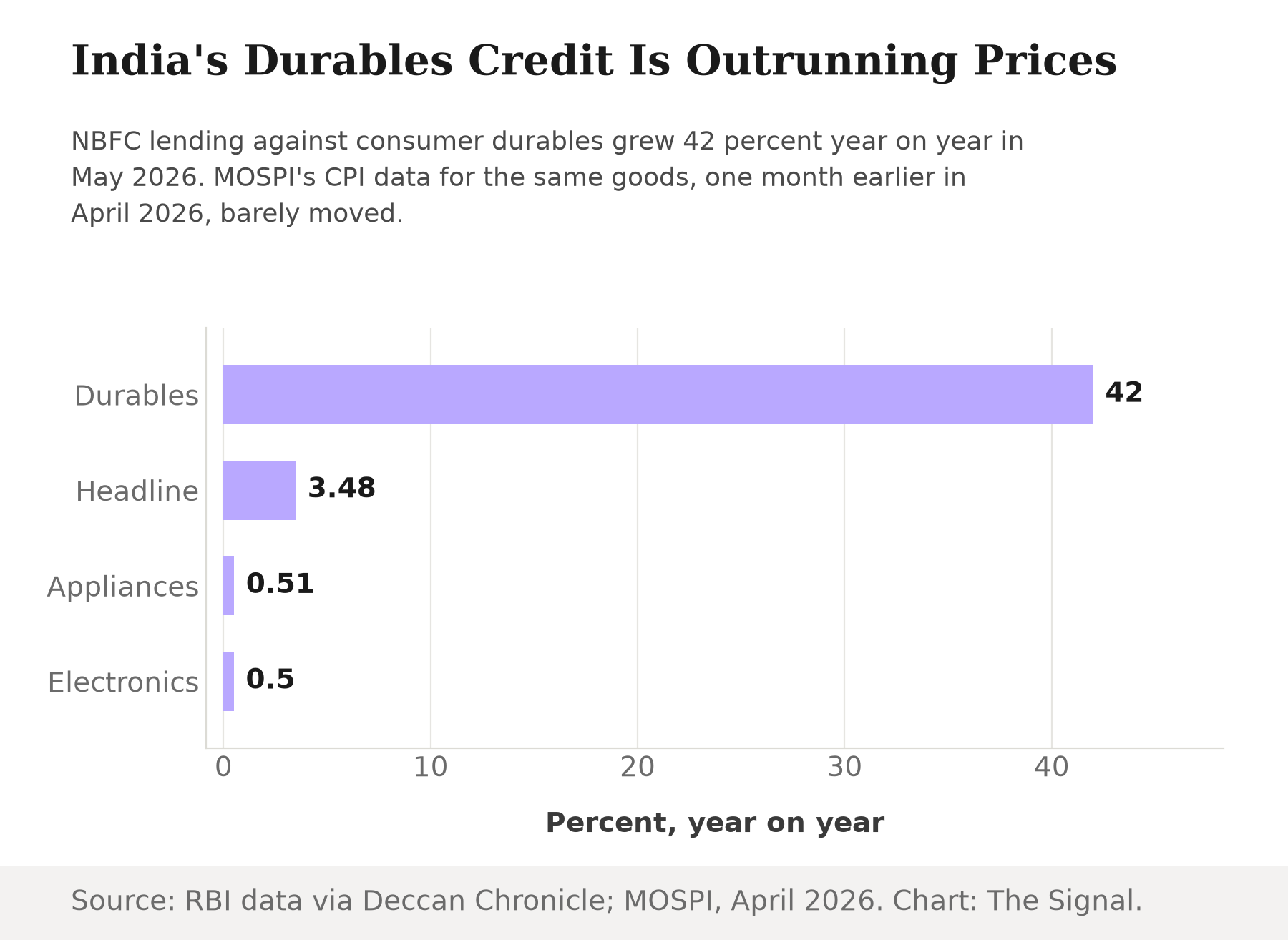

India's household borrowing accelerated hard again in the middle of 2026. Personal loan growth reached 15.4 percent year-on-year in the fortnight ended May 31, 2026, up from 11.1 percent a year earlier, the Reserve Bank of India's fortnightly sectoral data show. Underneath that headline sits a sharper number: outstanding NBFC credit against consumer durables surged 42 percent year-on-year in May 2026 to Rs 68,814 crore. These are the loans that finance televisions, refrigerators and similar goods, and the segment is one of the fastest-growing the central bank tracks. The easy read writes itself: electronics have gotten pricier, and Indians are borrowing more to keep buying them.

That reading matters beyond one lending segment. How a credit cycle splits between price and volume shapes what the RBI's rate-setters should watch, and what a lender pricing a new durables loan should assume about the borrower on the other end of it. That question matters more once a single segment is growing credit at 42 percent a year. A price-driven acceleration is a story about affordability eroding under people still buying the same number of goods. The alternative is a story about appetite, and about how much of that appetite is being carried on someone else's balance sheet.

