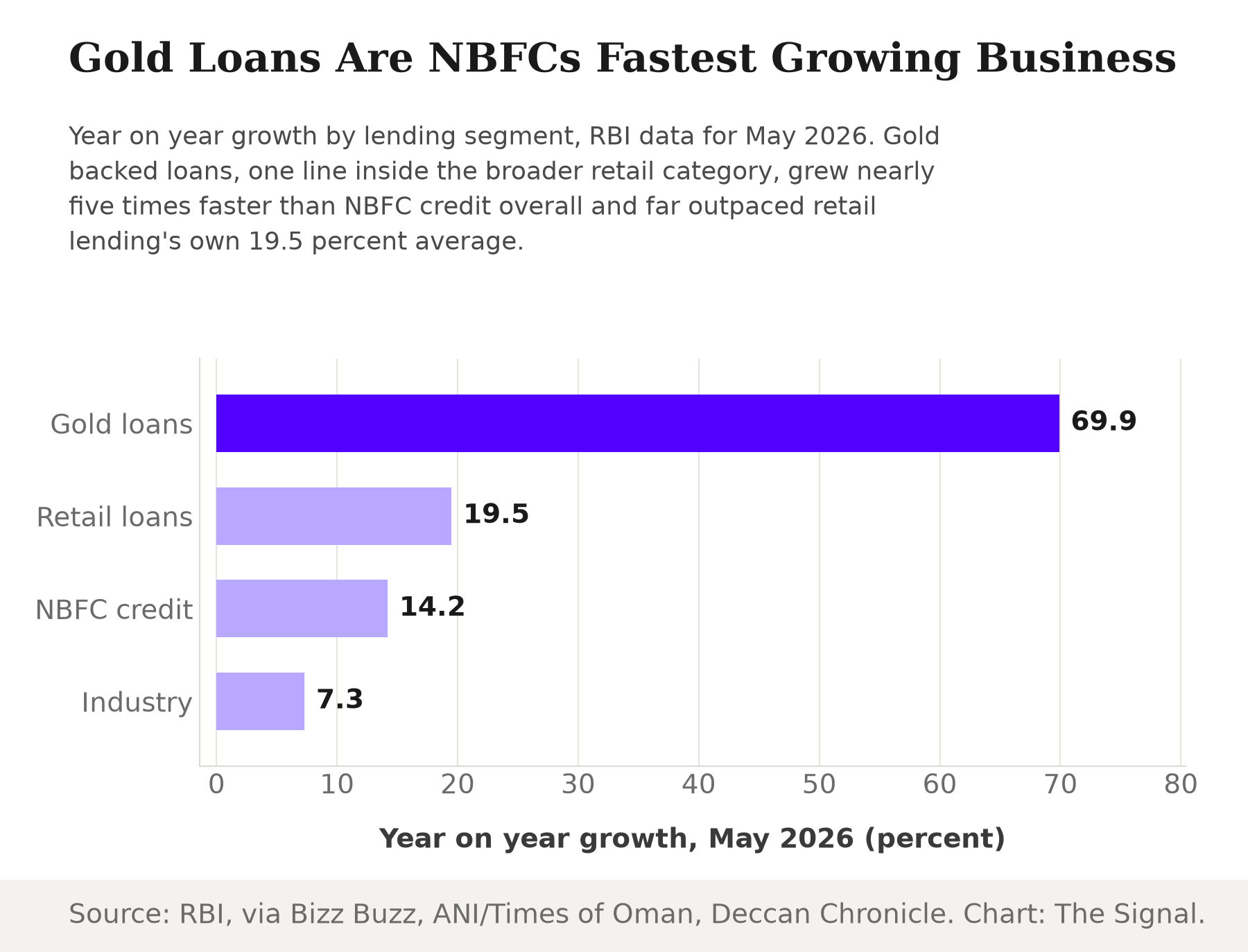

On July 7, 2026, the Reserve Bank of India released its Sectoral Deployment of Credit by NBFCs for May 2026, and the headline read like ordinary credit growth. NBFC credit grew 14.2 percent year on year in May 2026, up from 11.4 percent a year earlier, across a sample covering non-bank lenders in the Upper and Middle Layers plus housing finance companies, about 87 percent of the sector's total credit. Retail lending led that growth: retail loans expanded 19.5 percent year on year in May 2026, against 14.9 percent a year earlier. One line inside that retail bucket moved far faster than any of it. Outstanding NBFC loans against gold jewellery jumped 69.9 percent year on year in May 2026, to nearly Rs 3.29 lakh crore from Rs 1.94 lakh crore a year earlier, the fastest growth of any segment the RBI tracks. Read at face value, the story writes itself: Indians are pledging gold at an extraordinary rate, and that is either a credit boom or a distress signal.

Source: RBI, as also carried by Times of Oman, Bizz Buzz and Deccan Chronicle. Chart: The Signal.

