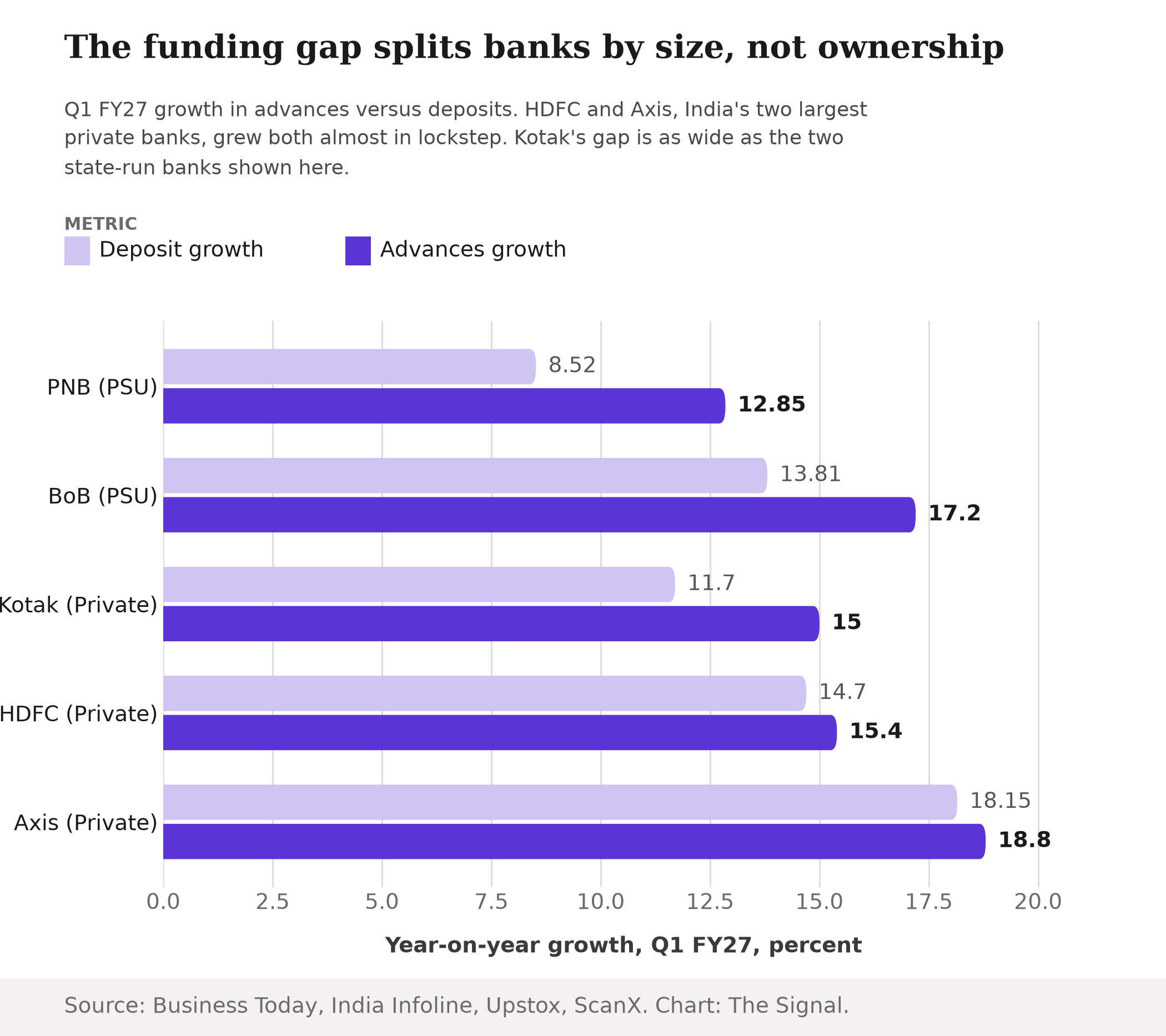

Every large Indian bank that reported Q1 FY27 provisional numbers in the first week of July 2026 told a version of the same story: loans grew faster than deposits. HDFC Bank's gross advances rose 15.4% year-on-year to Rs 30.61 lakh crore in the quarter ended June 30, 2026, while deposits grew 14.7% to Rs 31.70 lakh crore. Axis Bank posted a similarly tight scorecard: gross advances up 18.8% against deposits up 18.1 to 18.2%. Set those two against Bank of Baroda, whose global advances grew 17.2% to Rs 14.17 lakh crore while global deposits grew 13.81% to Rs 16.34 lakh crore, and Punjab National Bank, whose global advances climbed 12.85% to Rs 12,75,036 crore while global deposits rose just 8.52% to Rs 17,24,840 crore. The obvious read writes itself: private banks are winning the deposit race, and the state-run banks are the ones falling behind.

It is worth slowing down on that. Kotak Mahindra Bank, a private bank with no state ownership, posted credit growth of 15% against deposit growth of just 11.7% in the same quarter, a gap wider than Bank of Baroda's and nearly as wide as Punjab National Bank's. A private bank just produced a public-sector-shaped balance sheet.

Kotak's funding gap now sits closer to a PSU bank's than to fellow private lender HDFC's.

Ownership doesn't organize this quarter's results. The size of the gap between a bank's credit growth and its deposit growth does, and that gap tracks deposit-franchise strength, not who holds the largest shareholding. HDFC's advances-to-deposits gap ran about 70 basis points, and Axis's ran about 60 to 70 basis points, while Kotak's gap of roughly 330 basis points sat closer to Bank of Baroda's roughly 339 and Punjab National Bank's roughly 433 than to its fellow private lenders'.

