Adani Enterprises and Abu Dhabi's IHC, through its International Resources Holding arm, have agreed to build a 50:50 joint venture for an $11.5 billion (about ₹1.08 lakh crore) integrated aluminium project in Odisha. The plan comprises a 4 MMTPA (million tonnes a year) alumina refinery, a 2 MMTPA aluminium smelter, a 4,000-megawatt captive power plant and a 1 MMTPA downstream manufacturing park, funded in two phases of roughly ₹66,000 crore and ₹44,000 crore. The easy read is capacity addition: a new source of virgin metal, some of what India imports made at home instead. Read only the announcement and this is a scale story.

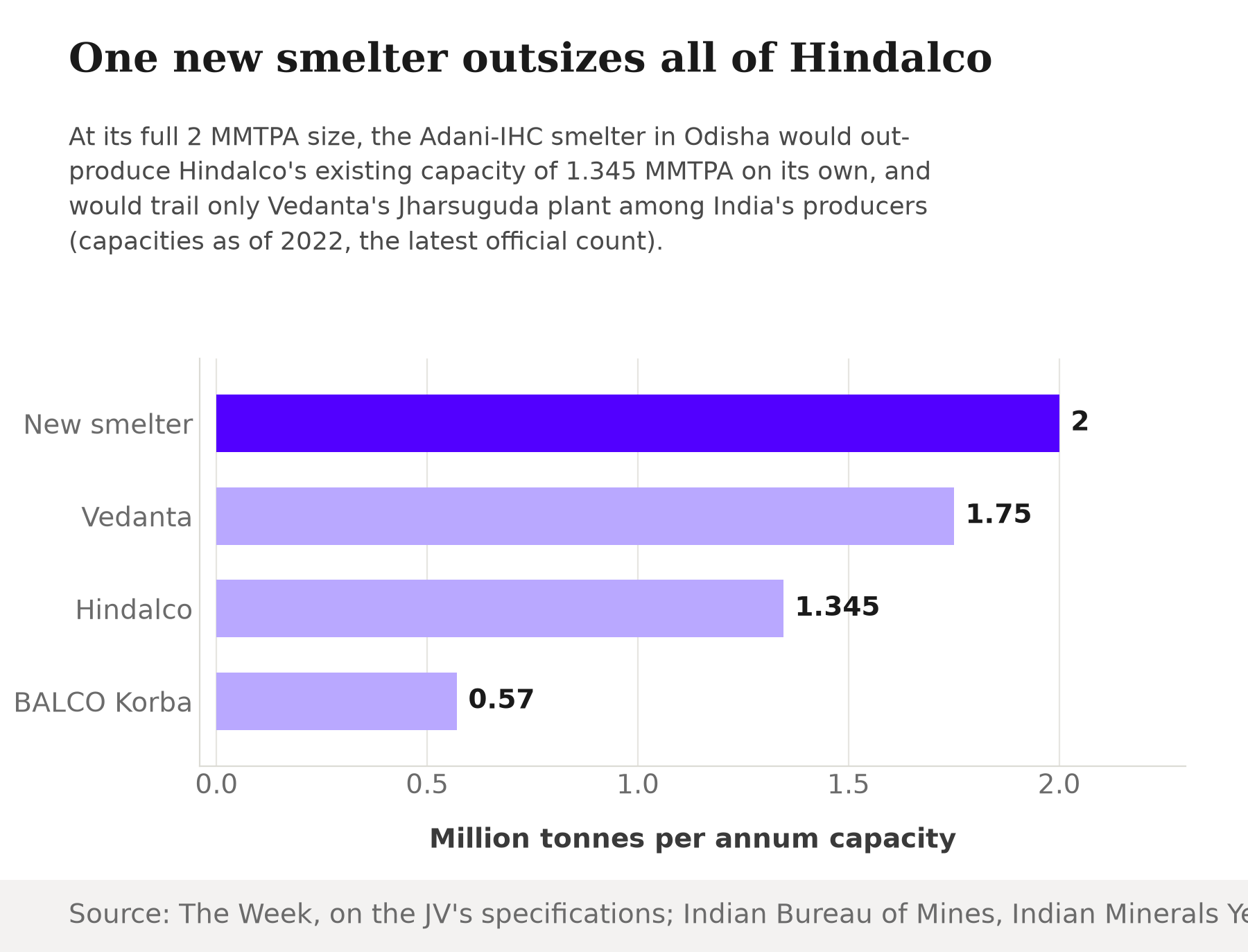

It is worth slowing down on that framing. India's primary aluminium supply has effectively run through two private producers for decades. Hindalco's capacity stood at about 1.345 million tonnes a year, well behind Vedanta Aluminium's roughly 2.32 million tonnes, split between 1.75 MTPA at Jharsuguda and 0.57 MTPA at BALCO's Korba plant. State-run NALCO's Angul smelter added a present capacity of 4.60 lakh tonnes (0.46 million tonnes) a year, well under a third of either private rival's. Together, those three producers made up the entirety of India's domestic supply. A new entrant does not need years to matter here. It needs one smelter.

