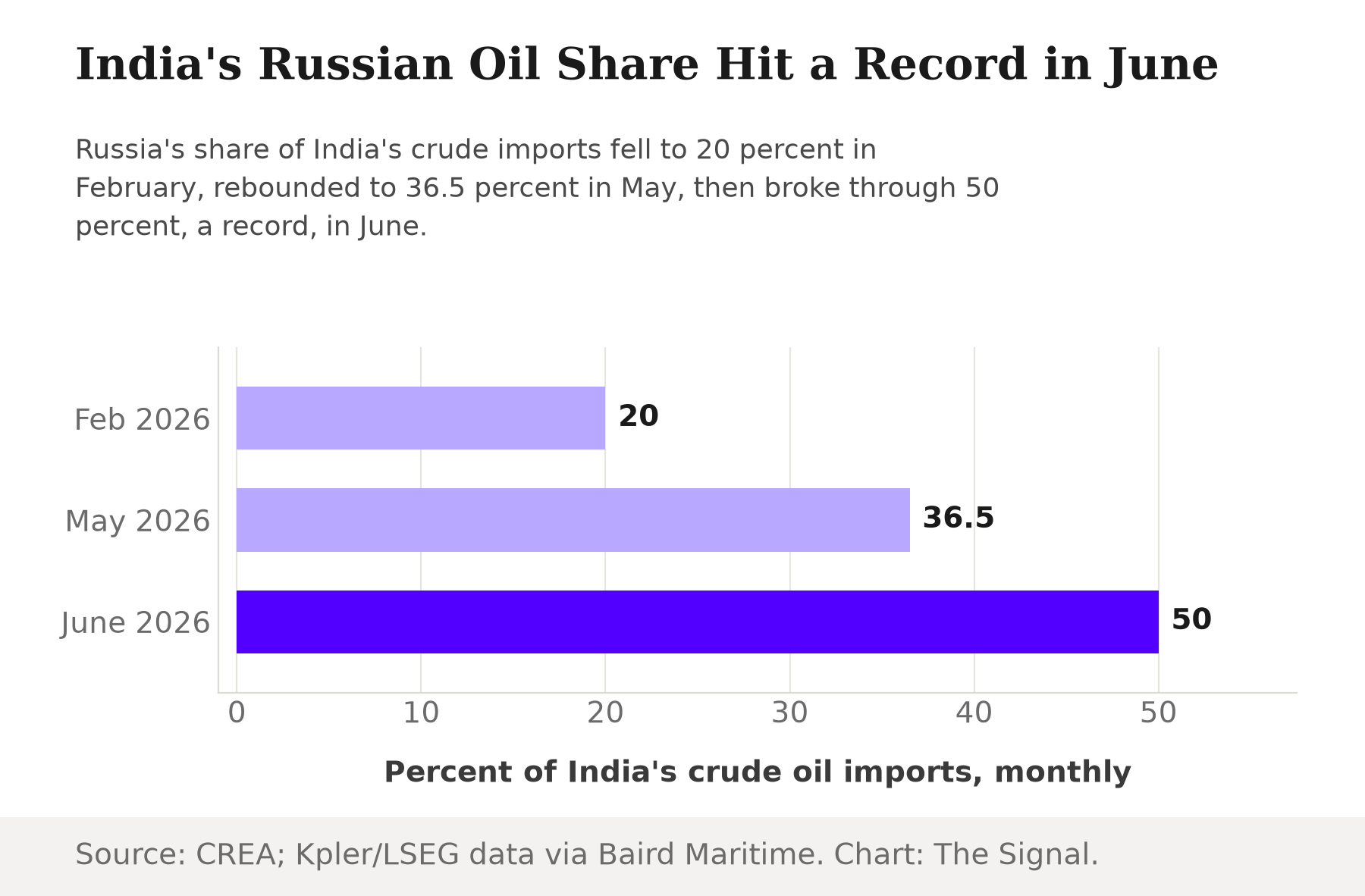

On February 2, 2026, Donald Trump agreed to cut the US tariff on Indian goods from 25 percent to 18 percent after Prime Minister Modi committed to halting purchases of Russian oil. Indian imports of Russian crude were projected to fall from about 1.2 million barrels a day in January to roughly 800,000 barrels a day by March. For a few weeks, the data matched the promise: Russia's share of India's crude imports fell to just 20 percent in February, after Russian volumes dropped 19 percent month on month, even as Russia remained India's single largest supplier. Read the headline numbers from February and the story looks settled: tariff diplomacy worked, and India was walking back its wartime bargain-hunting.

It is worth slowing down on that. By May, Russia's share of India's crude imports was back up to 36.5 percent, and in June it topped 50 percent for the first time on record, with Indian refiners taking in about 2.70 million barrels a day of Russian crude, according to Kpler and LSEG ship-tracking data. That is more than triple the roughly 800,000 barrels a day the tariff deal was supposed to leave India buying by March. The reversal would be a straightforward story about a broken promise, except for one detail: the discount that made Russian oil worth the diplomatic trouble in the first place had, by June, all but disappeared.

India's reliance on Russian oil hit a record the same month the price incentive for it nearly vanished.

