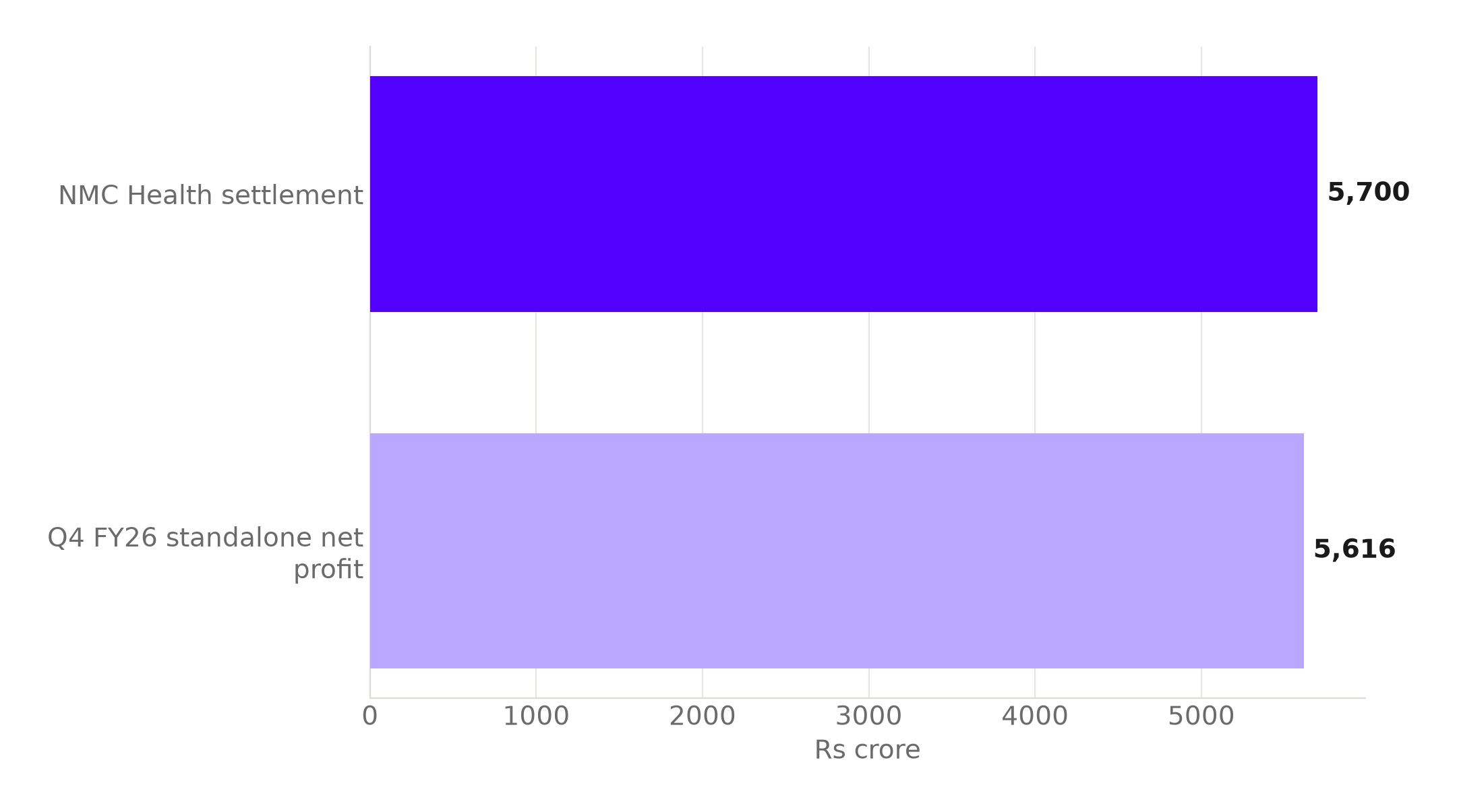

On July 2, 2026, Bank of Baroda's stock fell as much as 5.08 percent intraday, touching a low of Rs 257.70. The drop came after the state-run lender told exchanges it had reached an out-of-court settlement of $600 million, about Rs 5,700 crore, with the administrators pursuing claims tied to the collapse of NMC Health. Read as a single day's news, this looks like routine housekeeping: a large public-sector bank absorbs a one-time hit, the stock wobbles, the story moves on by the next session. NMC Health itself has not been a going concern for years. It formally entered administration in the United Kingdom on 9 April 2020.