The new smelter alone would out-produce Hindalco's entire operation.

At its planned 2 MMTPA size, the Adani-IHC smelter would produce about 49% more metal a year than Hindalco's existing 1.345 MMTPA capacity, our calculation from the two figures, and would rank second in India behind only Vedanta's Jharsuguda plant. That is not a competitor nibbling at share. It arrives at a scale India's incumbents took decades to reach, on day one.

Why the math even works

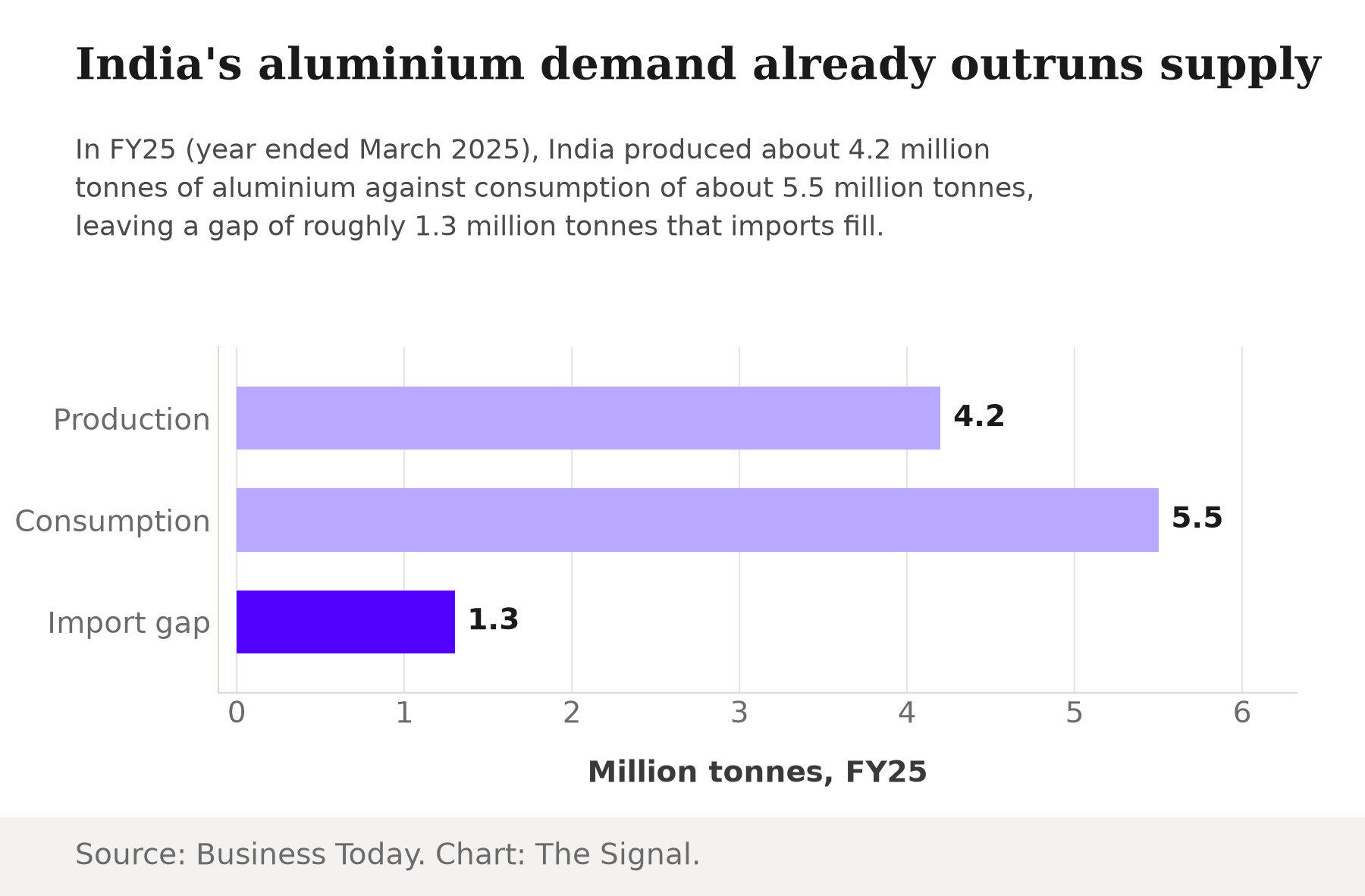

The reason a smelter this size makes sense: India is nowhere close to feeding itself. India produced a record 4.2 million tonnes of primary aluminium in FY25, up only marginally from 4.16 million tonnes the year before, keeping it the world's second-largest producer after China. But that 4.2 million tonnes sits against domestic consumption of about 5.5 million tonnes, a supply gap of roughly 1.3 million tonnes that imports currently fill.

A 2 MMTPA smelter, once fully ramped, would close most of that 1.3 million tonne gap on its own. That is the substitution case in one line: this is not capacity chasing a shrinking market, it is capacity aimed at metal India already buys from abroad every year.

Built where the raw material already is

The refinery-and-smelter combination is going up in Odisha for a reason that predates this deal. Odisha holds 41% of India's bauxite resources and produced 73% of the country's bauxite output in 2021-22, the ore that alumina refining and aluminium smelting both run on. Building the refinery next to the bauxite, and the smelter next to the refinery, cuts the freight between three stages of one supply chain. It is also why Vedanta's Jharsuguda smelter already sits in the same belt: this JV follows an established industrial logic, not a new one.

A third bet, and a steadier balance sheet

This is not IHC's first commitment to the Adani Group. IHC put $2 billion into Adani Green Energy, Adani Transmission and Adani Enterprises in 2022, then added a further $400 million into Adani Enterprises' FPO in January 2023. The Odisha aluminium project is the third and by far the largest.

| Year | IHC commitment | Amount |

|---|---|---|

| 2022 | Equity in Adani Green Energy, Adani Transmission, Adani Enterprises | $2 billion |

| January 2023 | Adani Enterprises FPO | $400 million |

| July 2026 | Odisha aluminium JV (50:50) | $11.5 billion |

Source: ThePrint; Business Today.

Each bet has been larger than the last, and this one is nearly five times the first two combined, our calculation from the amounts above. Part of what makes it plausible now is that Adani Enterprises is entering with a materially different balance sheet than it had for IHC's earlier checks. CARE Ratings puts Adani Enterprises' consolidated external debt to PBILDT, a measure of debt against operating cash flow, at about 3.43 times at the end of FY25, down from 5.85 times at the end of FY22. A company levered at nearly 6 times its operating cash flow taking on an $11.5 billion capital project would read very differently than the same company at 3.43 times. The deleveraging is what makes the scale of this bet arguable rather than reckless.

