UNCTAD's newly published World Investment Report 2026 gives India a genuine promotion. India rose two places to become the world's 11th-largest recipient of foreign direct investment in 2025, up from 13th in 2024. The number behind that climb is sharper still: India's FDI inflows rose 44 percent to $38.9 billion in 2025, from $27.1 billion in 2024. Read as a headline, it says global capital is choosing India faster than it is choosing almost anywhere else.

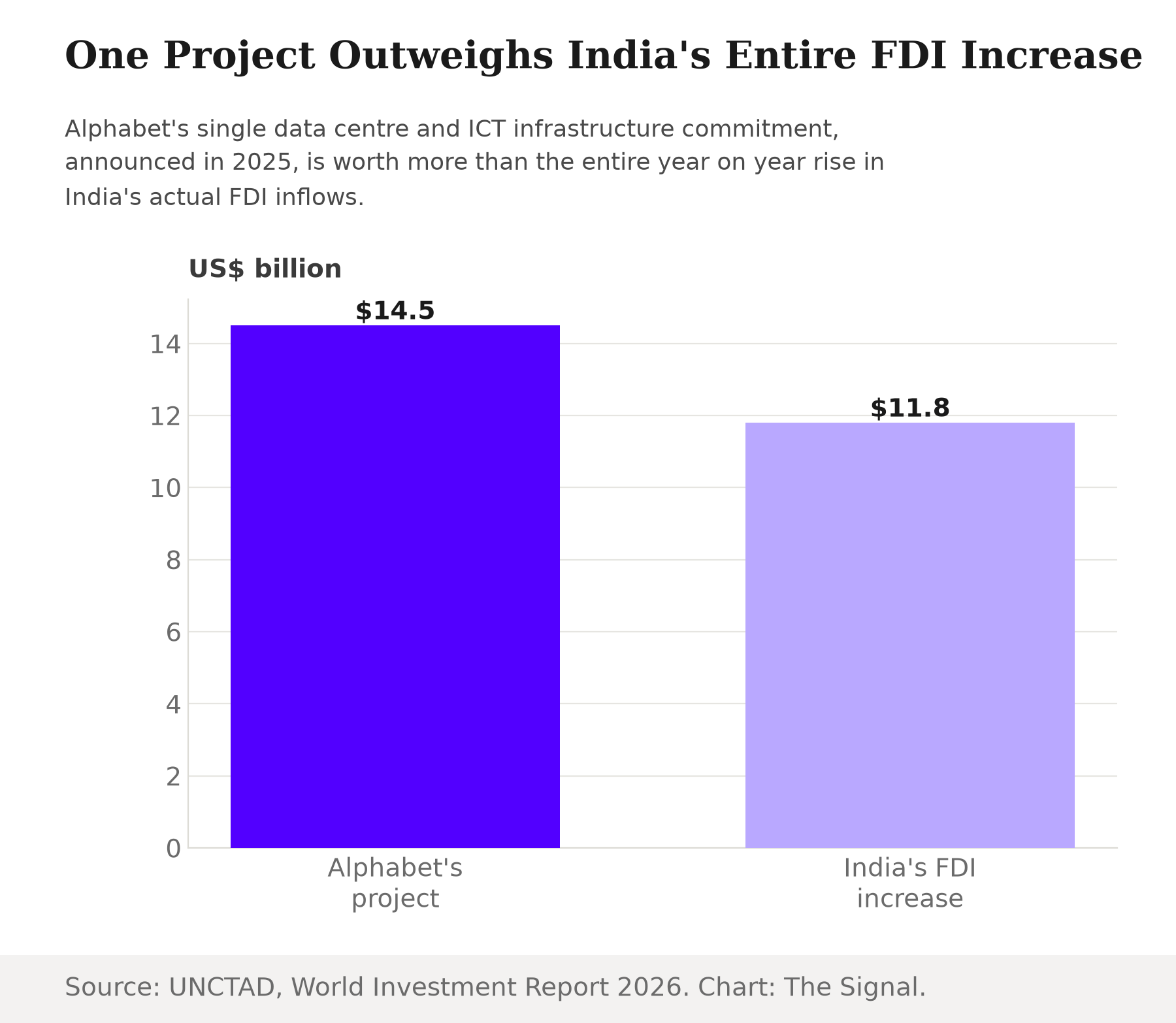

It is worth slowing down on that. Alphabet's $14.5 billion data-centre and ICT infrastructure commitment in India was the single largest greenfield investment project announced anywhere in developing Asia in 2025. That is not a footnote to India's FDI ranking. It is close to being the whole story.