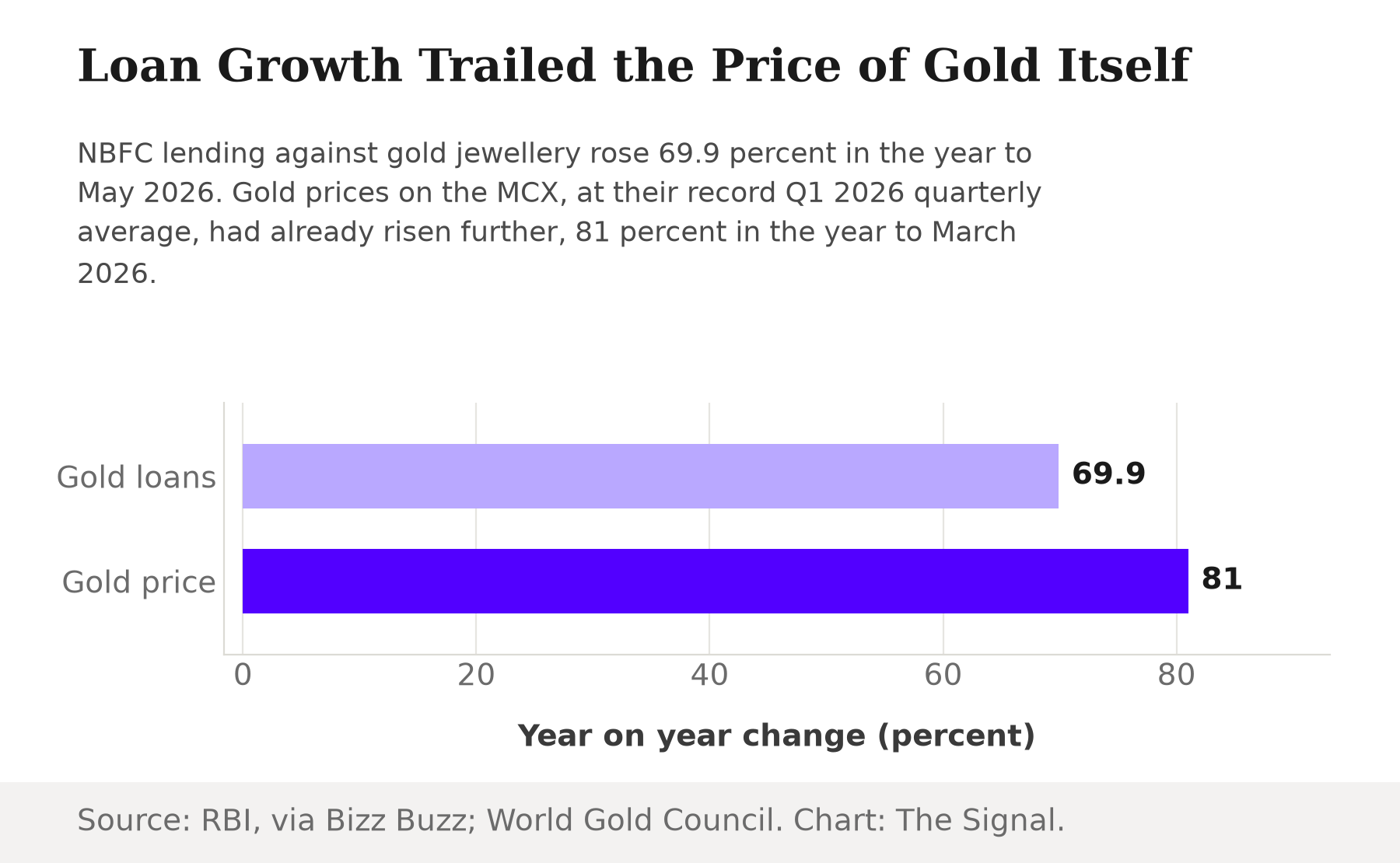

It is worth slowing down on that read. The World Gold Council's India Gold Demand Trends report put MCX gold spot prices at a record Q1 2026 quarterly average of Rs 151,108 per 10 grams, up 81 percent year on year. The metal behind these loans, measured to the March 2026 quarter, had already climbed in price faster than the loan book grew to May 2026. A lender holding the exact same weight of pledged gold twelve months apart would record a much bigger loan book today without a single additional gram walking through the door.

Source: RBI, via Bizz Buzz; World Gold Council. Chart: The Signal.

The rule that never moved

There is a second reason gold loans specifically absorbed this shift, and it predates the price run by two years. In November 2023, the RBI raised the risk weight on unsecured consumer-credit exposure at banks and NBFCs from 100 percent to 125 percent, making unsecured retail lending costlier to hold in regulatory capital. The same notification explicitly carved out loans against gold jewellery, along with microfinance and self-help group (SHG) loans for NBFCs, from that higher weight. In February 2025, the RBI reversed course specifically on microfinance, cutting its risk weight back to 100 percent, easing the same tightening that had briefly reached that segment. Gold's exclusion is the one thing that did not move across either notification: it was written into the rule in November 2023 and was still standing, untouched, when RBI revisited the same list in February 2025. For at least that fifteen-month stretch, gold loans were the cheapest large retail category an NBFC could grow in capital terms, while unsecured consumer credit sat at the higher weight throughout.

That leniency on capital was never touched, but a separate rulebook on how gold loans get written was tightening at the same time. In June 2025, the RBI issued a single harmonised framework for lending against gold and silver collateral, covering banks and NBFCs alike, with compliance required no later than April 1, 2026, a new conduct-and-valuation regime landing on lenders' books just five weeks before the May 2026 print this piece is built on. It governs how a loan against gold gets valued and documented, not what it costs in regulatory capital, so it sits alongside the capital-weight advantage rather than undoing it. But it is a reminder that the regulatory environment around gold loans was still actively moving in mid-2026, not settled two years ago and left alone.

