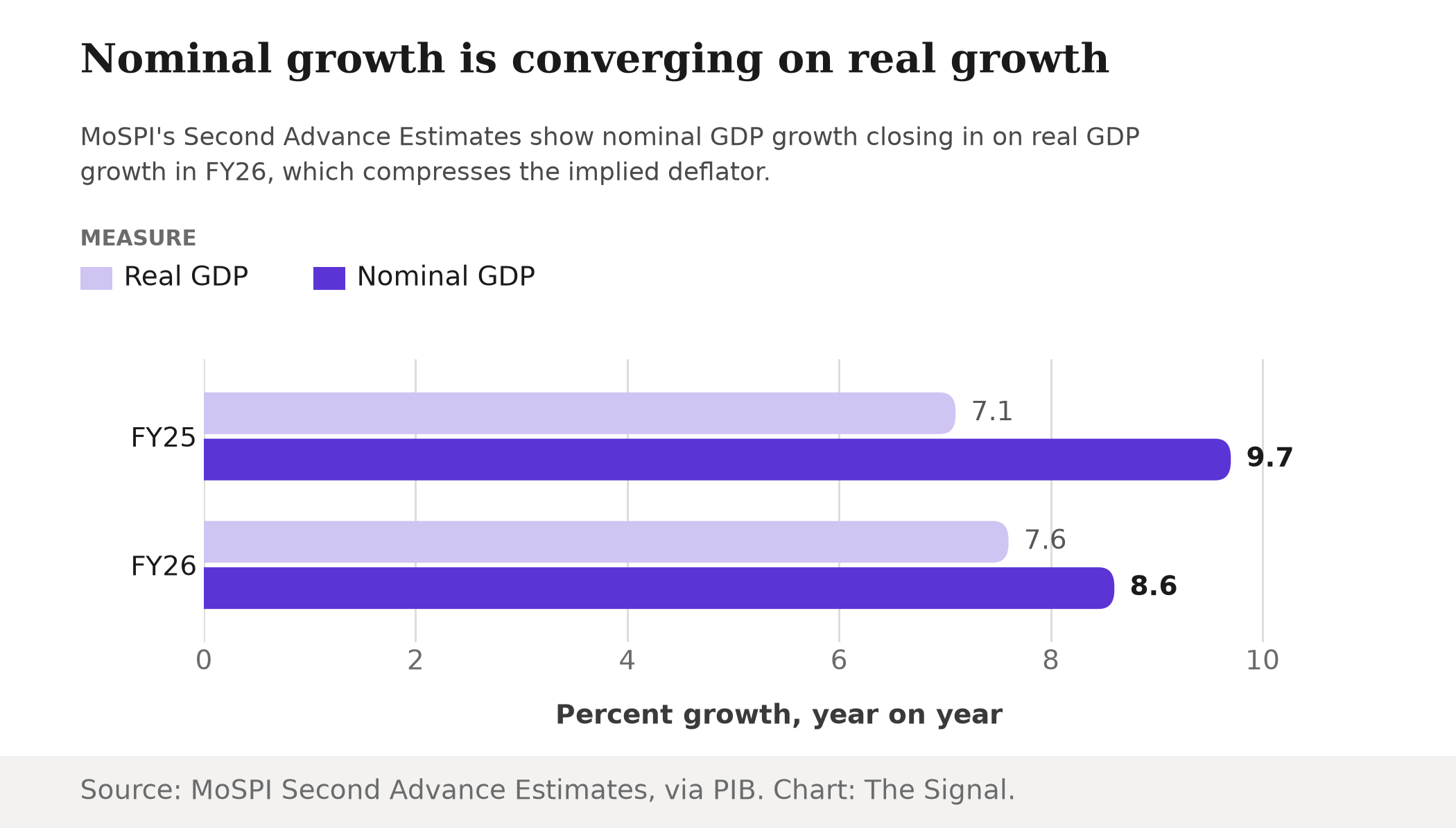

MoSPI's Second Advance Estimates, published in March for the fiscal year that closed at the end of that month, put India's real GDP growth for 2025-26 at 7.6%, edging up from 7.1% the year before (MoSPI's Second Advance Estimates report). Read only that line and the growth story looks steady: an economy compounding at roughly the same pace it managed the year before, the kind of headline a finance ministry release is built to lead with.