Source: Baird Maritime, citing Kpler and LSEG ship-tracking data; Centre for Research on Energy and Clean Air. Chart: The Signal.

The discount that justified the switch shrank

The entire case for buying Russian crude over Gulf or Atlantic Basin barrels was always the price. That price edge thinned out sharply just as India's dependence on it peaked.

| Cargo delivery window | Price of India-bound Urals crude vs. Brent |

|---|---|

| May-delivery cargoes | Premium of $6 to $7 a barrel over Brent |

| June-delivery cargoes | Premium of $2 to $4 a barrel over Brent |

| About 10 days before the August-delivery report | Discount of about $4 a barrel to Brent |

| August-delivery cargoes (reported around July 1) | Discount widened to below $7 a barrel to Brent |

Source: Baird Maritime; Baird Maritime.

Urals crude delivered to Indian ports traded at a premium of $2 to $4 a barrel over Brent in June, down from a premium of $6 to $7 a barrel for May-delivery cargoes: the margin that once made Russian barrels cheap had shrunk toward zero. Only in July, after Middle Eastern supply began flowing again, did the arithmetic reset: discounts for India-bound August-delivery cargoes widened back out to below $7 a barrel, up from about $4 a barrel roughly ten days earlier, as Gulf supply resumed through a reopening Strait of Hormuz. By the time the discount widened again, June's record had already been set.

