On 29 June 2026, a Gazette notification brought the Employees' Provident Funds Scheme, 2026 into force, replacing the EPF Scheme that had governed retirement saving since 1952. India's state broadcaster reports that the mandatory contribution rate itself did not move: employees and employers each still put in 12 percent of wages, exactly as before. Read only that number and the story is continuity, a seven-decade-old scheme renamed and modernised without touching the figure that actually funds it.

It is worth slowing down on where that 12 percent applies. Business Today reports that the 12 percent PF contribution is now compulsory only up to the statutory wage ceiling of Rs 15,000 a month, capping the mandatory contribution itself at Rs 1,800; anything a worker and employer would have contributed above that ceiling is now voluntary, a change touching nearly eight crore active EPFO members. The rate held. The base it applies to did not.

The scheme did not preserve the mandate. It shrank what the mandate covers.

| Monthly wage | Contribution rate, each side | Status under the EPF Scheme, 2026 |

|---|---|---|

| Up to Rs 15,000 | 12% | Mandatory |

| Above Rs 15,000 | 12% | Voluntary |

Source: News on Air; Business Today. Table: The Signal.

Why a rate cut would have mattered less than this

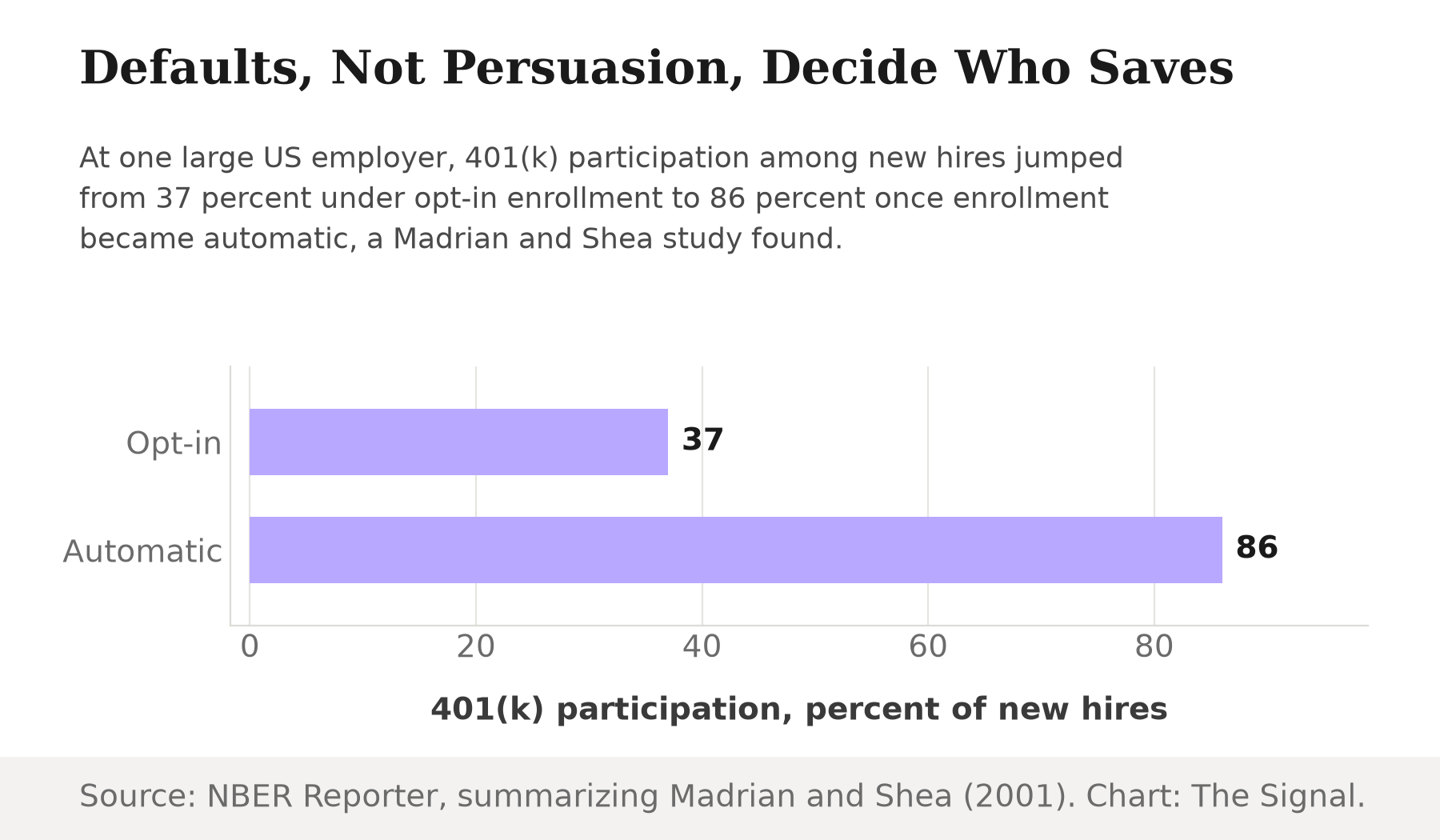

If the government had simply cut the mandatory rate from 12 percent to, say, 8 percent, every account would still be enrolled, just funded thinner. That is not what happened here. Above the wage ceiling, the contribution moved from automatic to elective, and behavioural economics has already run this exact experiment. An NBER research summary of Madrian and Shea's 2001 study found that when a large US employer switched its 401(k) plan from opt-in to automatic enrollment, participation among employees in their first three to fifteen months on the job jumped from 37 percent to 86 percent. Nothing about the plan's value changed between those two numbers, only the default a worker had to actively override.

Source: NBER Reporter, summarising Madrian and Shea (2001). Chart: The Signal.

Run that logic in reverse and the EPF Scheme, 2026 is not a neutral piece of housekeeping. It is India's own default switched off, for the slice of every wage that sits above Rs 15,000 a month. The mandate that took the enrollment decision away from nearly eight crore workers now hands it back, one payslip at a time.