It is worth slowing down on the number sitting next to it. The same release puts nominal GDP growth, growth measured in the rupees that actually changed hands rather than adjusted for prices, at 8.6% for 2025-26, against 9.7% the year before (MoSPI's Second Advance Estimates report). Subtract real growth from nominal growth and what is left is the GDP deflator: the broadest gauge of how fast prices rose across everything India produced in FY26. That gap comes out to about one percentage point.

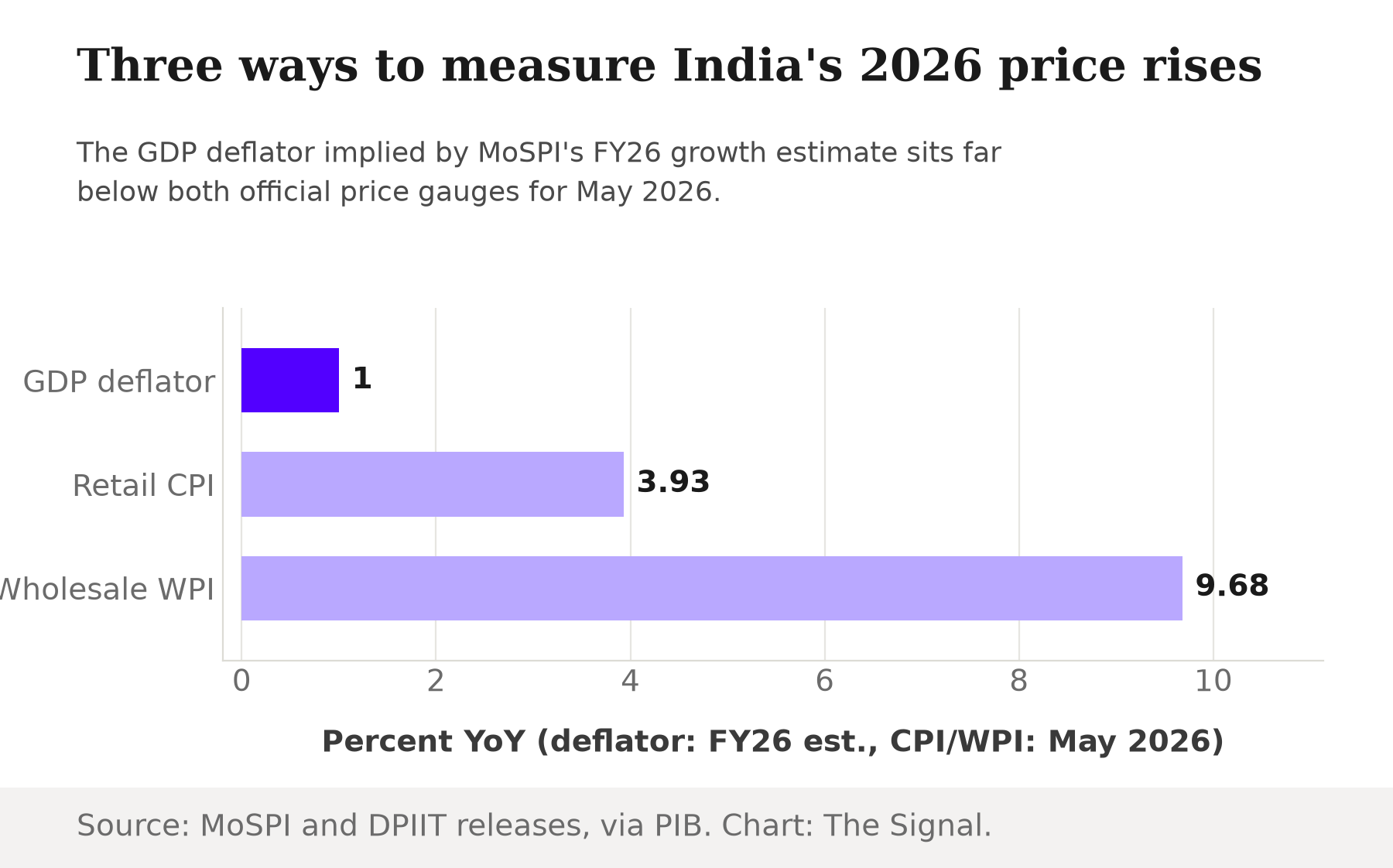

One point. That is what the government's own growth arithmetic assumes prices did this year, across every rupee of goods and services the economy produced. A year earlier, the same method implied a deflator of 2.6 points, nominal growth of 9.7% against real growth of 7.1% (MoSPI's Second Advance Estimates report). The deflator embedded in the FY26 estimate is worth well under half of what it was in FY25, a compression of 1.6 percentage points in a single year, our calculation from the same release.

Source: MoSPI's Second Advance Estimates; MoSPI's Consumer Price Index release; the Office of the Economic Adviser's WPI release. Implied deflator is The Signal's calculation. Chart: The Signal.

A deflator that compressed by more than half