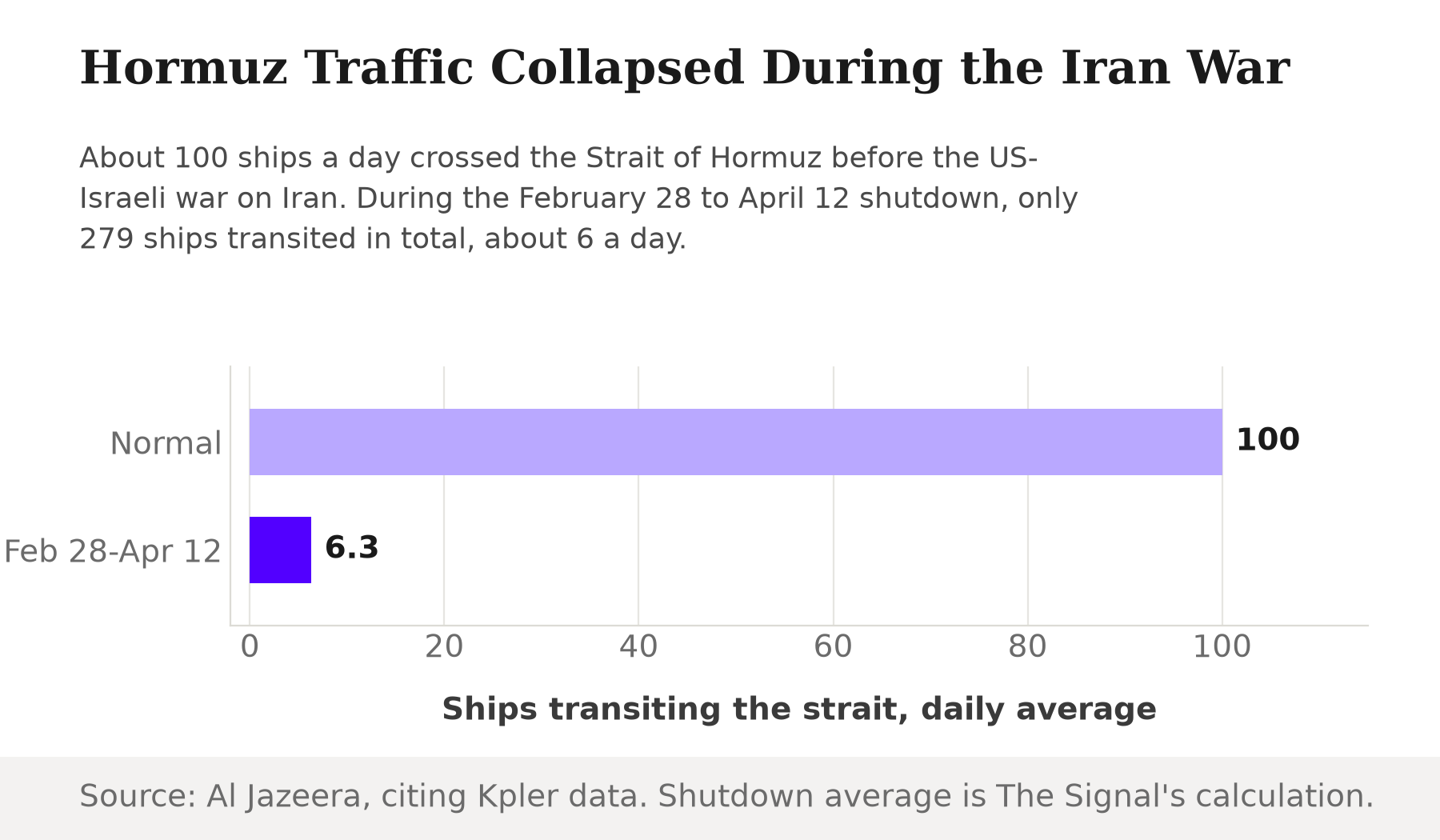

A shut strait, not a sale, drove the surge

The gap in the timeline is a war. The United States and Israel launched strikes on Tehran on February 28, 2026, and Iran declared the Strait of Hormuz closed on March 2. Only 279 ships transited the strait between February 28 and April 12, against roughly 100 crossings a day before the war: a drop of about 94 percent in daily transits over that six-week window, on The Signal's calculation from those two figures.

Hormuz traffic collapsed by roughly 94 percent during the six-week shutdown.

Source: Al Jazeera, citing Kpler ship-tracking data and Iranian officials. Daily-transit figures are The Signal's calculation. Chart: The Signal.

The strait matters precisely because of who depends on it. In 2024, oil flow through the Strait of Hormuz averaged about 20 million barrels a day, roughly a fifth of global petroleum liquids consumption, and 84 percent of that oil went to Asian markets led by China, India, Japan and South Korea. A shutdown of that scale does not fall evenly on the world. It falls, disproportionately, on the same handful of Asian buyers who were already leaning on Russian crude, which does not transit Hormuz at all. When the strait closed, Russian oil stopped being merely the cheaper option and became one of the few options that could not be cut off by the same war.