A ceiling the Supreme Court told it to review

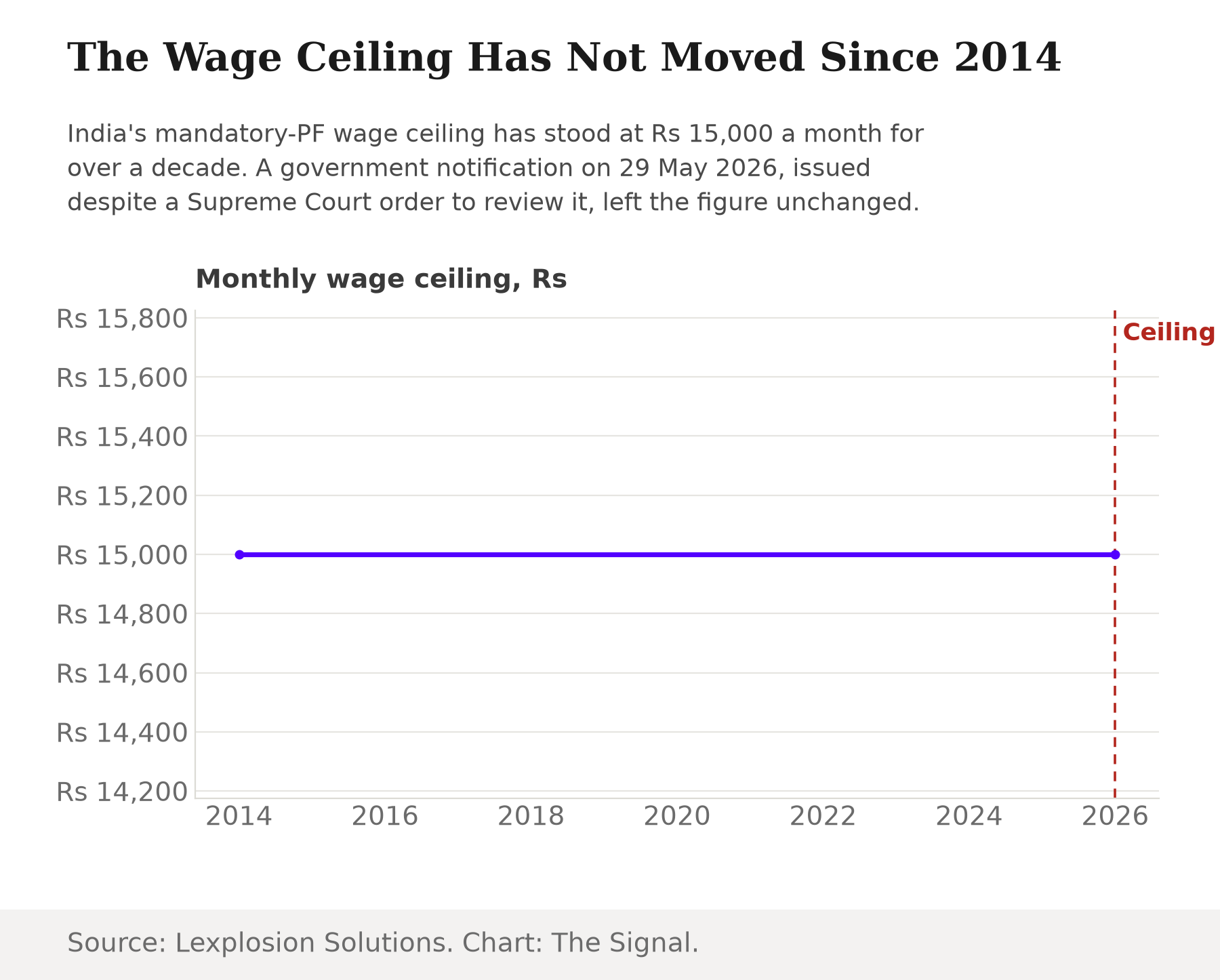

The Rs 15,000 figure is not new, and that is precisely the problem it creates. Lexplosion Solutions' regulatory bulletin reports that despite a Supreme Court order directing a review, the government's notification dated 29 May 2026 left the EPF wage ceiling unchanged at Rs 15,000 a month, the same level it has held since 2014. A ceiling frozen for over a decade, while wages elsewhere rose, means an ever-larger share of a typical formal-sector salary now falls into the newly voluntary zone, not the mandatory one.

Source: Lexplosion Solutions. Chart: The Signal.