This is not a generic ICT build-out. UNCTAD's own account of the project describes it as data-centre capacity built, alongside associated renewable-energy development, specifically to support AI and cloud-computing demand, sited in Visakhapatnam. India's IT ministry puts a number and a clock on it: an approximately $15 billion AI-infrastructure investment, deployed in phases over five years, from 2026 to 2030. That timeline matters for reading the 2025 numbers: the disbursement window UNCTAD's project value is drawn from had barely begun as of the FDI data used in this piece. Most of the actual capital is still ahead, not behind, the 2025 figures.

The single project is worth more than the entire annual increase. India's actual FDI inflows rose from $27.1 billion in 2024 to $38.9 billion in 2025, a gain of $11.8 billion. Alphabet's announced project alone was valued at $14.5 billion. The two figures measure different things: one is money that has already landed, the other is a project pledge. But the scale comparison is the point: a single announcement is bigger than the entire year-on-year rise in India's realised FDI.

A pipeline that was shrinking, not growing

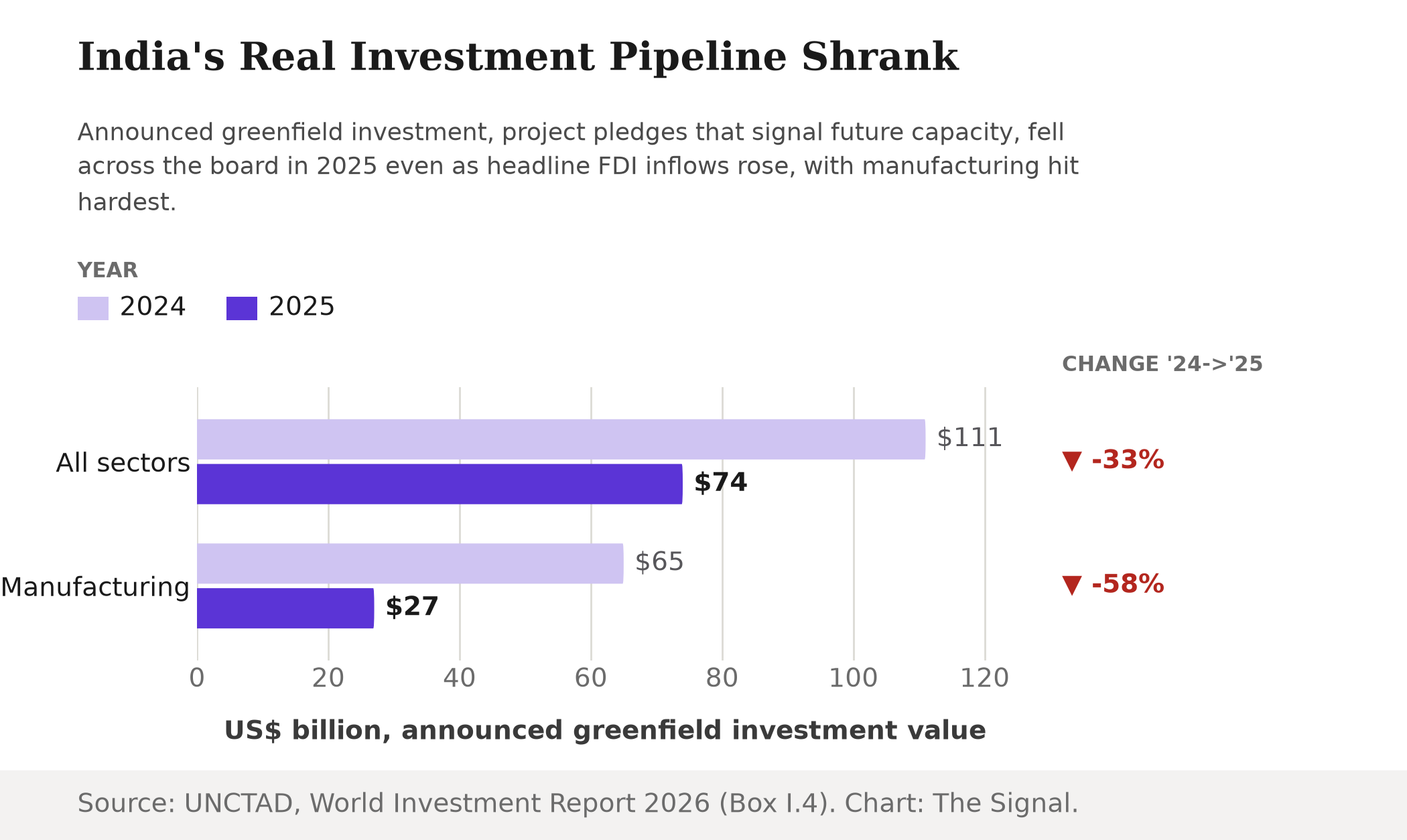

The ranking jump describes inflows that have already been counted. It says nothing about what comes next, and what comes next looks worse. Even as headline FDI inflows to India rose to $39 billion in 2025, announced greenfield investment into India fell from more than $111 billion in 2024 to about $74 billion, a decline of roughly a third in the value of new projects being pledged for the years ahead. The drop was not spread evenly. Manufacturing-specific greenfield investment announcements in India fell from about $65 billion in 2024 to $27 billion in 2025, a fall of more than half in the one category India's industrial policy has spent a decade trying to build up.

Greenfield announcements are a leading indicator: the pipeline of factories, plants and campuses that eventually turn into capacity, jobs and, years later, more FDI. India's 2025 ranking rose on money that had already arrived, in the same year the pipeline of money committed to arrive later kept shrinking.

That $74 billion pipeline figure and the Alphabet project are not separate figures: the pipeline almost certainly contains the project. Information and communication technologies became India's largest greenfield sector in 2025, the same category Alphabet's data-centre commitment sits in, and both that sectoral breakdown and the $14.5 billion project figure itself are drawn from the same underlying project database. Strip the single largest project out of a pipeline that already fell by a third, and the shrinkage in everything else India is attracting looks sharper still, not milder.

Why one project can move a country's whole ranking

The pattern goes beyond India. It is what happens to FDI rankings once investment itself is dominated by a small number of very large projects. Megaprojects worth $1 billion or more accounted for about 44 percent of the total value of global announced greenfield investment in 2025, up from 22 percent in 2017: the share held by billion-dollar-plus projects has doubled in eight years. UNCTAD draws the direct consequence itself: the growing dominance of megaprojects distorts country and regional FDI patterns, since one or two projects can dominate a country's total inflows. India in 2025 is close to a textbook case of the pattern UNCTAD is describing about the global data.

