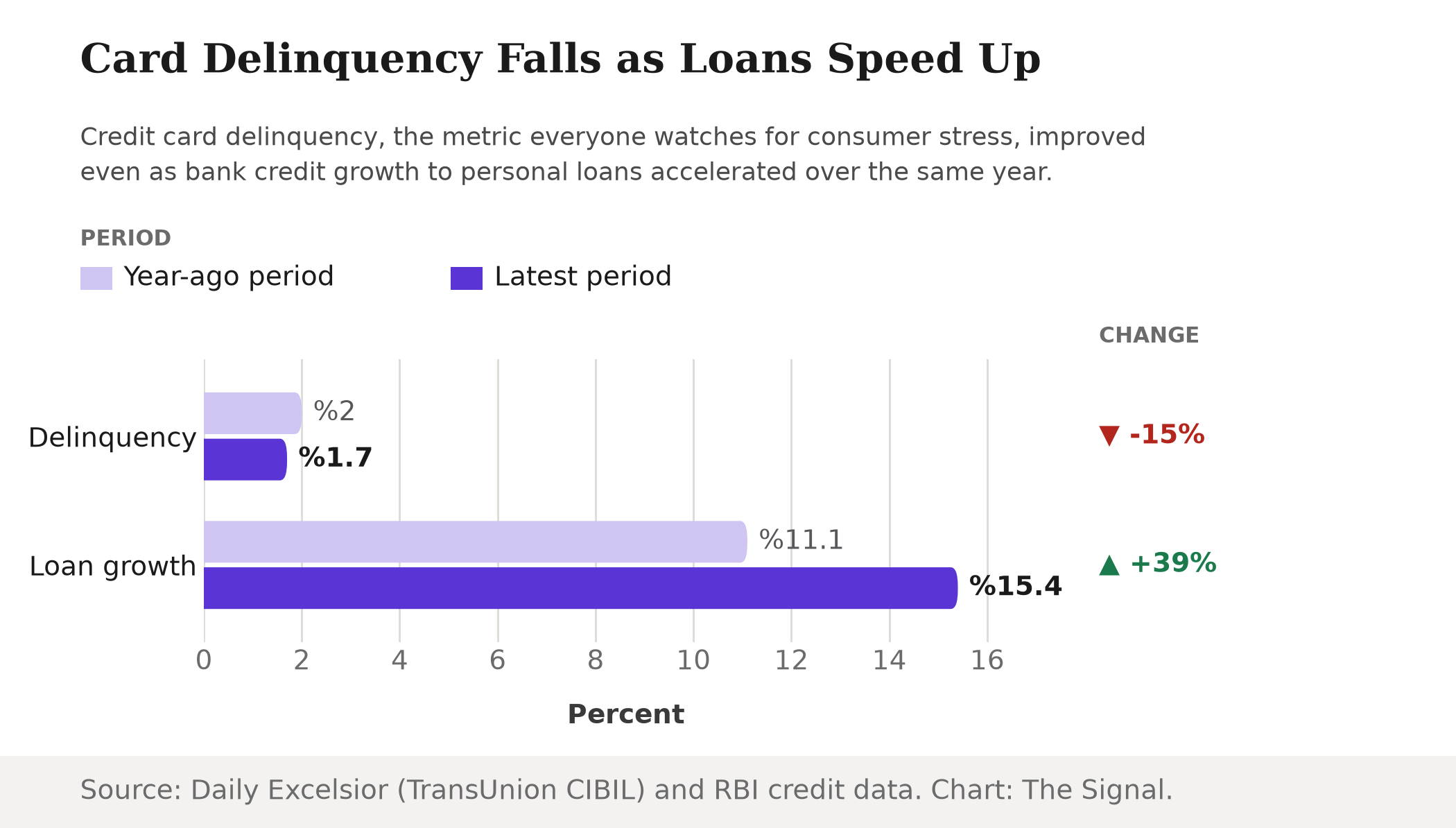

India's credit card book looks healthier than it has in years. Credit card delinquency, accounts 91 to 179 days past due, improved to 1.7% in the year to March 2026 from 2.0% in the year-ago period, Daily Excelsior reports, citing TransUnion CIBIL data. TransUnion CIBIL's own Credit Market Indicator, a single gauge of the health of India's retail credit market, rose to 102 in the December 2025 quarter from 97 a year earlier, its third consecutive quarterly improvement. Read only those two lines and the conclusion writes itself: Indian households are managing debt better, banks are lending more carefully, and the credit cycle is turning up.

It is worth slowing down on that. The card book is not shrinking, but it has become far more selective about who gets in, and the borrowers it now shuts out have not stopped wanting credit. Only 8% of new credit card additions in the year to March 2026 went to consumers with no prior credit history, down from 26% in the year-ago period, Deccan Chronicle reports, citing TransUnion CIBIL MD and CEO Bhavesh Jain. Banks are deepening relationships with the customers they already trust, not opening the card book to new ones.