It is worth checking that against what electronics actually cost. MOSPI's Consumer Price Index for April 2026 puts the "Household appliances" group up just 0.51 percent year-on-year, and the "Information and communication" division, which covers electronics and telecom equipment, up 0.50 percent over the same period. Both readings sit barely above zero, and both are well under the 3.48 percent headline retail inflation MOSPI reported for April 2026. By the government's own index, consumer durables are not getting meaningfully pricier. The credit surge is real. The price story that would explain it is not, at least not yet in the numbers that matter.

NBFC credit against durables grew 42 percent while durables prices grew about half a percent.

A credit boom broader than gadgets alone

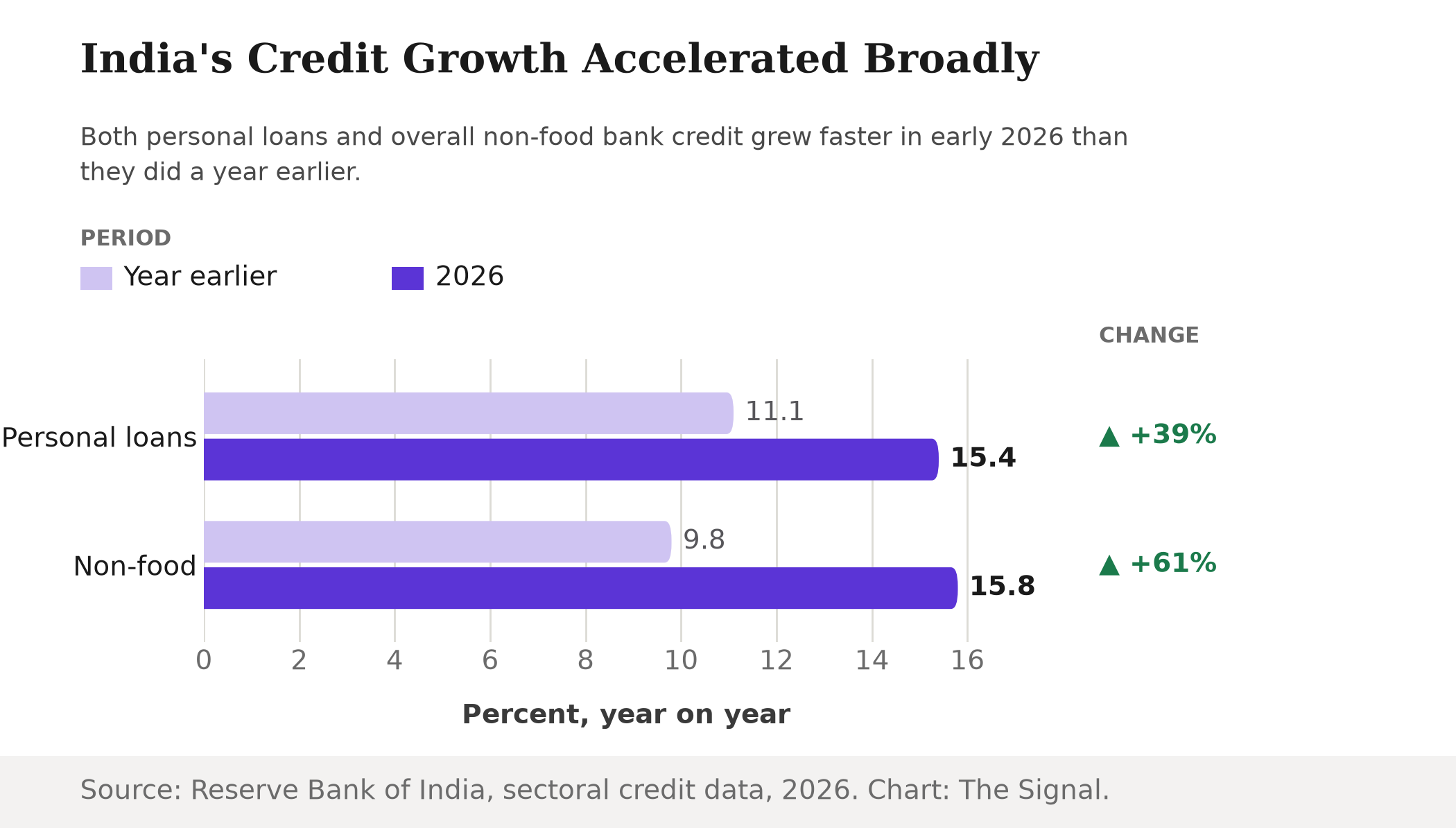

The acceleration is not confined to durables. Non-food bank credit, which excludes food-linked lending, grew 15.8 percent year-on-year in the fortnight ended April 30, 2026, up from 9.8 percent a year earlier. Personal loans specifically climbed from 11.1 percent to 15.4 percent over roughly the same window, per the RBI's fortnightly data. Credit is growing faster across nearly every category the central bank tracks, not only the durables segment financing new phones and appliances. Indians are borrowing more everywhere; durables lending is simply the fastest-accelerating slice of a broader trend.