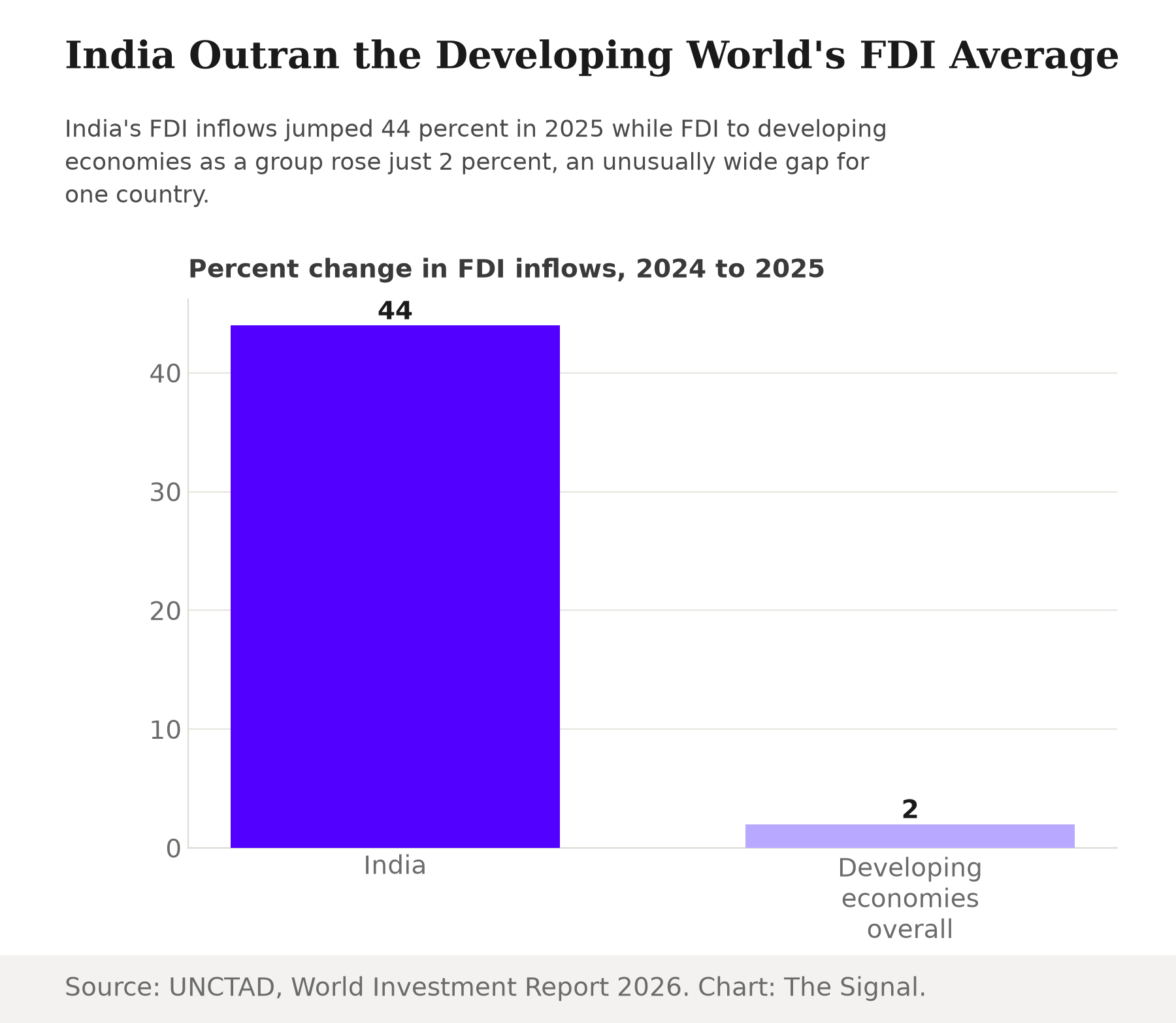

FDI inflows to developing economies overall rose just 2 percent, to $901 billion, in 2025, against India's 44 percent rise, India grew roughly 22 times faster than the developing-world average.

A gap that wide, in a world where a single megaproject can swing a country's total, is exactly the kind of number UNCTAD's own methodology note is warning readers not to over-read.

The rank move was not confined to inbound investment either. India's outward FDI rose 47 percent to $35.7 billion in 2025 from $24.3 billion in 2024, lifting it two places to 18th among the world's top home economies for FDI, from 20th. The same year produced a matching two-place jump on both sides of India's ledger.

| 2024 rank | 2025 rank | Change | |

|---|---|---|---|

| Inbound FDI recipient | 13th | 11th | +2 |

| Outbound investor (home economy) | 20th | 18th | +2 |

Source: UNCTAD, World Investment Report 2026, Figures I.4 and I.5.

The honest objection

The strongest case against calling this a mirage is that 2025 was a genuinely good year for FDI everywhere, not just in India. Global FDI rose 6 percent to $1.6 trillion in 2025, ending two consecutive years of decline, and developing economies as a group grew too, even if only 2 percent. On this view India is not manufacturing an illusion out of nothing; it is riding a real global upswing, and whatever its source, the money genuinely arrived. A dollar of realised FDI does not stop counting because it happens to be concentrated in one deal.