It is worth slowing down on that "one-time hit" framing. Bank of Baroda's standalone net profit for the January to March 2026 quarter, its most recently reported quarter, was Rs 5,616 crore. The bank just wrote a check to close a six-year-old lawsuit that is larger than the profit it earned running its entire business for three months.

The settlement bill is bigger than three months of the bank's earnings.

The comparison holds even before counting the six years the exposure sat on the bank's books, unresolved.

Source: AGBI and Upstox. Chart: The Signal.

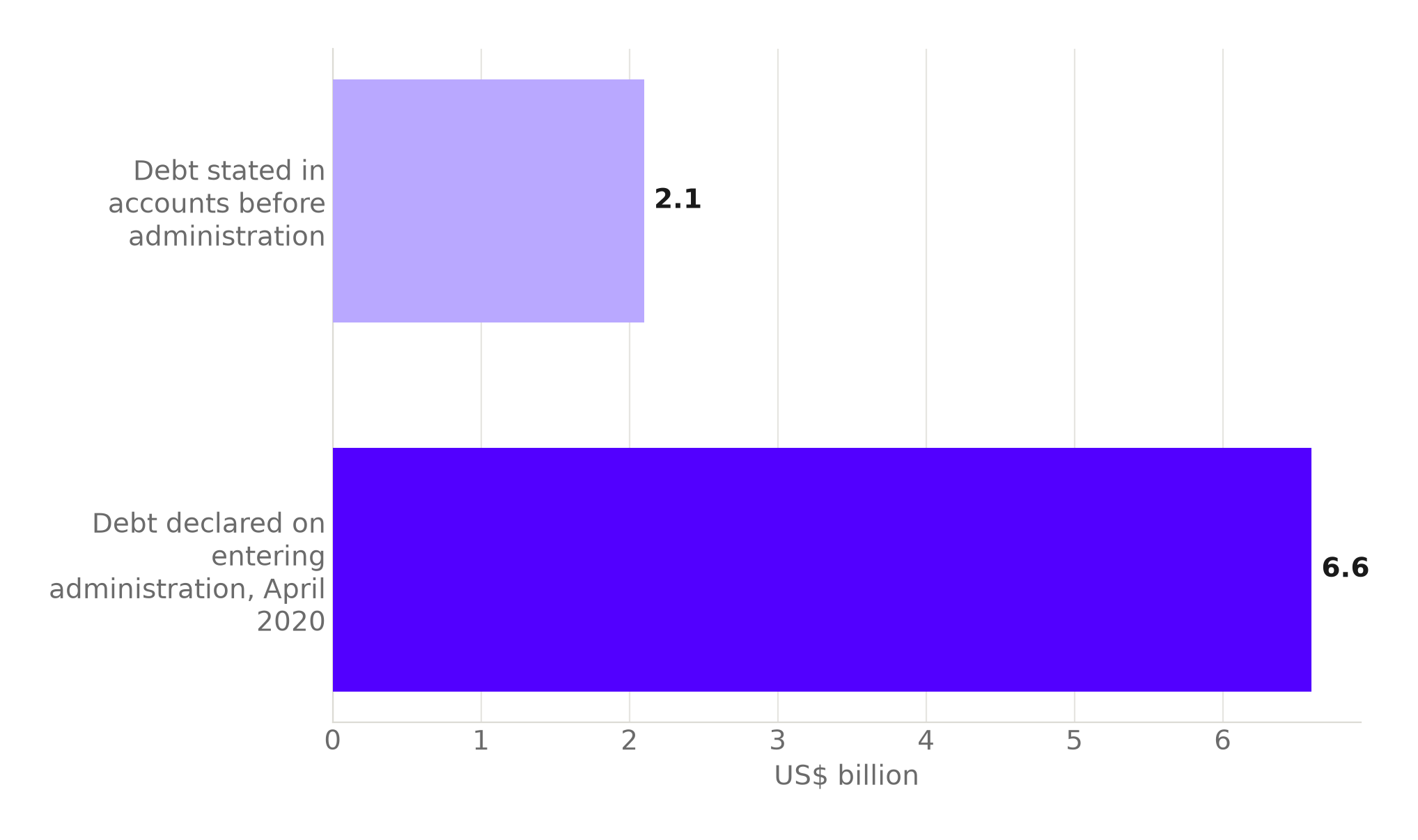

What NMC Health hid

NMC Health was, for over a decade, one of the largest private hospital operators in the Gulf, and its published finances turned out to be substantially false. The UK's Financial Conduct Authority found that NMC Health misled the market by understating its debts by as much as $4 billion. The concealment became impossible to hide once outside administrators opened the books: on entering administration in April 2020, NMC declared debts of $6.6 billion, far higher than the $2.1 billion its own accounts had previously stated.