India's response was not the regional default. China's crude imports fell 3.6 million barrels a day from February to April 2026, Japan's fell 1.9 million barrels a day and South Korea's fell 1 million barrels a day over the same stretch, as all three simply absorbed the shortfall rather than substituting at scale, per the International Energy Agency. Combined with India's own 760,000-barrel-a-day cut, the four countries' import losses totaled an unprecedented 7.2 million barrels a day since the war began. China, Japan and Korea took the hit as a demand shock, while India, uniquely among them, had a supplier that could backfill it.

A security trade, not a savings trade

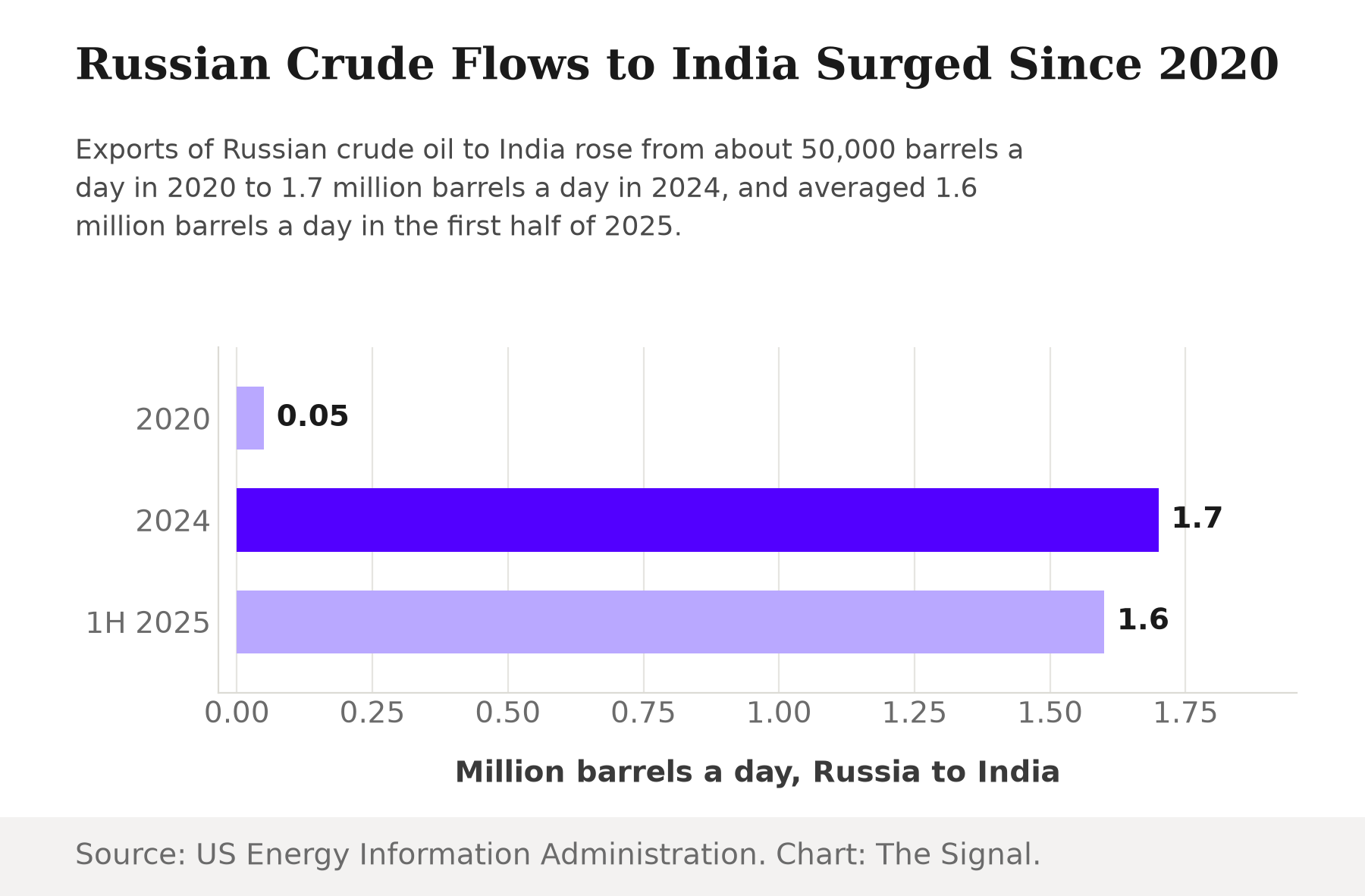

Line up the numbers and the switch in motive is hard to miss. India was the second-largest buyer of Russian fossil fuels in May 2026, importing EUR 5.8 billion of Russian hydrocarbons, with crude oil accounting for 83 percent, or EUR 4.8 billion, of that total: a scale of purchasing that was still rising even as the price cushion behind it was thinning. None of this appeared from nowhere. Russia's crude exports to India rose from about 50,000 barrels a day in 2020 to 1.7 million barrels a day in 2024, averaging 1.6 million barrels a day in the first half of 2025, as Asia's share of Russia's total crude exports climbed from 41 percent in 2020 to 81 percent in 2024. The war did not invent India's Russian-oil habit. It interrupted a brief attempt to wind the habit down, then handed India a supply-security reason to let it run past its old highs instead.

Source: US Energy Information Administration. Chart: The Signal.

The honest objection

The strongest case against reading this as a deliberate security pivot is that the June numbers may simply be a scramble. Ship-tracking data on a given month is preliminary and gets revised, refiners often lock in cargoes weeks before delivery, and a chunk of June's Russian barrels may have been contracted during the worst of the Hormuz shutdown in March and April, arriving late rather than reflecting a fresh decision made in June itself. On that reading, India was not choosing Russian oil for security in June so much as still digesting orders placed in a panic months earlier, and the swift return of a wider discount in July, once Gulf supply resumed, shows price discipline reasserting itself the moment it could.