The deflator is a residual, nominal growth minus real growth, so it moves whenever either side of that equation moves. Between FY25 and FY26, real GDP growth rose slightly, from 7.1% to 7.6%, while nominal GDP growth fell more sharply, from 9.7% to 8.6% (MoSPI's Second Advance Estimates report). Both changes point the same way: toward an economy whose prices, by this measure, are rising far more slowly than they were a year ago.

Source: MoSPI's Second Advance Estimates. Chart: The Signal.

Nominal GDP in rupee terms tells the same story. The government's estimate puts nominal GDP at ₹345.47 lakh crore for FY26, against ₹318.07 lakh crore for FY25 and ₹289.84 lakh crore for FY24 (MoSPI's Second Advance Estimates report): a nominal growth rate that has now slowed for two straight years, from 11.0% to 9.7% to 8.6%.

It is not a one-year blip. FY24's real GDP growth came in at 7.2% against that same 11.0% nominal growth, an implied deflator of about 3.8 points, per MoSPI's own Provisional Estimates of GDP for FY26 (MoSPI's Provisional Estimates of GDP for FY26 report). Line up three years and the implied deflator has been shrinking every year: about 3.8 points in FY24, 2.6 points in FY25, and now near one point in FY26. That same Provisional Estimates release, published 5 June 2026, is also the first revision of the FY26 figures used above: it nudges real GDP growth for FY26 up to 7.7% and nominal growth up to 8.9% (MoSPI's Provisional Estimates of GDP for FY26 report), an implied deflator of about 1.2 points. The revision moved the gap slightly wider, not toward the CPI or WPI readings, which is the opposite of what would resolve this cleanly.