| Bank | Ownership | Advances growth (YoY) | Deposit growth (YoY) | Gap |

|---|---|---|---|---|

| Punjab National Bank | Public sector | 12.85% | 8.52% | ~433 bps |

| Bank of Baroda | Public sector | 17.2% | 13.81% | ~339 bps |

| Kotak Mahindra Bank | Private | 15% | 11.7% | ~330 bps |

| HDFC Bank | Private | 15.4% | 14.7% | ~70 bps |

| Axis Bank | Private | 18.8% | 18.1-18.2% | ~60-70 bps |

Source: Business Today, India Infoline, Upstox and ScanX, citing each bank's Q1 FY27 provisional business update. Gap column is The Signal's calculation from those figures.

A wider, older gap

Zoom out from single banks to the whole system and the gap is similarly wide, and considerably older. Systemic non-food bank credit grew 17.4% year-on-year in the fortnight ended May 31, 2026, more than double the 8.8% pace of the same fortnight a year earlier, with services-sector credit accelerating fastest at 20.4%, up from 8.4% a year earlier. Deposits did not keep up: in that same fortnight, outstanding bank credit rose to Rs 215.15 lakh crore on 17.65% year-on-year growth, against deposit growth of just 12.21%, a gap of 5.44 percentage points, roughly 540 basis points, system-wide. At the annual level, the Economic Survey 2025-26's statistical appendix, sourced to RBI's Basic Statistical Returns, shows all-India banks' credit-deposit ratio at 80.1% at the end of March 2025, up from 79.6% at the end of March 2024, with credit growing 11.1% against deposit growth of 10.3%.