Strip the delinquency number out of the picture and follow those excluded borrowers instead. India's outstanding bank credit to the personal loans segment grew 15.4% year on year in the fortnight ended May 31, 2026, up from 11.1% growth a year earlier, the Reserve Bank of India's Sectoral Deployment of Bank Credit release reports. Personal loan originations among first-time borrowers grew 20% year on year in the December 2025 quarter, reversing a 3% decline in the year-ago quarter, TransUnion CIBIL's Credit Market Indicator report states. The figure that actually carries this story is not the improving card delinquency rate. It is that reversal, from a 3% decline to 20% growth among first-time personal loan borrowers, arriving in the same year that first-time card issuance collapsed from 26% to 8% of new accounts: not a story about universally improving underwriting, but about the same borrowers walking up to a different counter.

Where the excluded borrowers land

The RBI's own numbers point at the mechanism. In November 2023, before any of the 2025-2026 data described here existed, the RBI raised the risk weight on banks' unsecured consumer credit exposure, including personal loans, by 25 percentage points to 125%, and on credit card receivables by 25 percentage points to 150% for banks and 125% for NBFCs, while explicitly excluding housing, education, vehicle and gold loans. A higher risk weight makes a loan more expensive for a bank to hold in capital terms, and the RBI set the credit card weight higher than the personal loan weight.

Cards became the costlier product for a bank to hold.

| Exposure type | Increase (Nov 2023) | New risk weight |

|---|---|---|

| Personal loans, banks | +25 points | 125% |

| Credit card receivables, banks | +25 points | 150% |

| Credit card receivables, NBFCs | +25 points | 125% |

| Housing, education, vehicle, gold loans | Excluded | Unchanged |

Source: Reserve Bank of India notification, November 2023.

A bank facing a costlier capital charge on card receivables than on personal loans, while both sit in the same "unsecured consumer credit" bucket the regulator is watching, has an obvious lever: keep the card book to known, low-risk customers, and let the personal loan book, still growing fast, absorb the new and marginal names.