The price data is not slowing down

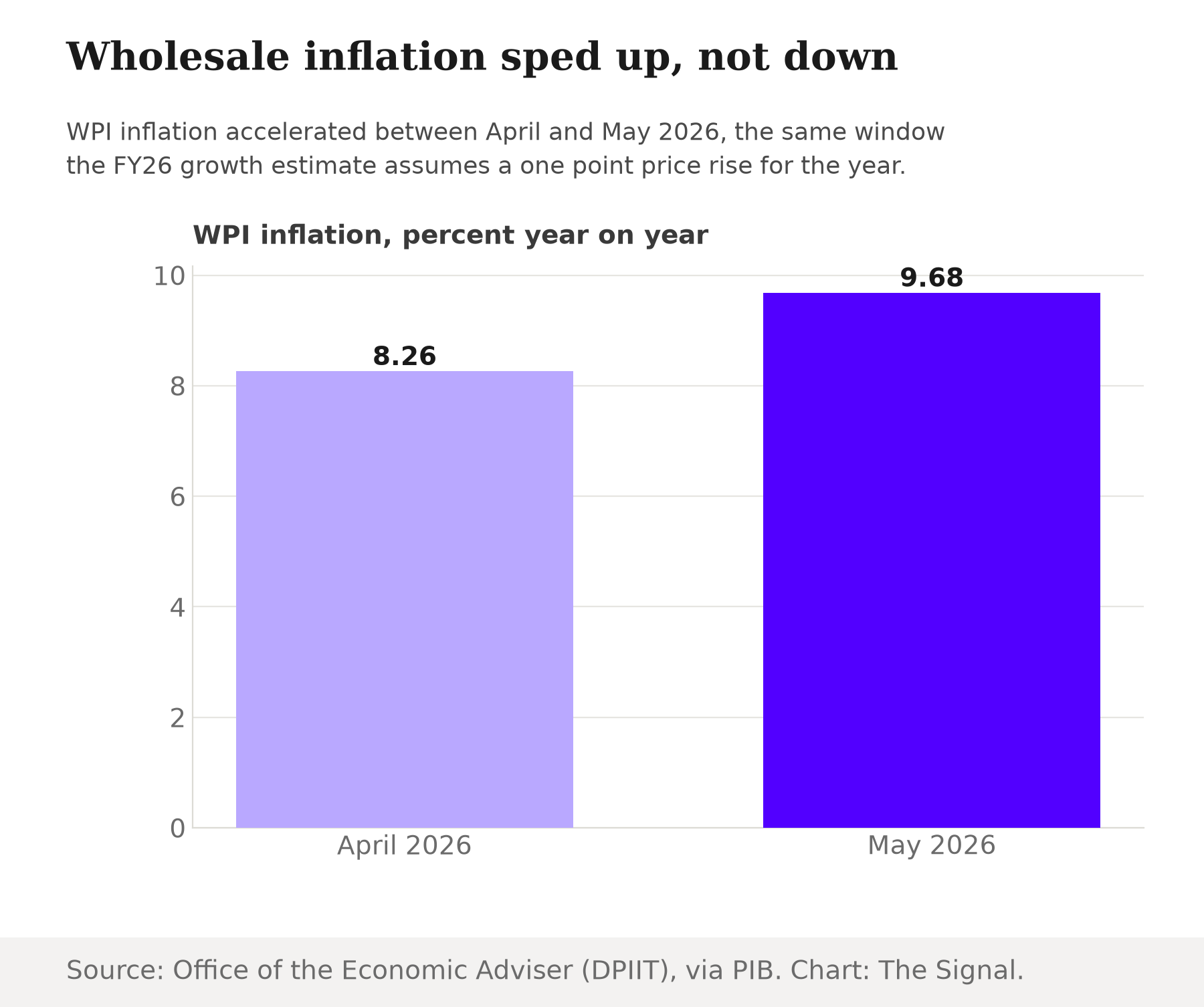

Two monthly indexes exist specifically to track how fast prices are actually moving, and both were updated for May 2026, the freshest month on record when this piece was written. Wholesale price inflation accelerated to 9.68% year-on-year in May 2026, up from 8.26% in April (the Office of the Economic Adviser's WPI release). Retail inflation, the index the Reserve Bank of India actually targets, came in at 3.93% year-on-year in May 2026, with rural inflation at 4.25% and urban inflation at 3.53% (MoSPI's Consumer Price Index release).

Source: the Office of the Economic Adviser's WPI release. Chart: The Signal.

Both readings sit well above the roughly one point of price rise the FY26 growth estimate assumes for the whole economy. The RBI's own mandate frames how wide that gap is: its inflation-targeting framework sets a 4% CPI target with a tolerance band running from 2% to 6% (the RBI's own account of its mandate), a target the government has just extended, reaffirming the 4% goal and the 2-6% band for the five years from April 2026 to March 2031 (Trading Economics reports). Even the floor of that band, 2%, is double the roughly one point the FY26 estimate implies.