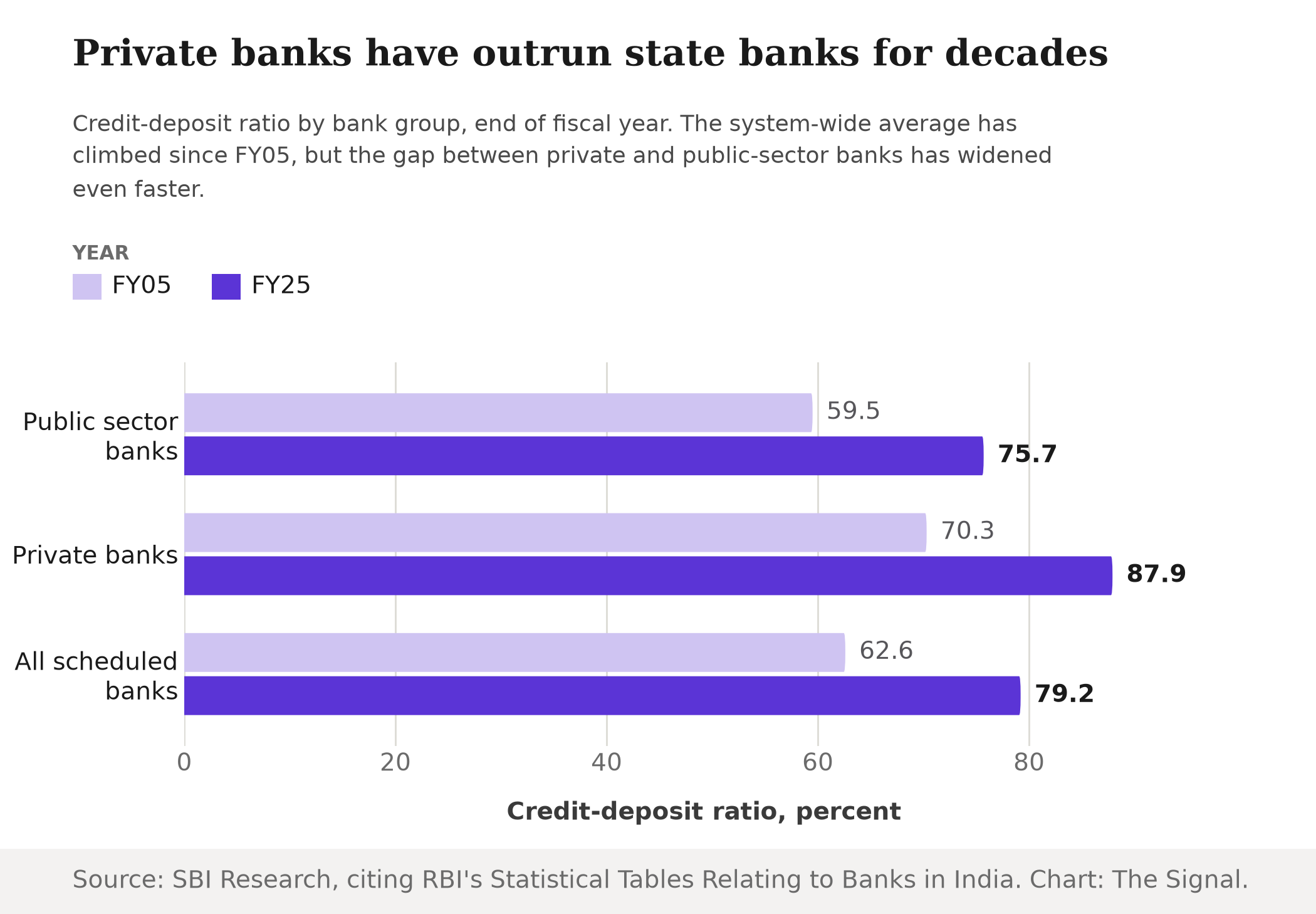

That gap has been building for two decades, and it runs straight through the ownership line this quarter's results seem to blur. SBI Research's compilation of RBI's own banking statistics puts private banks' credit-deposit ratio at 87.9% and public-sector banks' at 75.7% as of the end of FY25 (March 2025), against an all-scheduled-bank average of 79.2%, itself up from 62.6% two decades earlier at the end of FY05 (March 2005).