The risk did not disappear, it moved to a category with a worse track record

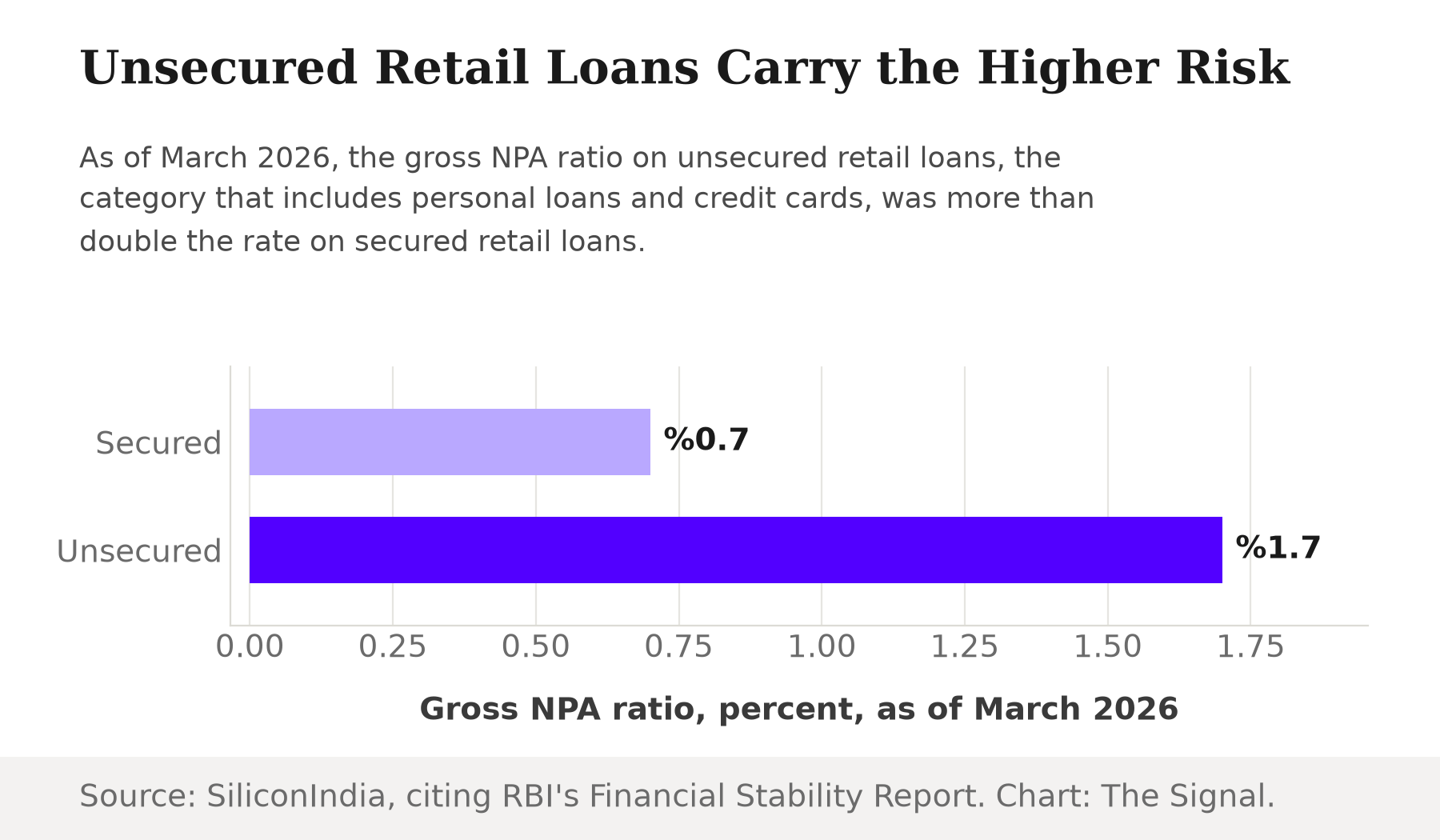

The problem with treating this as a wash is that personal loans are not a safer place to park the same risk. The RBI's Financial Stability Report, June 2026, put the gross NPA ratio at 0.7% for secured retail loans versus 1.7% for unsecured retail loans as of March 2026, SiliconIndia reports. Personal loans and credit cards both sit inside that unsecured bucket, and its bad-loan rate already runs more than double the secured book's.

Non-housing retail loans, the consumption-driven category that includes personal loans and credit cards, made up 58.4% of total Indian household borrowings as of March 2026, Policy Circle reports, citing the same Financial Stability Report. That is the scale of the book now carrying the risk that used to show up, and get flagged, on the card side. A watched gauge improving while the underlying exposure keeps growing in a worse-performing bucket is not the same as the exposure shrinking.