Three official measures of India's prices, one number apart.

| Measure | Latest reading | Period | Source |

|---|---|---|---|

| Implied GDP deflator | About 1.0 percentage point | FY26 (2025-26), Second Advance Estimate | MoSPI |

| Retail inflation (CPI) | 3.93% | May 2026, year on year | MoSPI |

| Wholesale inflation (WPI) | 9.68% | May 2026, year on year | Office of the Economic Adviser, DPIIT |

| RBI's target band | 2% to 6% | April 2026 to March 2031 | Reserve Bank of India |

Source: MoSPI's Second Advance Estimates and Consumer Price Index release; the Office of the Economic Adviser's WPI release; the RBI's inflation-targeting mandate, extended through 2031 per Trading Economics. Chart: The Signal.

The honest objection

The strongest case against reading too much into this is that the GDP deflator is not the CPI or the WPI, and it was never supposed to move in lockstep with either. The deflator prices everything domestically produced: capital goods, government services, agriculture, exports net of imports, weighted by what the economy actually produced, not by what a household buys at retail or a trader buys at wholesale. A shift in the mix of output, or a swing in the terms of trade, can pull the deflator away from the consumer or wholesale gauge for a year without either number being wrong.

That case is real, but it does not stretch to cover a gap this wide. A deflator of about one point sitting beside a CPI of 3.93% and a WPI of 9.68% is not a small composition effect (MoSPI's Second Advance Estimates report; MoSPI's Consumer Price Index release; the Office of the Economic Adviser's WPI release). It would mean the parts of the economy that CPI and WPI do not survey, investment goods, government output, net exports, somehow got cheaper by enough to offset the price rises both surveyed baskets are recording. That is a lot of weight for one unexamined line item to carry.

The Signal

The FY26 figures are still not a final account. The first revision has already landed: MoSPI's Provisional Estimates, published 5 June 2026, nudged the implied deflator from about 1.0 point to about 1.2, not toward the CPI or WPI readings that sit far above it (MoSPI's Provisional Estimates of GDP for FY26 report). Two further revisions are still to come before the figure is treated as settled. Watch which way each one moves it. If a later revision pulls the deflator up toward what the retail and wholesale gauges are already showing, the FY26 growth figure itself was too generous: some of that reported output was really just prices rising, counted as if it were more goods and services produced. If the deflator holds near its current level, MoSPI will have to explain a composition effect wide enough to cover the entire gap on its own.

The RBI's own forward guidance does not expect the gap to close from the price side. Its June 2026 policy statement projects CPI inflation of 5.1% for FY27, rising from 4.2% in the first quarter to 5.9% in the third, with core inflation, which strips out volatile food and fuel, projected at 4.7% for the year (the RBI's Monetary Policy Committee statement). That is the central bank's own house view of where prices are headed, and it sits nowhere near the roughly one point a year the growth arithmetic has been implying. Either way, the number worth watching next is not the growth rate. It is what happens to the gap underneath it.

Reporting basis: the real and nominal GDP growth rates, the nominal GDP levels for FY24 through FY26, and the implied GDP deflator for FY25 and FY26 are all from MoSPI's Second Advance Estimates of National Income, via the Press Information Bureau. FY24's real GDP growth, and the revised FY26 real and nominal GDP growth, are from MoSPI's Provisional Estimates of GDP for FY26, published 5 June 2026. Wholesale price inflation for April and May 2026 is from the Office of the Economic Adviser's WPI release, DPIIT, via PIB. Retail inflation for May 2026 is from MoSPI's Consumer Price Index release, via PIB. The RBI's inflation-targeting mandate is per the RBI's own account of its framework, and its extension through March 2031 is per Trading Economics, the only source for that extension. The FY27 inflation and growth projections are from the RBI's Monetary Policy Committee statement of June 2026. The implied deflator figures, the year-on-year compression from FY24 through FY26, and the comparisons against the CPI, WPI and RBI band are The Signal's calculations from those releases.