Whoever it hits, the fix costs more

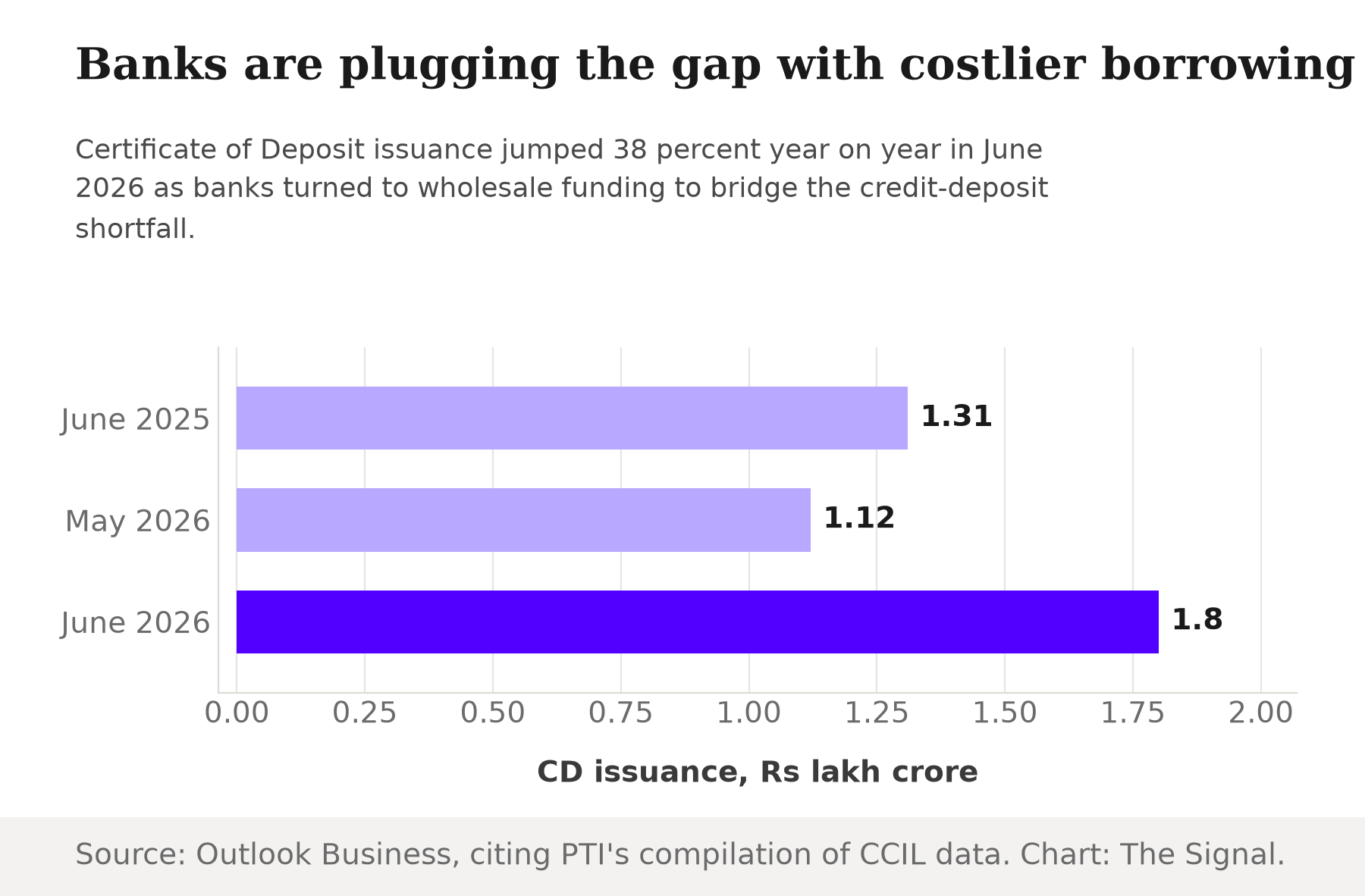

When a bank's loan book outgrows its deposit base, the shortfall does not disappear. It gets funded, typically through wholesale borrowing that costs more than a savings or current account. Banks' fundraising through Certificates of Deposit surged 38% year-on-year to Rs 1.80 lakh crore in June 2026, up from Rs 1.12 lakh crore in May 2026 and Rs 1.31 lakh crore in June 2025, driven by tighter liquidity conditions and robust credit growth. That reach for wholesale money is a system-wide reflex, not a state-bank-only one.