The card wallet is not a stand-alone product anymore either

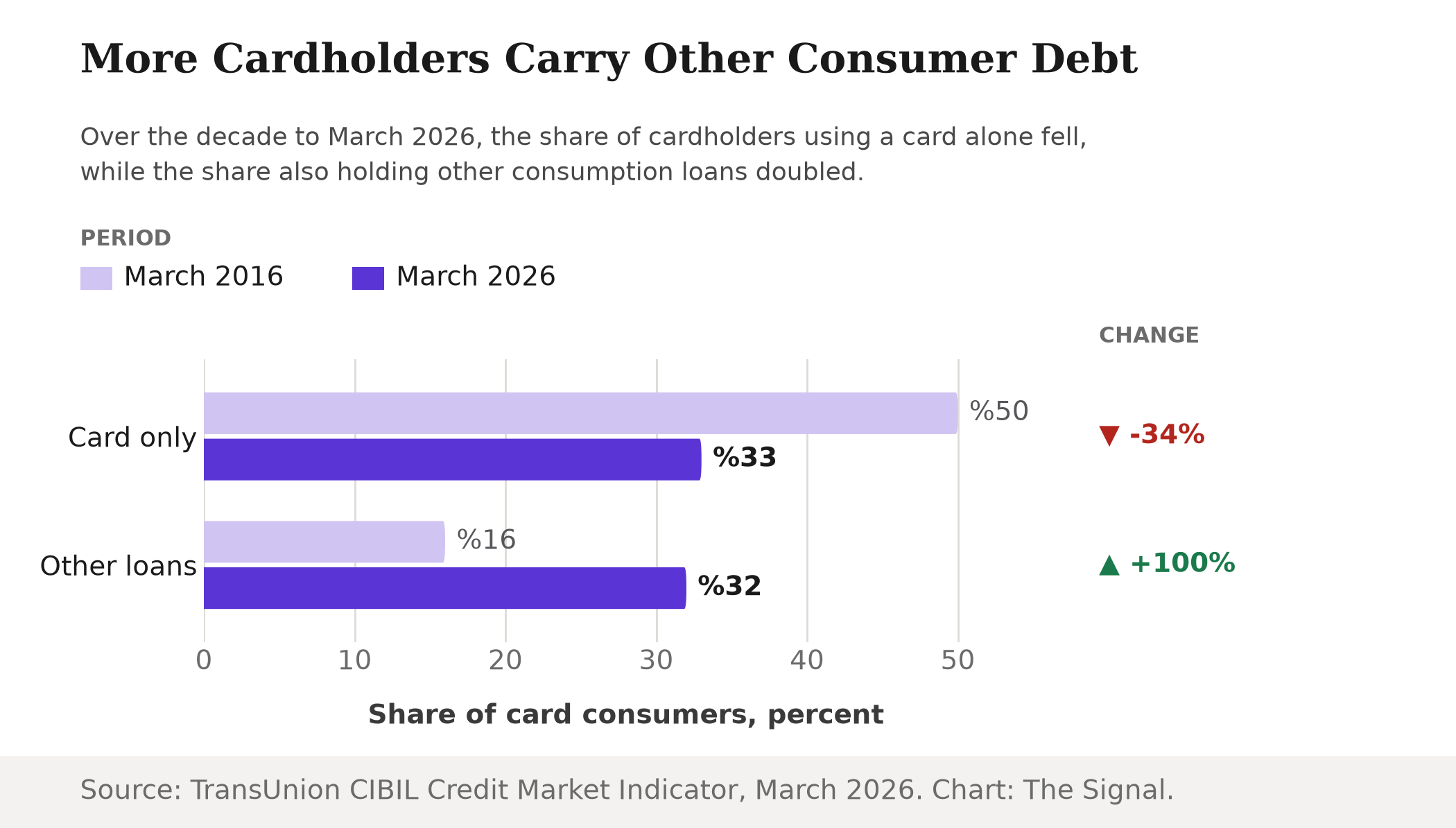

Even the cardholders who keep their cards are borrowing more elsewhere. The share of India's credit card consumers who hold only a card, with no other loan, fell from 50% in March 2016 to 33% in March 2026, while the share also holding other consumption loans rose from 16% to 32% over the same decade, TransUnion CIBIL's Credit Market Indicator reports.

The cards themselves are carrying more, too. The average outstanding credit card balance per Indian cardholder roughly doubled over the decade to March 2026, rising from about ₹31,000 to about ₹65,000, even as outstanding balances overall grew 8.3 times, BusinessToday reports, citing TransUnion CIBIL. Because the average balance only doubled while the total outstanding book grew more than eight-fold, the number of active cardholders behind that total must have grown roughly four times over: the card market widened even as its newest, riskiest entrants got redirected to personal loans instead. Both trends, a shrinking card-only wallet and a widening but redirected card base, point the same way: the credit card has stopped being India's entry product for new borrowers, and the delinquency rate calculated on that narrower, more curated book is measuring a smaller, safer slice of total household credit than it used to.

The honest objection

The strongest case against reading this as risk migration is that the improvement looks too broad to be a selection effect. TransUnion CIBIL's Credit Market Indicator has now improved for three straight quarters, not just on cards, and a metric built from multiple product lines climbing for that long could reflect a genuine, system-wide gain in underwriting quality after the RBI's 2023 intervention forced lenders to price risk more carefully everywhere, not a shell game between two products.

That case is real, but it does not explain the direction of the gap. If underwriting had simply gotten better across the board, the unsecured retail NPA ratio would be converging toward the secured book's 0.7%, not sitting at 1.7% as of March 2026. And a genuine system-wide improvement would not require personal loan originations among first-time borrowers to swing from a 3% decline to 20% growth in the same quarter that card issuance to the same group cratered. A broad improvement and a sharp product-level substitution are not mutually exclusive, but the size and precision of the swap, concentrated exactly among first-time borrowers, in the same year, in the two products, is more than a system-wide trend would produce on its own.

The Signal

The headline card delinquency rate, 1.7% and falling, is not wrong. It is just measuring a book that has been quietly redrawn to exclude the borrowers likeliest to default, who have not stopped borrowing, only moved to a product with a worse historical loss rate and looser scrutiny from the metric everyone actually watches. Watch what happens to personal loan delinquency data as the current cohort of first-time borrowers, onboarded through 2025 and 2026, seasons past its first year of repayment. If that number stays flat, the RBI's 2023 risk-weight shift genuinely raised underwriting quality across the unsecured book. If it climbs, the country's consumer-credit stress gauge will have been watching the wrong door the whole time.

Reporting basis: credit card delinquency and the new-to-credit share of card issuance are TransUnion CIBIL figures, as reported respectively by Daily Excelsior and Deccan Chronicle, which also cited TransUnion CIBIL's Bhavesh Jain directly. The Credit Market Indicator, first-time personal loan borrower growth, and the card wallet composition figures are from TransUnion CIBIL's own newsroom releases. Personal loan bank credit growth is from the Reserve Bank of India's Sectoral Deployment of Bank Credit release. The November 2023 risk-weight change is from the Reserve Bank of India's own notification. The secured-versus-unsecured NPA ratio and the non-housing share of household borrowings both originate in the RBI's Financial Stability Report, June 2026, as reported respectively by SiliconIndia and Policy Circle. The average and total credit card balance figures are from BusinessToday, citing TransUnion CIBIL. The estimate that India's active cardholder base grew roughly four times over the decade to March 2026 is The Signal's calculation from those balance figures.