That case fits the mechanics, but it does not explain the timing. If June's volumes were simply a delayed echo of March's panic buying, the margin on those barrels should have been irrelevant to the decision, since the order predates the price. Instead the record was set in the exact month the premium over Brent had shrunk to $2 to $4 a barrel, the thinnest edge on record for these cargoes, which is when a refiner motivated purely by savings would have had the least reason to keep buying. A buyer chasing a bargain does not set a record the month the bargain nearly disappears. That is what a buyer chasing supply security looks like.

The Signal

The tariff deal tested whether price and diplomacy could pry India off Russian crude, and for a few weeks in February, it looked like they had. Then the Strait of Hormuz posed a different test: whether India would still buy Russian oil once the discount that justified it was gone. It would. Watch what happens now that the strait has reopened and the discount is widening again: if India's Russian share retreats toward February's 20 percent, the June spike really was an emergency measure. If it holds near June's record above 50 percent even as Gulf oil flows normally and the price gap reopens, the emergency measure will have become the new baseline, tariff deal or not.

Reporting basis: the June and May 2026 Russian crude import share and Urals pricing figures are from Kpler and LSEG ship-tracking data, as reported by Baird Maritime, across three separate Baird Maritime articles. The February 2026 import share is per the Centre for Research on Energy and Clean Air's monthly sanctions tracker, which also supplies the May 2026 total value of India's Russian fossil-fuel purchases. The Trump-Modi tariff agreement and its projected import trajectory, and the Strait of Hormuz war timeline and transit counts, are per Al Jazeera, the latter citing Kpler ship-tracking data and Iranian officials. The strait's normal oil-flow volume and its Asian-market share, and Russia's 2020-2025 crude export trend to India, are from separate US Energy Information Administration analyses. The February-April 2026 crude import figures for China, Japan, South Korea and India are per the International Energy Agency's May 2026 Oil Market Report. The Hormuz transit-count change and the daily-average ship figure during the shutdown are The Signal's calculations from Al Jazeera's reported figures.