That case is real, but it explains the wrong number. It accounts for why inflows could rise at all in 2025. It does not explain why India's pipeline of announced future projects shrank in the very year its ranking improved. A country riding a genuine, broad-based investment wave should show a rising pipeline alongside rising inflows. India showed the opposite pairing, and UNCTAD's own warning that one or two projects can dominate a country's total inflows describes precisely the mechanism that can produce it.

The Signal

India's FDI ranking improved in 2025 for a real reason: a single very large, very real commitment from one company. That is worth having. It is not, on this data, evidence that the broader universe of investors is newly convinced about India, because the pipeline behind that ranking was shrinking at the same time. The number to watch next year is not the ranking. It is whether another megadeal lands to keep the rank afloat, or whether the pipeline keeps shrinking with nothing large enough left to mask it. A ranking built on one company's decision can unbuild itself just as fast.

Reporting basis: most figures in this piece, the FDI ranking and inflow figures, the Alphabet greenfield project, the greenfield investment declines, the megaproject share, the developing-economy and global FDI totals, and India's outward investment ranking, come from a single origin, UNCTAD's World Investment Report 2026, published July 7, 2026, covering calendar-year 2025 data. The AI-specific framing and investment timeline for the Alphabet project come from India's Ministry of Electronics and Information Technology. The net increase in India's FDI inflows and the ratio of India's growth rate to the developing-economy average are The Signal's calculations from those figures.