The honest objection

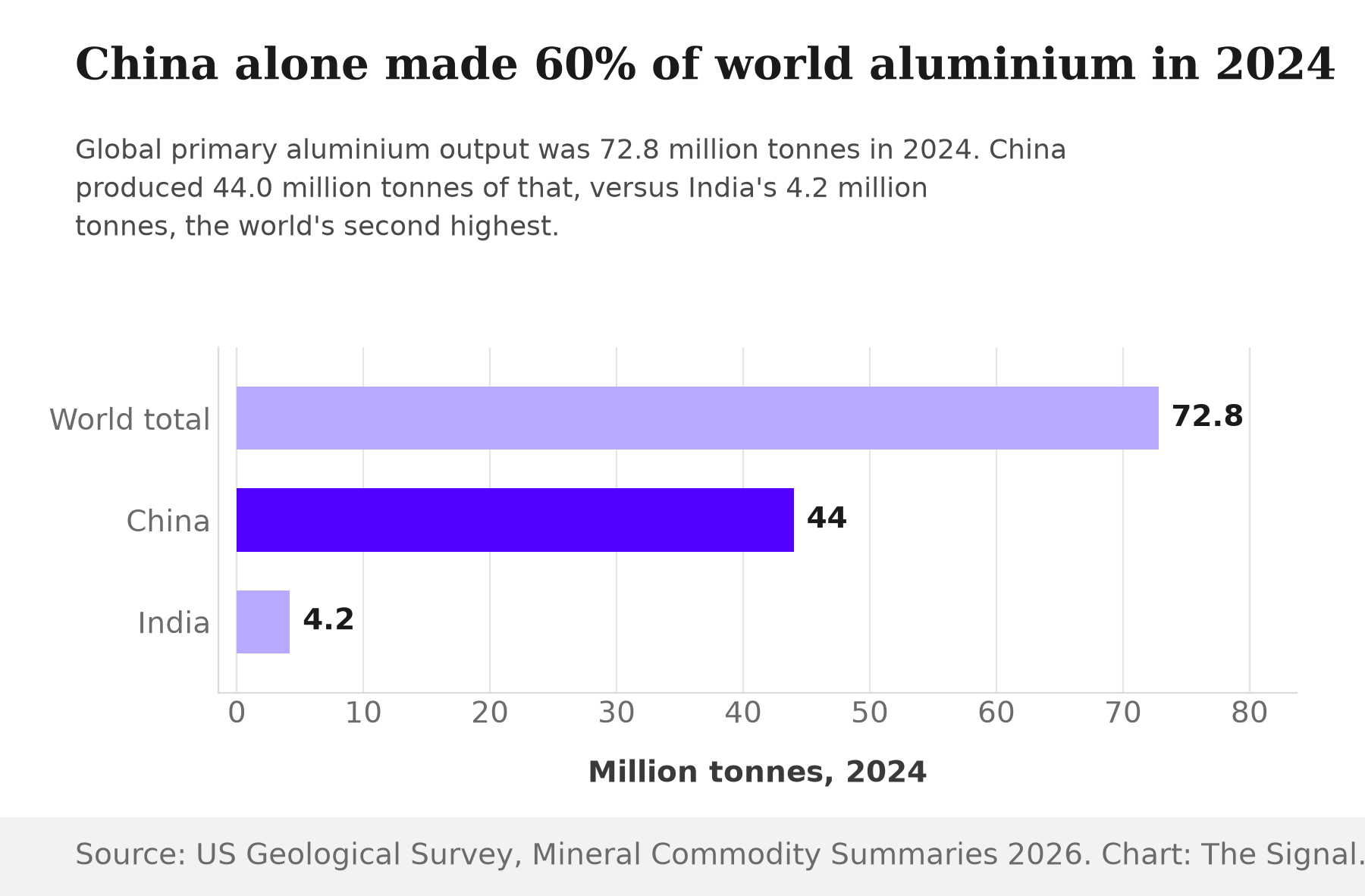

The strongest case against reading this as a clean structural shift is global aluminium's overcapacity problem, and it is real. China alone produced 44.0 million tonnes of the world's 72.8 million tonnes of primary aluminium in 2024, about 60% of global output, against India's 4.2 million tonnes. A producer that large can move price globally, and cheap Chinese metal reaching Indian ports would compress margins for every domestic smelter just as Adani-IHC's project tries to ramp to full capacity.

That risk is genuine, but it argues against the wrong target. The JV is not being built to chase export markets where Chinese supply already sets the price. It is aimed at a domestic gap of about 1.3 million tonnes that imports, including Chinese metal, already fill today. Global oversupply is a real ceiling on price and will squeeze the new entrant's margins like everyone else's. It does not remove the hole in India's own supply the smelter exists to fill.

The Signal

Hindalco and Vedanta have effectively set the price and the pace of India's aluminium market for two decades. That changes the day this smelter ships its first ingot, not the day the MoU was signed. Two things are worth watching once construction starts. First, whether the 2 MMTPA of new supply gets absorbed into the 1.3 million tonne import gap, which would mean India makes more of its own metal without anyone's margins getting hurt. Second, whether it instead lands on top of a domestic market the two incumbents have quietly kept tight, which would mean the first real price war among India's aluminium producers. Either way, a duopoly that has held since before this decade began now has to make room. The number to watch next is not the $11.5 billion price tag. It is the tonnage that actually leaves the smelter gate.

Reporting basis: the joint venture's structure and value are as reported by Business Today, citing the Adani Enterprises and IHC/International Resources Holding announcement, with the plant's technical specifications and phased financing as reported separately by The Week. India's FY25 production figures are from the Ministry of Mines' Press Information Bureau release; the FY25 consumption and import-gap figures, and Adani Enterprises' leverage ratios from CARE Ratings, are as reported by Business Today. Existing producer capacities and Odisha's bauxite share are from the Indian Bureau of Mines' Indian Minerals Yearbook 2022, the most recent official count; NALCO's smelter capacity is from NALCO's own operations page. Global and Chinese production figures are from the US Geological Survey's Mineral Commodity Summaries 2026. IHC's 2022 and 2023 investments in the Adani Group are as reported by ThePrint. The smelter's percentage size advantage over Hindalco's existing capacity, and the multiple of the two earlier IHC investments that the Odisha commitment represents, are The Signal's calculations from the cited figures.