What is riding on the default

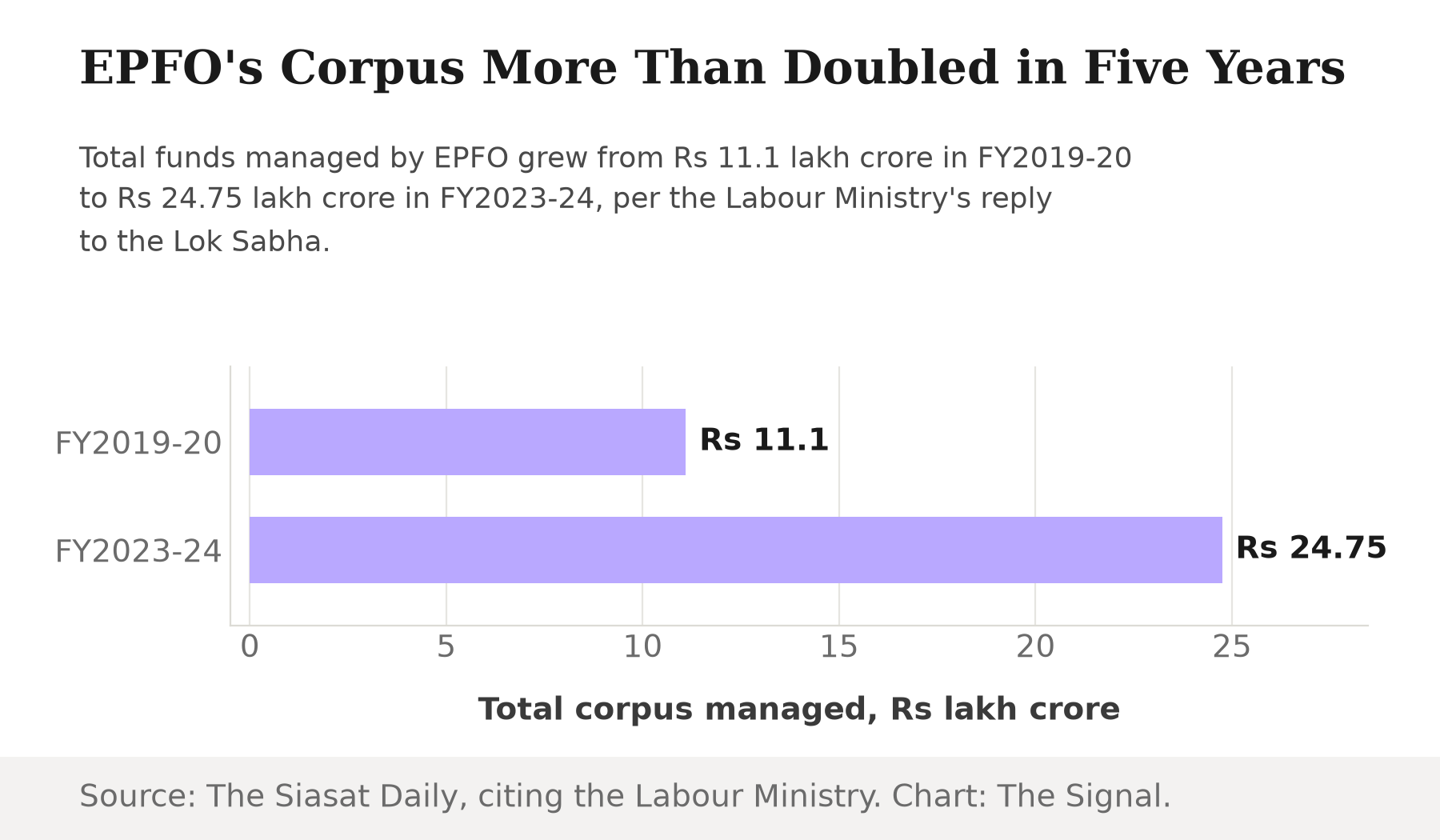

The stakes here are not abstract. DD News reports that EPFO's Central Board of Trustees retained an 8.25 percent annual interest rate on EPF deposits for FY2025-26, the second straight year at that level, to be credited to over seven crore subscriber accounts. And The Siasat Daily reports, citing the Labour Ministry's reply in the Lok Sabha, that the total corpus of funds managed by EPFO stood at Rs 24.75 lakh crore as of 31 March 2024, more than double the Rs 11.1 lakh crore it managed five years earlier in FY2019-20. That growth was built entirely under the old regime, where the contribution above the wage ceiling was never in question because, for most of that period, the ceiling covered a larger share of typical wages than it does now.

Source: The Siasat Daily, citing the Labour Ministry's reply in the Lok Sabha. Chart: The Signal.

Every rupee that now sits in the voluntary bucket and gets contributed anyway still earns that same 8.25 percent EPFO rate, compounding inside one of the few retirement instruments in India that offers a government-backed rate at all. Skip the box instead, and that rupee earns nothing at all, not in EPFO and not anywhere else, unless the worker separately picks another instrument. The scheme changed nothing about the return. It changed who has to ask for it.

The honest objection

The strongest case for the change is take-home pay. A worker earning just above Rs 15,000 a month, feeling inflation on groceries and rent today, may reasonably prefer the extra rupees now over a locked-in account payable decades from now. The government is not cutting anyone's core benefit; the mandatory contribution up to the wage ceiling is untouched, and the change simply lets a worker decide whether to save beyond that floor. For someone near the ceiling, the amount reclassified as voluntary is small in absolute rupees, and the case for choice over compulsion is real.