The demand side has a face, too. Consumer durable loans are the single largest entry product for India's first-time borrowers, accounting for 32 percent of new-to-credit loan originations nationally, credit bureau CRIF High Mark's data for the twelve months to February 2026 show. Two-thirds of those durables originations come from cities beyond the top 100. Across the wider lending system, durables loans are not mainly an existing customer borrowing more; they are the single biggest gateway bringing first-time borrowers, disproportionately outside India's largest cities, into formal credit. That pattern fits a demand story better than a price one: more people gaining access to credit, not the same borrowers paying more for the same goods.

That kind of acceleration is not automatically benign. Durables loans are typically short tenure and high frequency, repaid over a year or two rather than a decade. That means a book expanding 42 percent in a year turns into a repayment question well before it turns into a price question. The stress signals so far are muted: the RBI's Financial Stability Report puts gross NPAs at just 0.7 percent for secured retail loans and 1.7 percent for unsecured retail loans, the category covering personal and consumer-durable loans, as of March 2026. The central bank's own baseline scenario expects that ratio to rise only to 1.9 percent by March 2028. But the same report cautions that an unsecured personal loan or consumer-durable loan has less protection if wages or employment weaken. The borrowing is also stacking on an already-rising base: India's household sector debt reached 45.5 percent of GDP by September 2025, with non-housing retail loans, personal, consumer-durable and gold lending combined, now making up 58.4 percent of all household borrowing. Appetite financed on borrowed money is worth watching precisely because it can turn into stress quietly, long before a price index would ever show it.