Nor is the pressure expected to ease on its own. CRISIL Ratings forecasts bank credit growth of around 13% in FY27, a cooldown from the double-digit pace banks are currently reporting, but still a rate that outruns what most lenders' deposit books have shown they can generate on their own. That FY27 forecast is itself a slowdown from CRISIL's own ~14% estimate for FY26. The rating agency's own numbers show why the gap will not close on its own: the shortfall between credit and deposit growth, which had briefly closed in early FY26, had widened back out to about 300 basis points by mid-March 2026, with certificate-of-deposit issuance growing roughly 27% even as deposits grew just under 11%. A bank that cannot fund its loan growth from deposits alone pays more for every rupee it lends, whether the logo on its branch says a state emblem or a private one.

The honest objection

The strongest case for still reading this along ownership lines is that the structural numbers say so. Over two decades, private banks as a group have run a credit-deposit ratio roughly 12 percentage points above public-sector banks, as SBI Research's own compilation of RBI data shows, and that gap did not appear this quarter. It has held for twenty years. Ownership plainly correlates with how aggressively a bank lends against its deposit base.

That case is real, but it describes a difference in level, not this quarter's difference in momentum. Kotak's problem in Q1 FY27 is that its deposit growth lagged its own historical franchise strength, not that private banks in general are struggling to gather deposits. HDFC and Axis, the two banks setting the pace on deposits this quarter, are private, and so is Kotak, the bank posing the sharpest supply-demand mismatch outside the public sector. Ownership predicts the level of a bank's credit-deposit ratio reasonably well over twenty years, but it does not predict which specific bank is scrambling for deposits in any given quarter.

The Signal

The consensus reading of Q1 FY27, private banks winning deposits while state-run banks trail, flatters two banks by crediting their franchise strength to their ownership tag, and does the reverse to Kotak by hiding its shortfall behind a "private bank" label that often signals safety. What actually separates banks right now is how large and sticky their retail deposit base already was before this credit cycle began, not which shareholder controls the bank. Watch Kotak's deposit growth next quarter and the certificate-of-deposit data alongside it. If Kotak's gap narrows while the state-run banks' stays wide, ownership will have reasserted itself as the dividing line. If it does not, this is a system-wide scramble for deposits that happens to be cheaper to fund at two large private banks than everywhere else, and the costlier borrowing plugging that gap will keep showing up in margins across the board, not just at the banks currently getting blamed for it.

Reporting basis: the HDFC Bank Q1 FY27 update is per India Infoline's report of the bank's provisional business filing. The Axis Bank and Kotak Mahindra Bank Q1 FY27 figures are per Business Today's report of each bank's provisional update. Bank of Baroda's update is per Upstox, and Punjab National Bank's is per ScanX. System-wide credit and deposit growth for the fortnight ended May 31, 2026, is per the Reserve Bank of India's own press release and, for the credit-deposit differential specifically, per a Multibagg market-pulse report citing RBI data. The FY25 all-India credit-deposit ratio is from the Economic Survey 2025-26's statistical appendix, sourced to RBI's Basic Statistical Returns. The two-decade FY05-to-FY25 comparison by bank ownership is from SBI Research's compilation of RBI's Statistical Tables Relating to Banks in India. Certificate of Deposit issuance data is per Outlook Business's report of PTI's compilation of Clearing Corporation of India figures, and the FY27 credit growth forecast is per CRISIL Ratings, as reported by Upstox. The FY26-versus-FY27 growth comparison and the widening credit-deposit gap and CD-funding figures are from CRISIL Ratings' own April 2026 outlook note. The basis-point gaps between each bank's advances and deposit growth, and the percentage-point comparisons across bank groups, are The Signal's calculations from those figures.