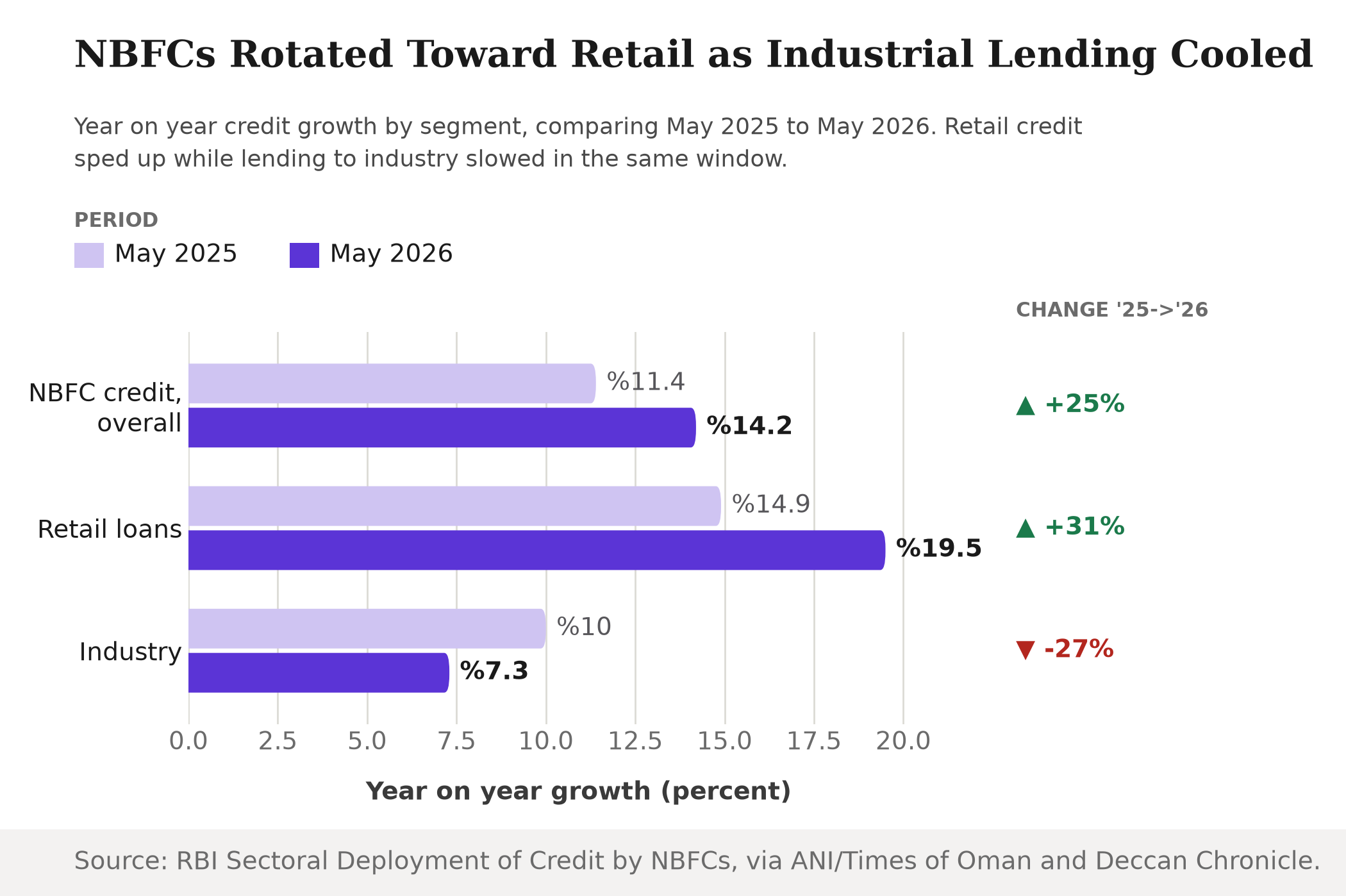

Retail up, industry down

The rotation shows up on the other side of the ledger too. Credit growth to industry slowed to 7.3 percent year on year in May 2026, down from 10.0 percent a year earlier, even as retail lending and gold-backed loans both sped up. Gold loans, one line inside that retail bucket, grew more than three and a half times faster than retail lending's own blended rate and nearly ten times faster than lending to industry, in the same May 2026 print.

Retail and gold-backed lending both accelerated even as industry credit growth slowed.

| Segment | May 2025 (YoY) | May 2026 (YoY) |

|---|---|---|

| NBFC credit, overall | 11.4% | 14.2% |

| Retail loans | 14.9% | 19.5% |

| Industry | 10.0% | 7.3% |

| Gold backed loans | not reported | 69.9% |

Source: RBI, via Times of Oman, Deccan Chronicle and Bizz Buzz.