NMC Health's declared debt more than tripled the moment administrators looked at the real books.

The gap between the two numbers is the size of the fraud the market had not priced in.

Source: The National. Chart: The Signal.

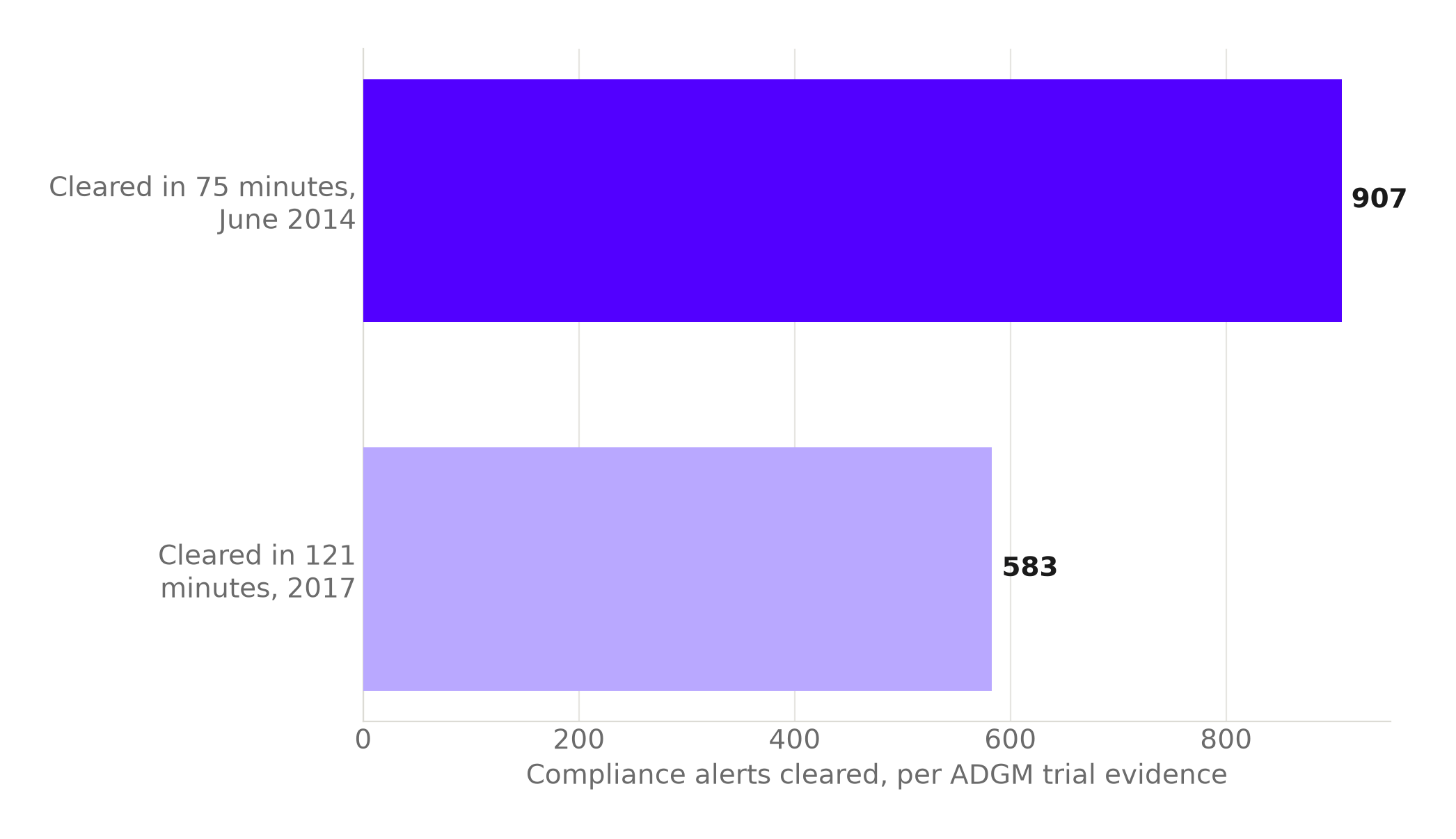

The bank in the middle

Bank of Baroda's exposure came from lending to the group, not from owning or directing it. But evidence presented at the trial in the Abu Dhabi Global Market alleged that NMC-linked payments were cleared through the bank in bulk: a Bank of Baroda executive allegedly cleared 907 compliance alerts within 75 minutes on one day in June 2014, and cleared 583 alerts in 121 minutes on another day in 2017.

Bank of Baroda's flagged NMC payments cleared in a rush, not one at a time.

Divided out, the first batch works out to about 12 alerts cleared every minute, the second to roughly 5 a minute, our calculation from the trial evidence. A number that fast is hard to reconcile with individual review of each flagged transaction.

Source: AGBI. Chart: The Signal.

That evidence sat inside a much larger case. Bank of Baroda was one of three defendants named in a $5.4 billion claim brought by NMC Health's administrators, alongside NMC's founder BR Shetty and its former chief executive Prasanth Manghat. Its $600 million settlement closes the bank's part of that claim; it says nothing about what the other two defendants will separately owe, or when.

A discount is the norm, not the exception

NMC's administrators went after more than the banks that moved money for the group. They sued the company's former auditor, EY, for about $2.6 billion in damages over its failure to detect the hidden debt. After years of litigation, EY agreed to settle for £105.5 million, a figure dwarfed by the damages originally claimed against it. Bank of Baroda's $600 million looks large in isolation. Set against a $5.4 billion claim naming three defendants, and an auditor case that closed for a fraction of what was sought, it reads as one more entry in a pattern this litigation keeps repeating: the number written in a claim and the number that eventually changes hands are two different numbers.

The honest objection

The strongest case against reading this settlement as an admission of serious wrongdoing is that out-of-court settlements are a routine way to close expensive, multi-year litigation, not a verdict on guilt. Banks settle to make a claim disappear regardless of its underlying merits, because fighting a $5.4 billion claim for several more years would cost more in legal fees and management attention than paying now. EY's experience supports that reading: administrators sought billions and collected a fraction, which suggests the opening claims in this case were priced for negotiation, not for what a court was ever likely to award. On this view, Bank of Baroda's $600 million is not proof the bank did anything wrong. It is the price of making a six-year-old distraction disappear.