The price shock that has not reached the shelf

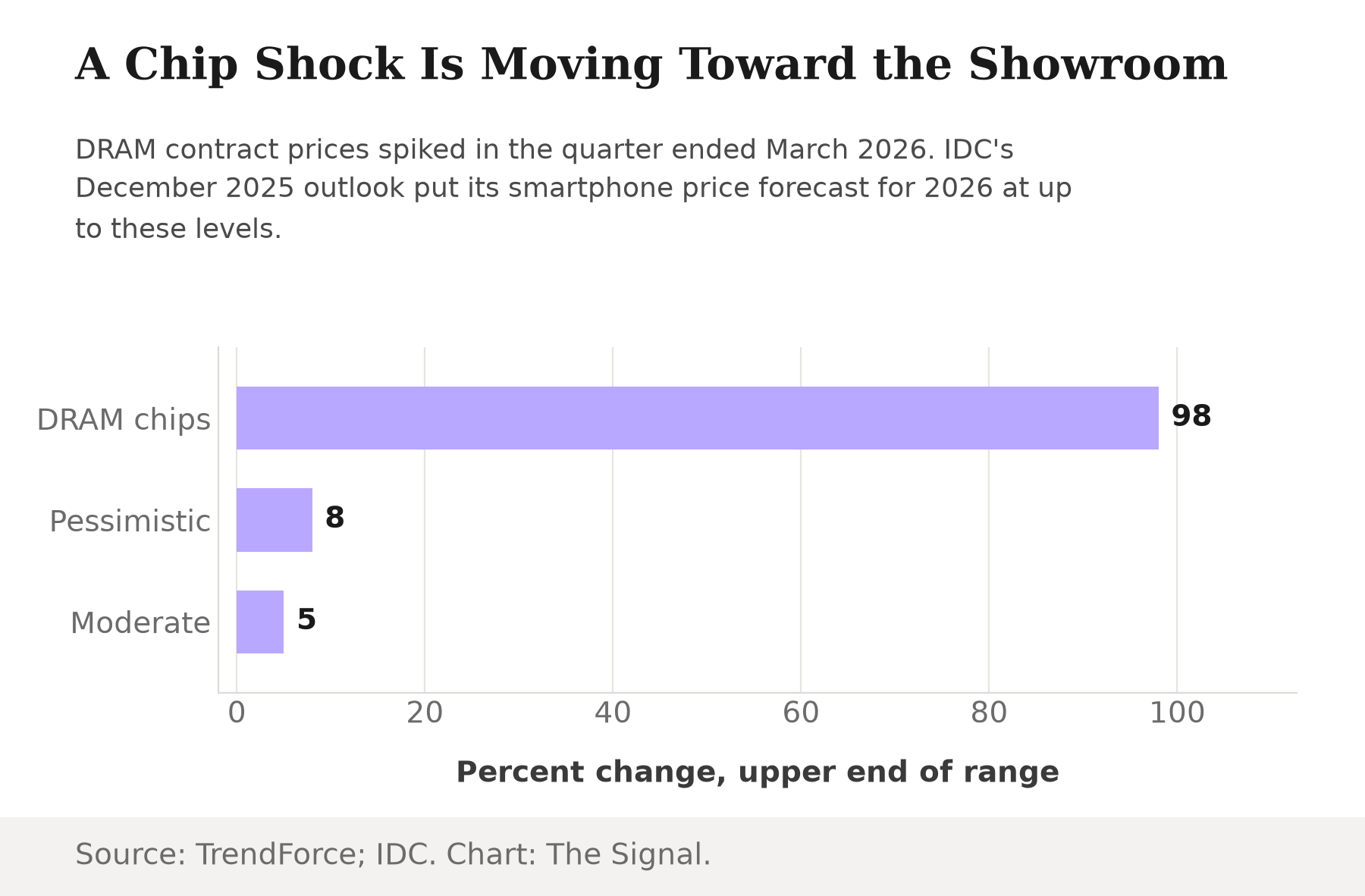

There is a real price story unfolding, just not the one the loan numbers would suggest, and not yet visible in MOSPI's index. Contract prices for conventional DRAM, the memory chips inside every phone, laptop and screen-equipped appliance, jumped roughly 93 to 98 percent quarter-on-quarter in the quarter ended March 2026, as AI data-centre buyers crowded out consumer-grade chip supply, Taiwan-based research firm TrendForce found. IDC's analysts wrote, in a December 2025 note, that the shortage could lift global smartphone average selling prices 3 to 5 percent in a moderate scenario over 2026, or 6 to 8 percent in a pessimistic one. India has already felt the leading edge of that move: Samsung's Galaxy S26 series launched in India in March 2026 with price hikes of up to Rs 10,000 per model, attributed to memory-chip cost pressure. The mechanism is straightforward: a data centre and a smartphone draw on the same DRAM factories, and when hyperscalers building out AI infrastructure are willing to pay more for a chip than a phone maker is, the phone maker either pays up or waits in line.

That shock is moving through a supply chain, not yet through a consumer price index. Chips get built into finished devices months before those devices reach a shelf. Samsung's price hike landed with the Galaxy S26 launch in March 2026, and MOSPI's freshest available print, for April 2026, still puts the "Information and communication" division at just 0.50 percent year-on-year. The mechanism that could eventually move that reading has started. The index has not caught up to it yet.

The honest objection

The strongest case against reading this as a pure volume story is that borrowers might already be front-running the price shock. If shoppers know memory-chip costs are climbing and expect the next round of phone and appliance launches to cost more, the way prices moved with Samsung's Galaxy S26 launch in March 2026, then buying now on borrowed money is a rational trade. That would make today's credit surge a price story in disguise, running ahead of the index rather than behind it.

That case holds some truth for the Galaxy S26 launch specifically. But it strains against the scale of the credit numbers. The price move reported so far is confined to Samsung's flagship Galaxy S26 line, not the broader durables market, and a single high-end phone line's price increase would move the broad "Information and communication" basket only marginally. Meanwhile non-food bank credit grew 15.8 percent broadly across the economy in the fortnight ended April 30, 2026, in categories nowhere near a memory chip. A shortage in one component of one product line cannot explain borrowing that is accelerating everywhere at once.

The Signal

India's loan numbers and its price numbers are telling two different stories this year, and conflating them is the easy mistake. The record in personal and durables lending reads as a demand story: more borrowing, not costlier borrowing. The price story is real but stuck upstream, in a chip shortage that has reached only one flagship phone line so far. Watch MOSPI's coming CPI releases. If the "Information and communication" and "Household appliances" readings start climbing, the chip shock has finally reached the shelf, and this year's credit surge will look, in hindsight, like borrowing ahead of its own price rise. If those readings stay flat, the record was always about appetite, not cost.

Reporting basis: personal loan and non-food bank credit growth are from the Reserve Bank of India's fortnightly sectoral deployment of credit releases, for the fortnights ended May 31 and April 30, 2026 respectively. NBFC lending against consumer durables is per Deccan Chronicle's reporting of RBI data for May 2026. All price figures, headline, household appliances, and information and communication, are from MOSPI's Consumer Price Index press release for April 2026. DRAM contract-price data is from TrendForce's memory-market research for the quarter ended March 2026. The smartphone price forecast is from IDC's December 2025 analysis. The Galaxy S26 pricing details are as reported by Business Today. Retail loan asset-quality and household debt-to-GDP figures are from the RBI's Financial Stability Report of June 2026, as reported by Policy Circle and the Risk Management Association of India. First-time borrower and city-tier lending data is from CRIF High Mark's April 2026 new-to-credit report. No figure in this piece is The Signal's own calculation.