Two listed NBFCs show the same rotation lender by lender, in the same window the RBI's aggregate figures cover. Muthoot Finance, India's largest gold-loan NBFC, reported its highest-ever consolidated Gold Loan AUM of Rs 1,65,000 crore for the quarter ended March 2026, up 54 percent year on year. Manappuram Finance's consolidated AUM rose 48.3 percent year on year to Rs 63,798 crore in the same quarter, led by 99.1 percent year-on-year growth in its gold loan book alone. Neither company's own number is the RBI's sector-wide figure, but both move in the same direction at a similar pace, which is what a sector-wide rotation should look like at the individual-lender level.

The honest objection

The strongest case against a purely mechanical reading is that pledging gold for a loan is a well-worn response to financial stress in India, whether from a wedding, a medical bill or a working-capital gap at a small business, and a genuine 69.9 percent rise in the outstanding book, price effects aside, still means many more households or small enterprises found it worthwhile to borrow against family gold this year than last. Nothing in the RBI's release, the two risk-weight notifications, or the World Gold Council's price series says why any individual borrower walked into an NBFC branch, and that gap in the evidence is real.

One data point cuts against the freshest version of that story. Only around 6 percent of gold loan originations are from new-to-credit borrowers, per the RBI's Financial Stability Report as analysed by Elara Securities, implying most of the growth in this book is existing borrowers rather than a fresh wave of households pledging gold for the first time. That does not settle whether repeat borrowing itself reflects distress, a wedding season or investment-linked demand against a rising asset, since the evidence does not say why any of them came back. It only weighs against the specific claim that a new cohort of households turned to gold out of desperation this year.

But that case does not explain why the growth concentrated in gold and retail while credit to industry cooled to 7.3 percent in the very same window. A pure demand shock from household distress would not, on its own, predict which side of an NBFC's book grew and which slowed. A supply-side shift, in which lenders rotate fresh capital toward the product regulation makes cheapest to write, predicts exactly that split: faster gold and retail, slower industry, all at once.

The Signal

The number this release will be covered for is the 69.9 percent surge in gold loans. The number that explains it is the 81 percent rise in the gold price itself, what the collateral was already worth before a single new loan got written, plus a capital rule, in place since November 2023 and still standing as of the RBI's February 2025 review, that makes gold the cheapest large retail category for an NBFC to grow. Neither figure alone answers whether Indian households are more willing to pledge the family gold or more desperate to. What both together show is that NBFCs did not need either answer to grow this book: a price that outran the loans it backs, and a rule that has favoured gold over unsecured credit for two and a half years, were enough by themselves. Watch the next print for whether the growth rate holds once gold prices stop climbing. If the book keeps expanding near 69.9 percent after the metal's price flattens, that is the moment the household-distress story starts to look real rather than mechanical.

Reporting basis: the May 2026 NBFC credit and gold-loan growth figures are from the Reserve Bank of India's Sectoral Deployment of Credit by NBFCs release, as also carried by Bizz Buzz, an ANI wire via Times of Oman, and Deccan Chronicle; all three outlets recarry the same RBI release, so they count as one origin, not three. The risk-weight history is from two RBI notifications, RBI/2023-24/85 and RBI/2024-25/119; the newer conduct-and-valuation framework is from RBI/2025-26/47. The gold-price figures are from the World Gold Council's India Gold Demand Trends release for the first quarter of 2026. The named-lender figures are from Muthoot Finance's and Manappuram Finance's own Q4 FY26 results, as carried by Whalesbook and TradingView/Quartr respectively. The new-to-credit-borrower share is from Business Today's report on Elara Securities' analysis of the RBI's Financial Stability Report. The comparison between gold-loan book growth and gold-price growth, and every ratio between segment growth rates, are The Signal's own calculations from those figures.