That case is real, but it does not explain away the trial evidence on its own terms. A settlement figure can be a negotiated number with no fixed relationship to guilt. The compliance process it closes the book on is a different question: a description of how the bank's own alert system was allegedly operated on two separate occasions, three years apart. Paying to end a lawsuit and fixing whatever let hundreds of alerts clear in minutes are separate problems. A settlement resolves only one of them.

The Signal

Six years after NMC Health's collapse, Bank of Baroda has converted an open-ended overseas legal risk into a fixed, one-time number, and that number happens to match a full quarter's earnings. That is probably a reasonable trade for the bank: certainty is worth paying for when the alternative is indefinite exposure to a claim of this size. But the settlement itself answers nothing about whether the process that let hundreds of alerts clear in minutes, on two occasions years apart, has actually changed. Watch what Bank of Baroda discloses about its overseas compliance controls next. A bank that fixed the process would say so specifically. A bank that only fixed the bill will simply move to the next account, and it will not tell anyone which one until that number comes due too.

Reporting basis: the settlement amount and Bank of Baroda's exchange disclosure are per AGBI; the share-price move is per BusinessToday, an outlet independently covering the same event. NMC Health's administration date is from the UK's Companies House filing record, and the finding on debt understatement is from the Financial Conduct Authority's own press release, both primary artifacts the Signal verified directly. The debt NMC declared on entering administration and the damages sought from EY are per The National; EY's settlement figure is per Insurance Journal. Bank of Baroda's quarterly profit is per Upstox, reporting the bank's own results. The Abu Dhabi Global Market trial evidence on bulk-cleared alerts, and the claim naming Bank of Baroda, are both per AGBI and Gulf News respectively. The per-minute alert-clearing rates are The Signal's calculations from the trial evidence reported by AGBI.