That case weakens further up the wage ladder. The higher a salary sits above Rs 15,000 a month, the larger the absolute rupee sum now sitting in the voluntary bucket, and it is precisely at higher, steadier salaries that the automatic-enrollment research carries its sharpest warning: participation swung between 37 percent and 86 percent purely on whether enrollment was opt-in or automatic. A worker earning several multiples of the wage ceiling has the most to lose from inertia and the least excuse for needing the extra rupees today, yet faces exactly the same passive box to tick as everyone else.

The Signal

The EPF Scheme, 2026 will be read, correctly, as a story about a contribution rate that survived its own rewrite untouched. The more consequential figure is the one that moved years before this notification: a wage ceiling stuck at Rs 15,000 since 2014, now acting as the line between saving that happens automatically and saving that has to be chosen. Watch what EPFO reports next on new voluntary enrollments above the ceiling, not the headline contribution rate. If the accounts opting in track anywhere near the share that opted in without a default to override them, India's retirement mandate has quietly become a retirement suggestion for everyone who earns enough to notice.

Reporting basis: the Employees' Provident Funds Scheme, 2026 and its effective date are per News on Air (Akashvani), reporting the Ministry of Labour and Employment's Gazette notification. The wage-ceiling threshold, the voluntary reclassification, and the nearly eight-crore-member figure are per Business Today, reporting the scheme notification. The Supreme Court review order and the unchanged wage ceiling are per Lexplosion Solutions' regulatory bulletin, reporting the Ministry's 29 May 2026 notification. The FY2025-26 interest rate is per DD News (Doordarshan), reporting EPFO's Central Board of Trustees. The EPFO corpus figures for FY2019-20 and FY2023-24 are per The Siasat Daily, citing the Labour Ministry's reply in the Lok Sabha; this is the only source for those figures. The automatic-enrollment participation study is a single Madrian and Shea (2001) finding, as summarised by the NBER Reporter, and is the only source for those two participation rates.